Can I Change My Insurance Mid Policy?

Yes, you can change your car insurance provider whenever you wish to. However, changing your policy midway will likely trigger a ‘short-rate’ cancellation penalty, which typically costs between 2% to 7% of your annual premium (roughly equivalent to one month’s payment) to cover the insurer’s administrative costs.

Why Drivers Switch Their Policies?

There are several reasons to change your current insurer, ranging from identifying coverage gaps in your insurance to shopping around for a better deal.

Common reasons for moving to a new provider include:

- Price Hikes: Rates rising without a clear change in your driving record.

- Service Issues: Poor claims handling or customer support.

- Better Perks: Discovering a provider with a more attractive telematics (driving app) discount or better coverage for new vehicles.

- Gap Protection: Seeking a “Waiver of Depreciation” (OPCF 43) for a newly financed or leased car.

How Often Can You Change Your Insurance Policy?

You can change your insurance policy as often as you want. As mentioned, changing your policy mid-term may incur charges. You will also need to ensure there is no gap in coverage. Discuss all this with your insurance provider when you intend to cancel their service.

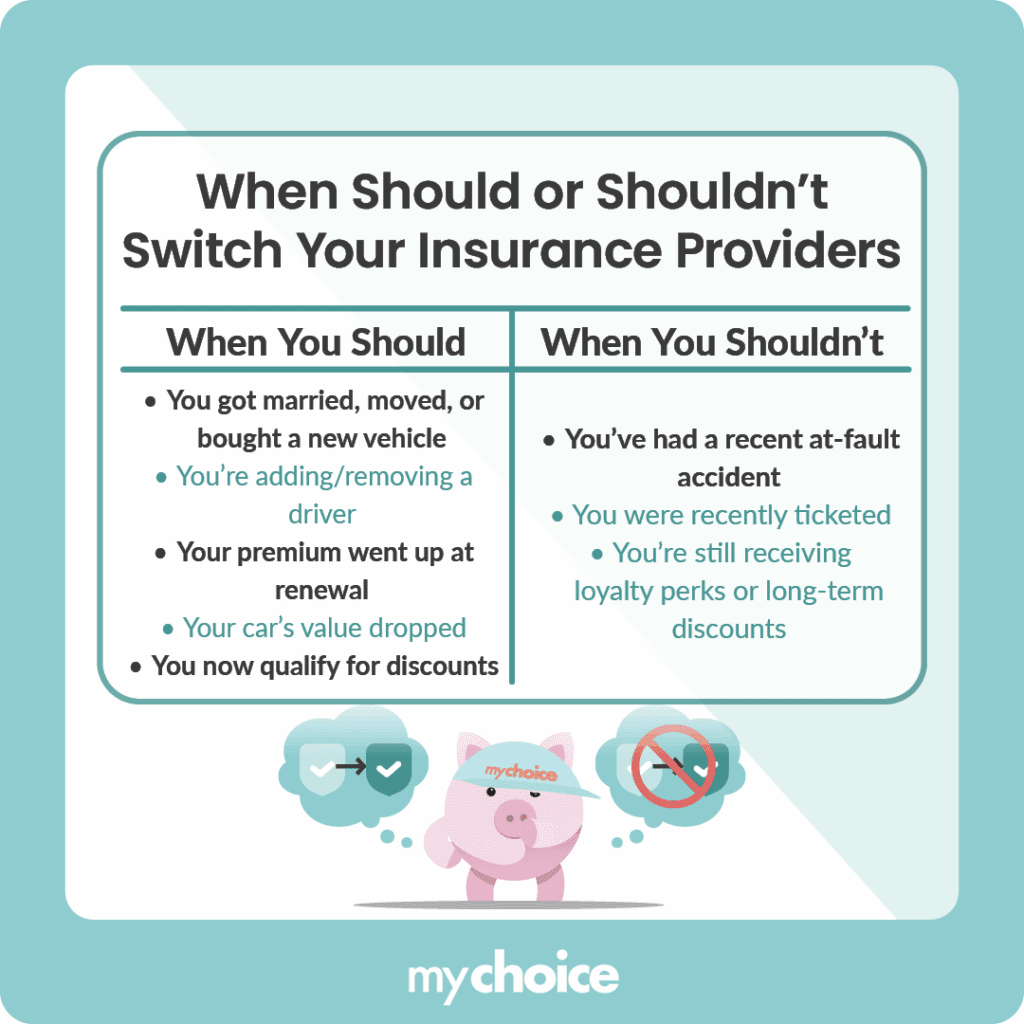

When Should You Switch Your Insurance Provider?

Below are a few reasons and life scenarios when you may want to start shopping around and consider switching your insurer.

Can You Switch While You Have An Open Claim With Your Current Provider?

Yes, you can switch insurance companies even when you have an open claim with your current one. Changing won’t affect the claim your insurer is supposed to pay.

Your original insurer remains legally responsible for processing and paying that specific claim because the accident happened while their policy was in force. You do not continue paying them premiums for future coverage. Simply continue communicating with their adjusters until the old file is closed, while your new provider covers you moving forward.

Key Advice from MyChoice

- Never stop payments or cancel your old policy until you have the new digital or physical pink slips in your possession.

- If you are six months into a policy, the short-rate penalty might be around $150 (based on the average premium in Ontario). If the new company saves you $300 over the course of the year, the switch still makes financial sense.

- If you are switching because you bought a new car, you must bind the new policy within 14 days of taking delivery to ensure seamless coverage.