Multi-Vehicle Insurance in Canada Explained

If your household has more than one vehicle, you might be paying too much for car insurance. Multi-vehicle insurance lets you cover two or more cars under one policy. Most Canadian insurers give you a 5% to 15% discount on each vehicle when you do this.

This is one of the easiest ways to lower your insurance bill without changing your coverage, deductible, or driving habits. Here’s how it works, when it’s a good idea, and when separate policies might be better.

How Much Can You Save With Multi-Vehicle Insurance?

The exact discount depends on your insurer, but most Canadian providers offer 5% to 15% off each vehicle’s premium when you bundle them on one policy.

Here’s what that looks like in practice using Ontario averages:

| Scenario | Separate Policies | Multi-Vehicle Policy (10% discount) | Annual Savings |

|---|---|---|---|

| 2 vehicles | $1,908 + $1,908 = $3,816 | $1,717 + $1,717 = $3,434 | $382 |

| 3 vehicles | $1,908 × 3 = $5,724 | $1,717 × 3 = $5,151 | $573 |

The more vehicles you add, the more the savings compound.

When Multi-Vehicle Insurance Makes Sense

Multi-vehicle insurance is a good option for most households that have more than one car. It can be especially useful in the following situations:

- Families with several drivers, like spouses, partners, or adult children, who each have their own car but live at the same address

- A single person who owns more than one vehicle, such as a daily driver and a weekend car, can save money by bundling both under one policy

- Households where all drivers have similar driving records can also benefit. If everyone has a clean record, the discount applies, and no one’s history increases the group rate.

- You can often add seasonal vehicles like boats, RVs, motorcycles, and snowmobiles to a multi-vehicle policy. This makes coverage simpler and usually costs less than insuring each one separately.

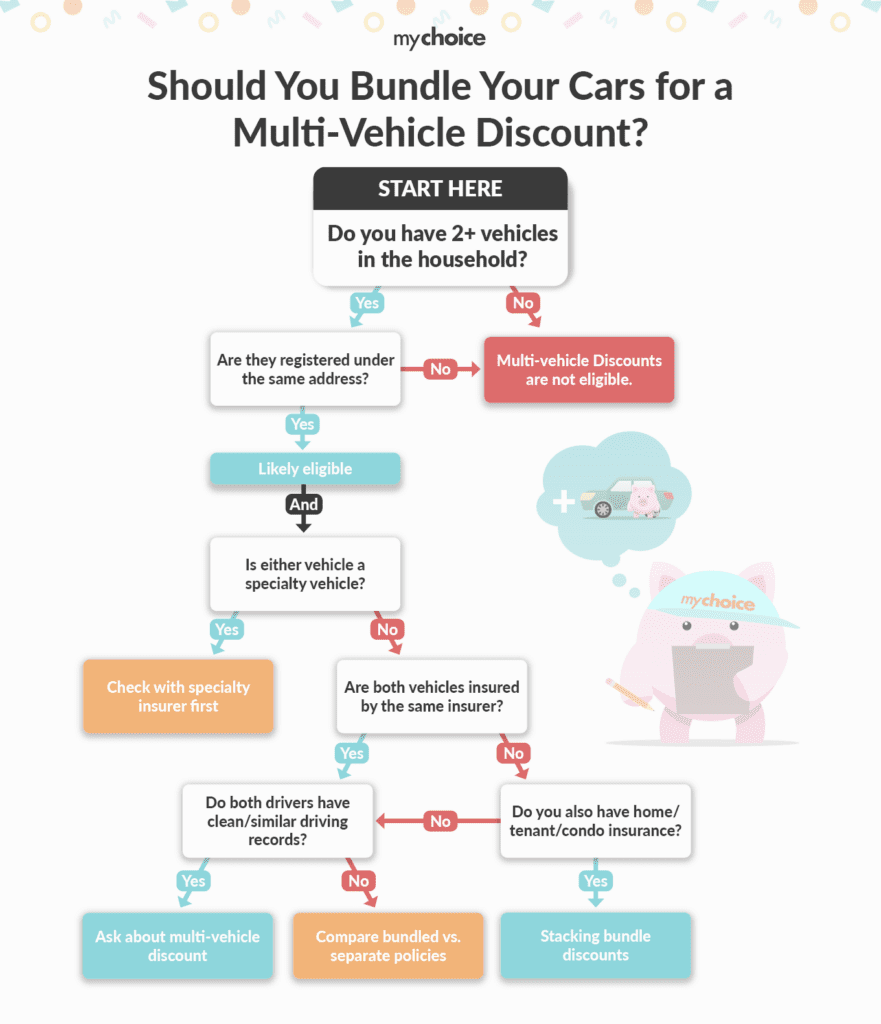

Below is a MyChoice infographic that should help you decide whether a multi-vehicle discount is the right fit for your situation.

When to Avoid Multi-Vehicle Insurance

Multi-vehicle insurance is not always the most affordable choice. In some cases, having separate policies could actually save you money.

- If someone in your household has a poor driving record, such as at-fault accidents, tickets, or a licence suspension, adding them to a multi-vehicle policy can increase the rate for every car. In this situation, it might be better to insure them separately, possibly with a company that specializes in high-risk drivers. This can help keep the rest of the household’s premiums lower.

- Young or new drivers in the household, especially those under 25, usually pay the highest premiums in Ontario. Adding them to a family multi-vehicle policy can sometimes raise the total cost more than you save with a bundling discount. It’s a good idea to compare both options before you decide.

- If your vehicles have very different risk profiles, such as a 2024 BMW and a 2012 Honda Civic, their insurance needs can vary a lot. In these cases, getting separate policies from different insurers might give you better rates for each car.

The best way to find out which option saves you more is to compare a multi-vehicle quote with individual quotes for each car. MyChoice lets you view both options side by side.

Can You Adjust Coverage for Each Vehicle?

Yes, and this is one of the biggest advantages of multi-vehicle insurance. You can choose different coverage for each car, so you’re not stuck with the same options for all your vehicles.

For example:

- For your newer vehicle, you might want full coverage, including collision, comprehensive, liability, accident forgiveness, and a waiver of depreciation.

- Your older vehicle might only need liability and basic coverage. By skipping collision and comprehensive, you can save hundreds of dollars each year on a car that has already lost much of its value.

This flexibility lets you protect the cars that need it most, while keeping costs low for the ones that don’t. You can do all this with one convenient policy.

Can I Add Another Vehicle to My Existing Policy?

Yes. Most insurers let you add a vehicle to your policy whenever you need. The multi-vehicle discount usually starts right away and might even be applied from the beginning of your current policy term. You can call your insurer or update your quote online.

Do All Drivers on the Policy Need to Live at the Same Address?

Generally, yes. Multi-vehicle insurance is meant for households, so most insurers want all drivers and vehicles registered at the same address. There are some exceptions, such as a child who is away at university but still uses the family home as their main address.

Will a Claim on One Vehicle Raise Rates on All of Them?

An at-fault claim will affect the rate for the driver who caused the incident. Since all vehicles are on one policy, the overall premium may go up at renewal. This also happens with separate policies, because insurers track driver records no matter how your policy is set up. Adding accident forgiveness (OPCF 39 in Ontario) can prevent a first at-fault claim from affecting your rates.

Can I Bundle Home and Auto on Top of Multi-vehicle?

Yes. Combining a multi-vehicle discount with a home-and-auto bundle is a great way to save more. Many insurers offer 5% to 15% off for multi-vehicle policies and an additional 5% to 20% off for bundling home insurance. These discounts usually add up.