Cash Value Life Insurance Explained

If you’ve ever found yourself wondering “what is cash value life insurance, exactly?” then you’ve come to the right place.

Simply put, cash value life insurance is an umbrella term used to refer to permanent life insurance policies (such as whole life or universal life) that contain a cash value component. It combines the traditional death benefit (the amount paid out to beneficiaries upon the policyholder’s death) with an investment or savings element.

Because of this, premiums for cash value life insurance in Canada can be higher than their term life counterparts. As you make these regular payments, the policy’s tax-deferred cash value begins to grow. Part of each premium payment goes toward the cost of insurance and another portion builds cash value; this growth is tax-deferred. The growth rate depends on the type of policy and the insurer’s terms.

How to Withdraw from The Cash Value

The cash value of a life insurance policy can be accessed by the policyholder during their lifetime, providing a versatile financial resource that can be used for various purposes.

Policyholders can access the cash value of their life insurance in several ways:

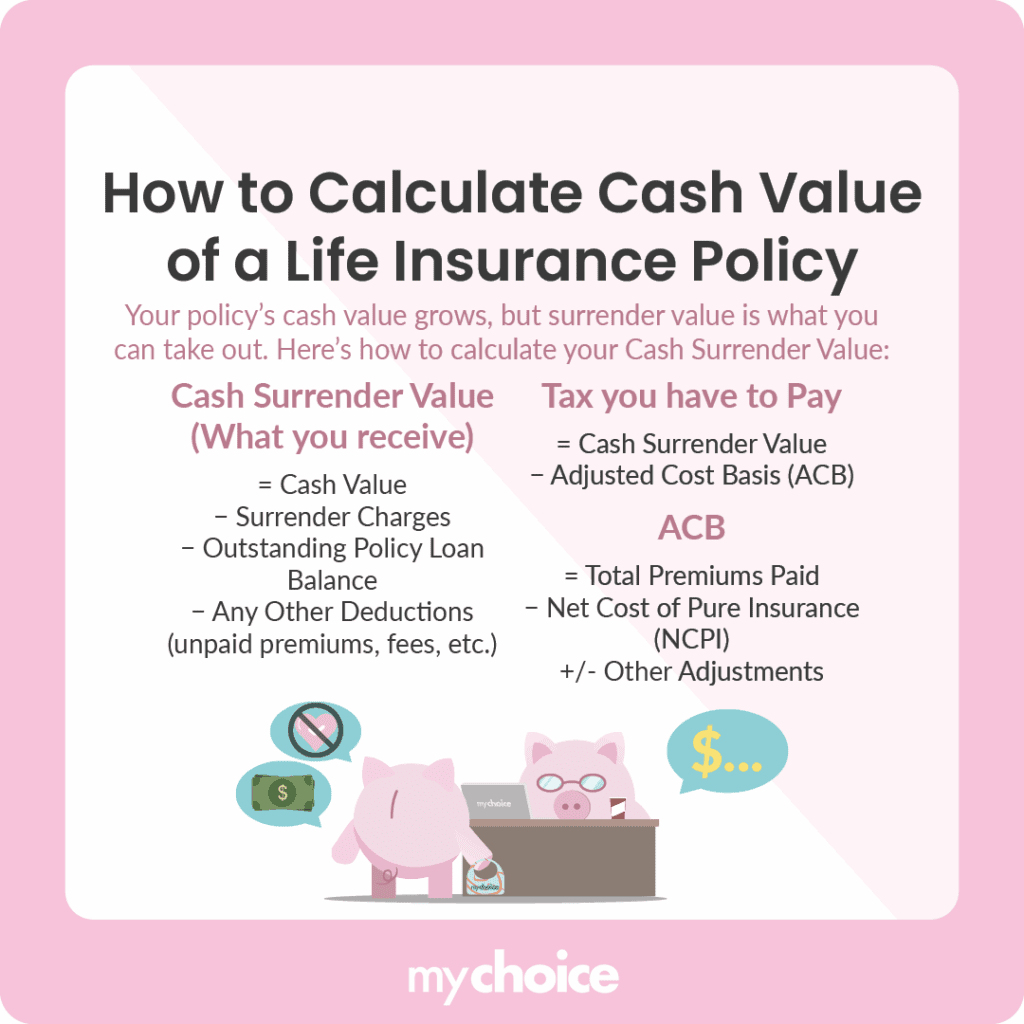

Surrendering A Policy For Cash Value

Surrendering a policy allows access to cash surrender value, but you may face surrender charges and taxes on gains above the adjusted cost basis.

But if you’re past the point when surrendering your policy incurs large fees because of the plan’s age, you’re able to choose between a lump sum payment or incremental payments. However, some policies don’t allow for this level of flexibility and will have the terms laid out in your contract.

Different Kinds of Life Insurance With Cash Value

Cash value components vary by policy type. Common permanent policies that include cash value are: whole life, universal life, indexed universal life, and variable universal life.

Key Advice from MyChoice

- Use cash value for short-term needs only when necessary. Borrowing reduces the cash value and death benefit, and unpaid loans accrue interest that further erodes value over time.

- Factor in tax and fees before accessing the cash value. Cash value withdrawals or policy surrender may trigger taxes on gains and surrender fees, especially if done early.

- Treat cash value as a living benefit, not a replacement investment. While you can access the cash value during your life, using it for lifestyle investments (like market investing) should be weighed against the loss of guaranteed protection and the cost of lost policy growth.