Every life insurance premium number on this page comes straight from our quote database and represents real numbers, not ballpark estimates. Additioallly, the guidance around the numbers and the content is reviewed by a licensed broker.

This pages should help you learn how life insurance actually works in Canada, what pushes your premiums up or down, and how to lock in the most comprehensive, affordable coverage for your situation.

Quick Facts About Life Insurance Costs and Coverage in Canada

- 23 million Canadians own $6 trillion in life insurance coverage, according to CHLIA. Life insurance can help you provide for your loved ones’ financial future when you’re gone. There are various types of life insurance policies available to Canadians, each offering different levels of coverage.

- Based on MyChoice’s quote data, the average monthly premium for a 35-year-old non-smoker in Ontario with $500,000 in coverage is around $28.80 for men and $22.05 for women for a 20-year term policy.

- Whole life insurance costs significantly more, averaging $322 per month for men and $276 for women, while universal life insurance averages $278 and $242, respectively.

- Premiums rise sharply with age. A 45-year-old male pays roughly $63/month for a 20-year term policy, while a 65-year-old pays over $500/month for the same coverage.

How Life Insurance Works In Canada

Life insurance in Canada requires an insurer to pay out death benefits to your beneficiaries when you pass away. There are three basic types of life insurance you can get in Canada:

How Do I Know Which Policy is Right for Me?

Canadians can choose from whole, term, and universal life insurance to provide financial security for their loved ones. Here’s a table comparing the similarities and differences between these life insurance options:

| Whole life insurance | Term life insurance | Universal life insurance |

|---|---|---|

| Lifetime coverage | Temporary coverage (e.g. 10 or 20 years) | Lifetime coverage |

| Fixed premiums from the start of your policy | Fixed premiums for the specified term of the policy | May have flexible premiums |

| Typically more expensive than universal life insurance | Less expensive than whole or universal life insurance | May be more cost-effective than whole life insurance |

| The insurer chooses where to invest your premiums | No investment of premiums | You can choose where to invest your premiums |

| Consistent death benefit and cash value | Death benefit only | Death benefit and potentially higher cash value |

Life Insurance Cost in Canada by Policy Type

Below are the average monthly life insurance premiums in Canada by policy type and gender, giving you a quick look at how costs vary between short-term and permanent coverage options.

| Policy Type | Male | Female |

|---|---|---|

| 10-Year-Term | $20.25 | $14.40 |

| 15-Year-Term | $25.38 | $20.25 |

| 20-Year-Term | $28.80 | $22.05 |

| 30-Year-Term | $49.50 | $36.90 |

| Whole Life Guaranteed Pay | $322.20 | $276.30 |

| Universal Life | $278.00 | $241.75 |

Life Insurance Cost in Canada by Age and Gender

Life insurance rates rise steadily with age because insurers take on more risk as you get older. The table below shows how monthly premiums increase for term, whole, and universal life insurance across different age groups and genders.

| Age | Gender | Term 20 Life Insurance | Whole Life Guaranteed Pay | Universal Life |

|---|---|---|---|---|

| 25-year-old | Male | $27.00 | $209.25 | $181.33 |

| Female | $19.80 | $176.40 | $155.50 | |

| 35-year-old | Male | $28.80 | $322.20 | $278.00 |

| Female | $22.05 | $276.30 | $241.75 | |

| 45-year-old | Male | $63.45 | $522.00 | $452.17 |

| Female | $48.60 | $436.05 | $385.92 | |

| 55-year-old | Male | $161.10 | $830.70 | $730.08 |

| Female | $115.20 | $663.75 | $608.41 | |

| 65-year-old | Male | $505.35 | $1,462.95 | $1,282.32 |

| Female | $349.20 | $1,282.95 | $1,136.05 |

Life Insurance Cost in Canada by Coverage Amount

Your life insurance premiums depend heavily on how much coverage you choose. As expected, larger coverage amounts lead to higher monthly cost, but not always proportionally. The table below shows how rates scale across term, whole, and universal life insurance for both men and women.

| Coverage Amount | Gender | Term 20 Life Insurance | Whole Life Guaranteed Pay | Universal Life |

|---|---|---|---|---|

| $250,000 | Male | $19.13 | $169.65 | $145.50 |

| Female | $14.85 | $149.40 | $126.33 | |

| $500,000 | Male | $28.05 | $322.20 | $278.00 |

| Female | $22.05 | $276.30 | $241.75 | |

| $1,000,000 | Male | $43.20 | $626.40 | $548.00 |

| Female | $31.50 | $548.10 | $475.40 |

Who Provides Life Insurance Quotes in Canada?

There are a few different ways you can get life insurance quotes from various trusted providers in Canada. Here are four different ways you can use to get a life insurance quote.

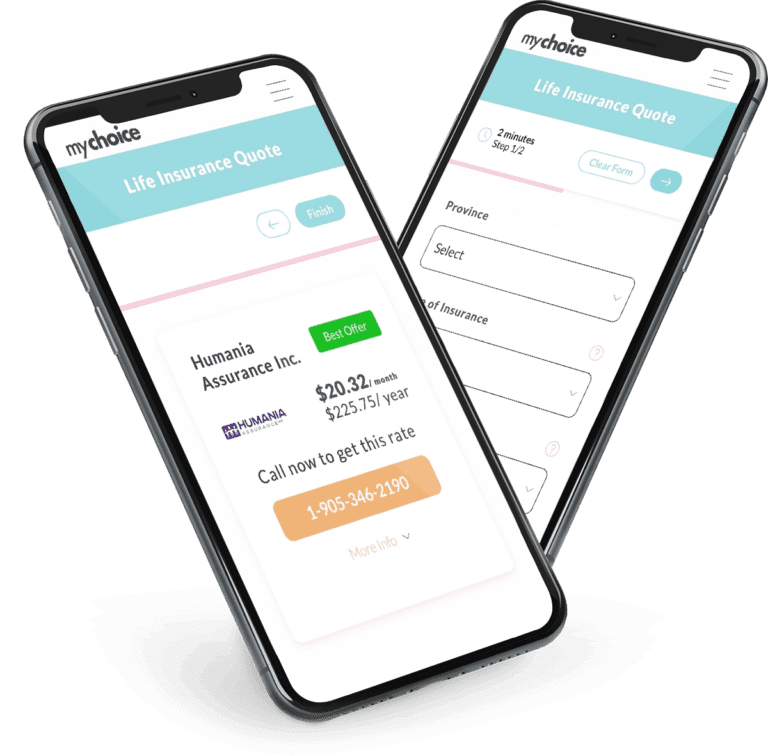

Why You Should Shop for Life Insurance with MyChoice

Shopping for life insurance is a snap with MyChoice’s user-friendly life insurance quoter. Share basic details like required coverage, age, and your province to get and compare quotes from trusted insurers in Canada.

It only takes a few minutes to enter your applicant information and secure the lowest rates for your budget on our site. Tell us what you want from your policy and insurer, and we’ll find the best deals available.

What Impacts My Life Insurance Premiums in Canada?

Several factors influence the price you’ll get for a life insurance quote in Canada. Understand these key considerations so you can make an informed decision in selecting a policy and provider:

How to Get Affordable Life Insurance in Canada?

Early financial planning and smart lifestyle choices can help you save money on life insurance in Canada. Here are some tips to help you lower your life insurance premiums:

- Buy as early as possible: Premiums are typically lower for younger people as they’re considered less risky by insurers.

- Have a healthy lifestyle: Non-smokers who maintain a healthy weight and get regular check-ups enjoy lower rates, as these choices demonstrate a lower likelihood of developing certain diseases.

- Bundle policies: Some insurers offer discounts

- Shop and compare to find cheap life insurance: Use MyChoice to compare quotes and coverage from different insurers without leaving your home.

Frequently Asked Questions About Life Insurance in Canada

How much is life insurance in Canada?

The average monthly premium for a 35-year-old non-smoker in Ontario with $500,000 in coverage is around $28.80 for men and $22.05 for women under a 20-year term policy.

The cost of life insurance in Canada depends on factors such as:

– Age

– Gender

– Family history of illnesses

– If you’re getting term or whole life insurance

How much life insurance do I need?

The average life insurance coverage in Canada is around $500,000. Use MyChoice’s life insurance calculator to check exactly how much life insurance coverage you need.

The amount of life insurance coverage you need depends on several factors, such as:

– Future income replacement for dependents when you pass away

– Your financial obligations

– Possible funeral and end-of-life expenses

– Assets and savings

Who needs life insurance?

If you fall under any of these categories, you may need life insurance to secure your loved ones’ financial future:

– Parents with dependents, especially those with minor or special-needs dependents

– Income earners

– Business owners or key employees

– Spouses

– Mortgage or debt holders

– High net-worth individuals

What is the difference between term life insurance and whole life insurance?

Term life insurance provides coverage for a specified number of years and pays out a benefit only if the insured passes away within that period. Whole life insurance offers lifetime coverage, including a death benefit and a growing cash value over time. Due to its more extended coverage and potentially larger benefits, whole life insurance is more expensive than term life insurance. Read our guide on the main differences between term and whole life insurance to learn more.

Can I get life insurance with pre-existing conditions?

Yes, you can get life insurance with pre-existing conditions. However, your policy may cost more because your insurer will consider you more likely to file a claim.

What happens after I apply for life insurance?

After you apply for life insurance, the insurer will usually contact you to complete the following steps:

Review of application and submitted documentation: The insurer will contact you to ensure all documents are complete and request any additional documents.

Medical examination: Depending on your policy, insurer, and other factors like age and history of family illness, you may be required to take a medical exam. The insurer may also request access to your medical records.

Underwriting: The insurer evaluates your application, medical records, medical exam results, and other documents to assess your risk profile.

Policy approval or modification: Based on their assessment, the insurer will approve your application or offer one with different terms. In some cases, the insurer may deem you too high-risk and deny your application.

Policy issuance and activation: The insurer sends an offer outlining the policy’s terms. If you accept, you make the first premium payment to activate the policy.

Ongoing coverage and management: By this time, the policy is in place. Make premium payments to keep it active, update beneficiary information when needed, and talk to your insurer if you need to make changes.

At what age should a person get life insurance?

The “best” age differs based on financial capability, health, and other circumstances. Typically, the best age to get life insurance is in your 20s, as you can lock in lower monthly premiums. The earlier you can factor life coverage into your budget, the easier it is to get affordable life insurance in Canada before serious health issues arise.

How do I make a life insurance claim?

The process between insurers may differ, but generally, you will take the following steps to make a life insurance claim:

1. Notify the insurer about the policyholder’s death as soon as possible.

2. Get the necessary documents for filing a claim – usually, you need a certified copy of the death certificate and the insurance policy.

3. Complete the claim form with any required information about beneficiaries.

4. Compile the claim form and documents to submit the claim to the insurer.

5. Wait for the claim to be approved, then receive the payment.