Car Insurance for Uber and Lyft Drivers in Canada

Most drivers are surprised to learn that you don’t need a separate commercial insurance policy to drive for Uber or Lyft. Instead, you need your personal auto insurance, which is required by law, and a rideshare endorsement added to that policy. Uber and Lyft provide commercial coverage while you’re working, but this does not replace your personal insurance.

There are three main parts to how this works:

1. Your Personal Auto Insurance (Always Required)

By law, you must keep an active personal auto insurance policy. This is your only coverage when you’re offline, like when you drive to the store, pick up your kids, or run errands. It’s also the base for all other coverage.

Driving for Uber or Lyft without a valid personal policy will get your rideshare driver account deactivated. No exceptions.

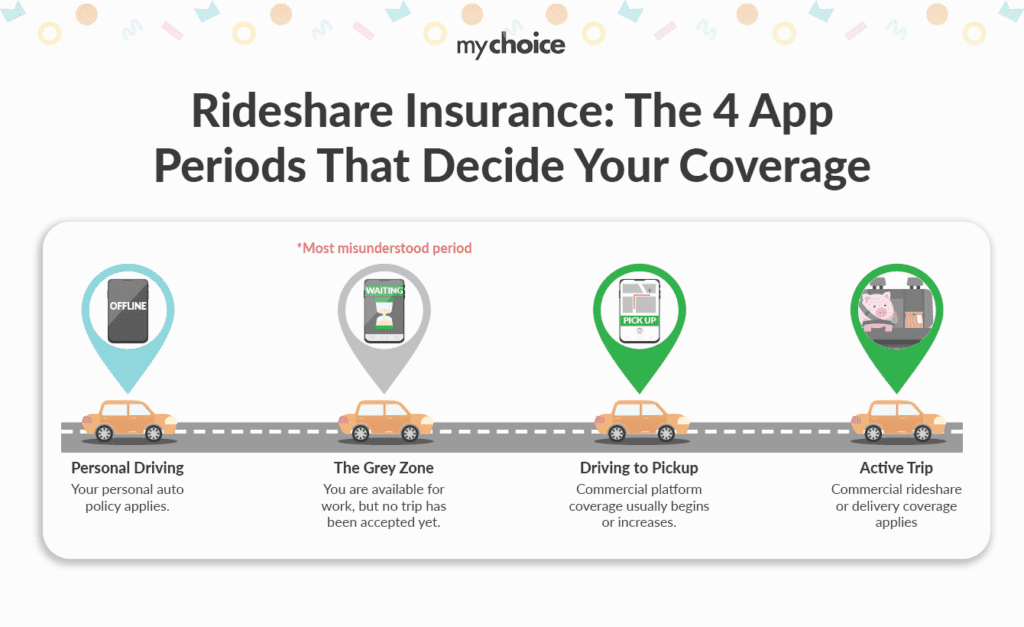

2. Uber and Lyft’s Automatic Commercial Coverage

As soon as you log into the rideshare app, the company’s commercial insurance starts. In Canada, Uber’s policy is underwritten by Intact, and the coverage changes depending on your activity. This coverage is automatic. You don’t pay for it separately or need to apply. It’s included when you drive on the platform.

3. The Gap: Why You Need a Rideshare Endorsement

This is where some drivers run into problems. Even though Uber covers you while you’re working, you must tell your insurer that you drive for a rideshare company. If you don’t, and they find out, whether it’s through a claim, an audit, or even talking to your broker, they can cancel your personal policy completely.

In Ontario, this rideshare endorsement is called the OPCF 6A. Adding a rideshare endorsement usually costs much less than a separate commercial policy, and it’s what keeps you fully protected instead of risking your coverage.

What Rideshare Insurance Covers

At a minimum, a rideshare insurance policy offers the following coverages:

- Third-party liability, which covers injuries or property damage you cause to others at any stage of rideshare driving.

- Passenger liability protects you if a passenger in your vehicle is injured.

- Collision coverage pays for damage to your own car if you are at fault in an accident.

- Comprehensive coverage which protects you from theft, vandalism, weather damage, and animal strikes

- Uninsured or underinsured motorist coverage that covers you if you are hit by someone who does not have enough insurance.

Beyond the basic coverage, you might want to consider the following as an Uber or Lyft driver:

- Interior damage coverage. It is not included in all policies, but if you drive full-time, wear and tear from passengers can add up.

- Loss of income protection. If your car is off the road due to a covered claim, some policies help replace lost earnings while you can’t drive

- Rental vehicle coverage. This helps you keep working by covering the cost of a rental car while yours is being repaired.

How To Shop For Rideshare Insurance

Getting a quote works much as it does for regular auto insurance, but there are a few more questions. Here’s what you can expect:

What Will Affect My Rideshare Insurance Premiums

Beyond the regular factors such as age, driving record, vehicle type, location, and annual mileage, there are some rideshare-specific factors that affect your car insurance premiums:

- Hours driven per week: The more hours you drive, the higher your premiums will be. Most policies set their prices based on hour ranges, such as under 20 hours, 20 to 40 hours, or over 40 hours.

- Which app or apps you drive for: If you drive for multiple platforms, your rate may go up.

- Your city: Urban drivers face a higher risk of accidents and theft. For example, in Ontario, a rideshare driver in Brampton will pay much more than someone in Kingston.

- Time of day: Some insurers consider whether you mainly drive during peak hours, late nights, or during the day.

- Vehicle age and safety features: Newer cars with advanced safety technology usually get better rates. Rideshare companies also often require vehicles to be under a certain age.

Pay attention to your policy details and the limits. Some policies limit how many hours you can drive each week. If you go over that limit, your coverage might not apply during those extra hours. Make sure the policy you choose matches how much you actually plan to work. It’s a good idea to add a little extra time, even if it costs more.

Does My Uber Insurance Affect My Personal Car Insurance

Getting rideshare insurance affects your personal auto policy in several ways, so it’s important to handle this carefully.

- You must tell your personal insurer. Most rideshare insurance providers require you to let your personal auto insurer know that you drive for a rideshare company, and some will notify them directly. This is not optional. If your personal insurer finds out you have been driving commercially and did not disclose it, they can cancel your policy retroactively.

- Your personal rates may go up. Some auto insurers raise premiums when they find out you are driving for a rideshare company, since the extra mileage increases wear on your vehicle and overall risk. Others do not change rates at all.

Before you contact your insurer, make sure to do your research on the following:

- Check whether your personal insurer allows rideshare driving. Some explicitly allow it, others prohibit it.

- Ask how your rates might change before you make any changes to your policy.

- If you have an accident, your rideshare insurer and personal insurer will need to work together on your claim. Which policy covers you depends on what you were doing at the time. If you were on a personal errand with the app off, your personal policy applies. If you were in any rideshare phase, the rideshare policy covers you. Having both policies with the same company makes the claims process easier.