Car Insurance For Non-Residents in Canada

Driving in Canada without valid car insurance is illegal in every province. This rule applies to tourists, international students, work permit holders, and new permanent residents who have not switched their insurance yet. The good news is that getting car insurance as a non-resident in Canada is simple once you know what kind of coverage you need and how long you plan to stay.

This guide explains who needs Canadian car insurance, how much it costs, how to apply with a foreign licence, and what changes depending on the province.

Can Non-residents Drive in Canada?

If you are not a resident, you can drive in Canada as long as you have a valid driver’s licence and car insurance.

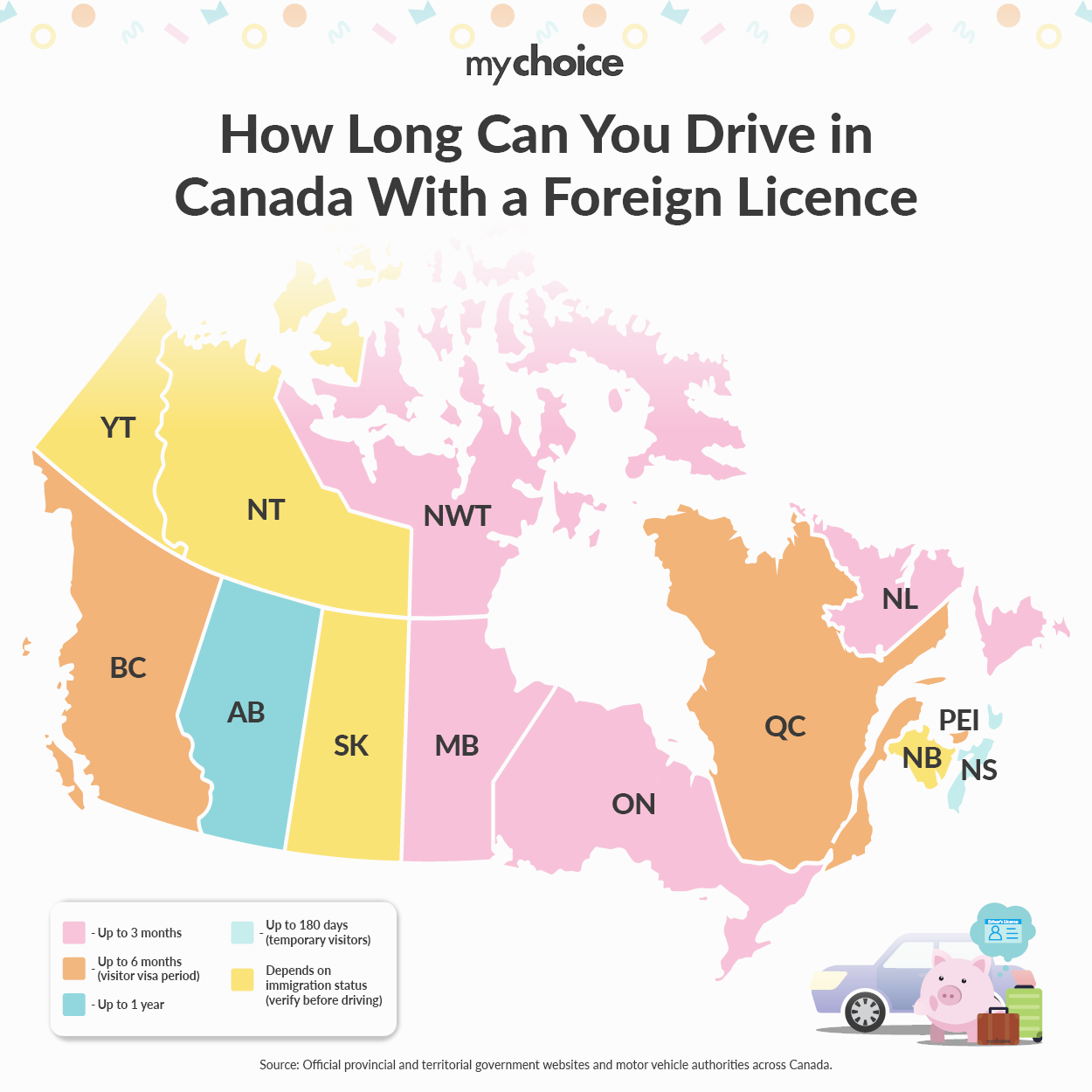

The amount of time you can drive in Canada with a foreign driver’s licence depends on the province. In some places, you can drive for three months, while in others, you may have up to a year before you need an International Driving Permit (IDP) or a Canadian licence. Here is a breakdown of the grace period for each province.

Once the grace period ends, you will need either an International Driving Permit from your home country, which must be in English or French, or a Canadian licence. To get a Canadian licence, you have to pass the knowledge and road tests in your province. The specific tests you need depend on your location. Some provinces have agreements with certain countries, so you might not need to take the road test at all.

The grace period does not include insurance. Even if your foreign licence is valid for several months, you must have Canadian car insurance or coverage that is recognized in Canada. Driving without it is illegal from your first day.

Does My Car Insurance From Home Cover Me in Canada?

The answer depends on your home country and the details of your insurance policy.

If you are driving from the United States, most US auto insurance policies automatically extend coverage into Canada. Your liability, collision, and comprehensive coverage usually apply just as they do at home. However, Canadian provinces have different minimum liability requirements than US states, and your US policy might not always meet them. For example, Ontario requires at least $200,000 in third-party liability coverage, which is also the minimum in most provinces. Before you cross the border, call your US insurer and ask for a Canadian Non-Resident Inter-Provincial Motor Vehicle Liability Insurance Card. This card, sometimes called the “yellow card” or “pink card” depending on the province, shows that your US insurance meets Canadian requirements.

If you are visiting from outside North America, some international insurers may cover you for up to 30 days while driving in another country, but this varies a lot. Many European, Asian, and other international policies do not include coverage in Canada. Always check with your insurer before you travel to make sure you are covered.

If your car insurance from home does not cover you in Canada or your 30-day window has ended, you need to get valid Canadian car insurance before you keep driving.

How Do Foreigners Get Insurance In Canada?

As a non-resident, you have two main options:

- You can get your own Canadian car insurance policy. To apply, you’ll need either an International Driving Permit or a Canadian driver’s licence.

- You can also be added to someone else’s insurance plan. If you are borrowing or sharing a car with a Canadian resident, they can list you as a driver on their policy.

Some insurers make it easier for non-residents to get car insurance than others. Certain companies focus on policies for newcomers and international drivers, but some may reject your application or charge higher rates if they cannot review your foreign driving records.

What You’ll Need to Apply for Car Insurance in Canada

- A valid International Driving Permit or a Canadian driver’s licence

- Proof of your current address in Canada, even if it is temporary housing

- Your foreign driving history, if you have it. Some insurers accept translated records.

- Details about the vehicle you will be driving

- Your visa or immigration documents that show how long you are allowed to stay

How to Get Cheap Rates as a Foreign Driver?

Car insurance in Canada is different from what you might be used to. Each province has its own rules, and some use a public system while others use private companies. This changes how you buy coverage and what rates you might pay as a newcomer.

In provinces such as Ontario, Alberta, and the Atlantic provinces, private companies sell car insurance and compete for your business. As a result, rates can vary a lot between insurers. Some companies are also much more open to accepting foreign driving records. For more details on how public and private systems compare, check out our guide on public vs. private car insurance in Canada.

Regardless of which province you’re in, here’s what actually moves the needle on your premium as a foreign driver:

- Get a Letter of Experience From Your Home Insurer. This is the most effective step you can take. This letter from your previous insurer shows how long you have been insured, your coverage history, and if you have made any claims. This can save you $500 to $1,000 each year.

- Choose a Vehicle That’s Cheap to Insure. The car you choose affects your insurance premium. Common, reliable models with low repair costs and good safety ratings usually have the lowest rates.

- Compare Quotes From Multiple Insurers. Insurers do not all price foreign drivers the same way. One company might quote you $3,500, while another offers $2,200 for the same coverage. Using MyChoice lets you compare several quotes at once.

- Take a Canadian Driving Course. If you complete an accredited driving course, most insurers will give you a discount.

- Bundle Policies If You Can. If you are renting or buying a home in Canada and need tenant or home insurance, you can usually save 5% to 10% by bundling it with your auto policy from the same provider.