Can you Change Car Insurance Companies at Any Point?

You can technically cancel your policy at any time, but doing so mid-term usually triggers a ‘short-rate’ cancellation penalty. This fee covers the insurer’s administrative costs and typically ranges from 2% to 7% of your annual premium. Unless you are at your renewal date, you should calculate whether your potential savings outweigh this penalty.

When is The Best Time to Change My Car Insurance Coverage?

The best time to look at your car insurance or think about switching is when something in your life changes, or when your policy is up for renewal.

Personal changes like moving to a new address or postal code, getting a new vehicle, or getting married can affect your rates. Switching at renewal makes sense because you avoid cancellation fees.

When It’s Not Recommended to Switch

Sometimes timing matters more than price. Switching right after a negative change to your driving record or too soon into a new policy can lock you into a higher premium or trigger extra fees.

It’s recommended to hold off on changing your policy if:

- You just renewed or recently switched policies

- You recently had a ticket or an accident

- Your risk profile just worsened (i.e. you had a recent claim)

Will Changing Car Insurance Companies Affect My Rate?

Changing companies does not affect your rate, but it can increase your insurance costs if your record has recently worsened.

Accident Forgiveness does not transfer between companies. If your current insurer is ‘forgiving’ an at-fault accident, a new company will see that accident on your record and charge you for it, often resulting in quotes that are 25% to 50% higher.

Should I Shop for Car Insurance Every Year?

Yes, you should compare rates every year, but that doesn’t mean you should always switch. Insurers constantly adjust pricing based on claims trends and profitability, and loyalty discounts often fade after the first term.

At the same time, your own risk profile may improve as tickets age or you build a longer claims-free history. By checking quotes 30-60 days before your renewal, you can ensure you’re not overpaying.

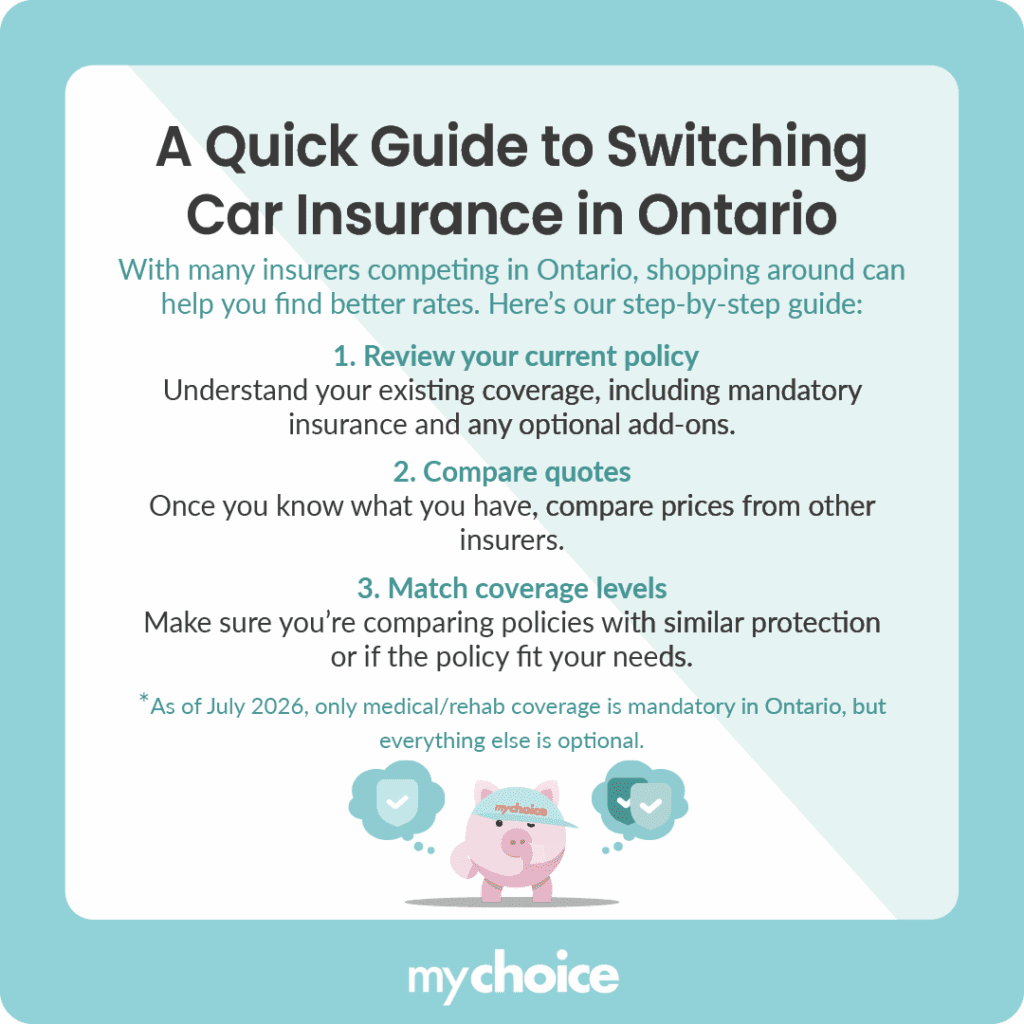

Why Shopping Around is Important

Before looking for a new car insurance company, understand your current policy and provider. For example, Ontario has certain minimum coverage amounts in its mandatory car insurance components.

While the government regulates standard policy terms, Ontario is moving to an ‘à la carte’ model on July 1, 2026. This means that while medical and rehabilitation benefits remain mandatory, other previously standard protections like income replacement and death benefits will become optional.

Once you understand your current policy, start comparing quotes from other companies. You can compare car insurance quotes from up to 30 best providers in Canada with MyChoice.

Key Advice from MyChoice

- Make sure your new coverage isn’t just cheaper because it has less protection. Always verify the limits and endorsements match your current needs.

- Never cancel your old policy until you have the new digital or physical legal pink slips in your hand. A gap in coverage of even one day can label you a ‘high-risk’ driver and double your future premiums.

- If you are switching your auto insurance, try to bundle it with your home, condo, or tenant coverage. Most Ontario insurers offer a 10% to 15% discount for multi-policy households.