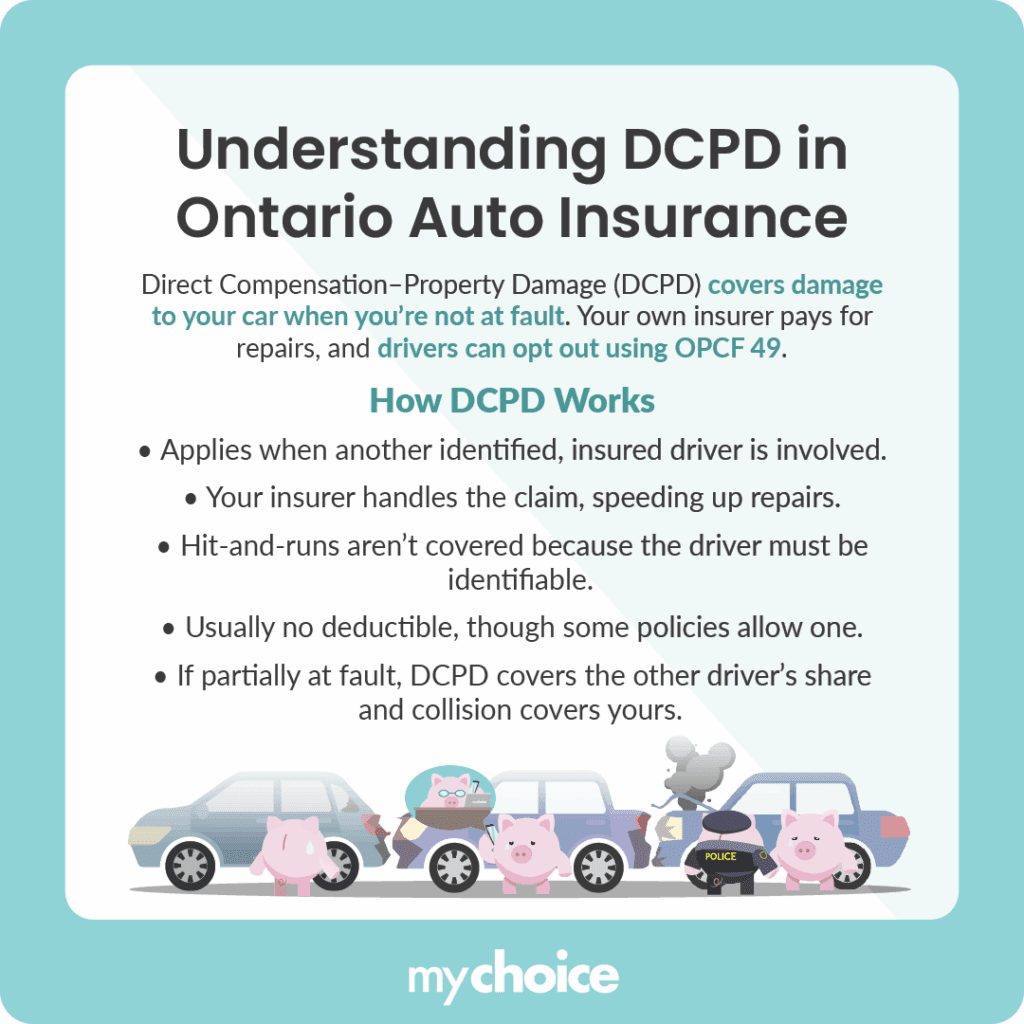

What is DCPD?

DCPD insurance is typically included in Ontario auto insurance policies, but drivers can choose to opt out of it through OPCF 49 as of January 1, 2024. It covers damage to your car and its contents if you’re deemed not at fault for an accident. It’s called “direct compensation” because your insurer provides the coverage.

Is DCPD Mandatory in Ontario?

DCPD coverage is included in standard Ontario auto insurance policies, but as of January 1, 2024 drivers can choose to opt out of it by adding the OPCF 49 endorsement. You can find it in all Ontario car insurance policies alongside third-party liability and accident coverage.

How Much Does DCPD Insurance Cost?

According to MyChoice internal quote data, the average cost of a DCPD coverage in Ontario is around $467 per year.

Why You Need DCPD Insurance

You need DCPD insurance because it ensures you get the money to cover repair bills as soon as possible. DCPD coverage pays out quickly because you’re dealing with your own insurer instead of the other driver’s. Because you get paid faster, you don’t have to pay out of pocket for repair bills.

DCPD insurance is important because it protects you from accidents you can’t control. According to our distracted driving research, 75% of Canadian drivers admitted to driving distracted.

Moreover, people often exhibit signs of careless driving, like failing to check their mirrors or eating while driving. This boosts their likelihood of getting in an accident that involves you even further.

The bottom line is that you can get in an accident even if you follow all the road rules, which is why you need DCPD insurance.

Where Do You Get DCPD Insurance?

You can get DCPD insurance alongside your basic auto insurance policy. Drivers usually buy car insurance from a broker or an insurance company’s agent. You can also visit insurance rate comparison sites like MyChoice to get a good look at what each insurer offers before purchasing a policy.

Either way, you need to have a policy before you can legally drive in Ontario.

How DCPD Works

DCPD works in a fairly straightforward way. DCPD applies when you are not at fault, or only partially at fault, in an accident involving another insured and identifiable vehicle. You don’t have to wait on the other driver’s insurer, so the process is generally much faster. This means you don’t have to spend too much money out of pocket to repair your car.

Under the DCPD system, your insurer pays for the damage directly rather than requiring you to claim against the other driver’s insurer.

Which Provinces Have DCPD Insurance?

Several Canadian provinces use direct compensation systems similar to Ontario’s DCPD, including:

- Alberta technically uses DCPD under its Care-First reforms

- Newfoundland

- Quebec

- New Brunswick

- Nova Scotia

- Prince Edward Island

Criteria to Use DCPD Insurance

DCPD insurance has four relatively strict criteria to kick in. If any of these four criteria aren’t fulfilled, your DCPD coverage won’t activate. The four criteria are:

- You can’t be at fault for the accident. This has to be established through an assessment according to the Insurance Act rules.

- The accident must involve one or more vehicles.

- All vehicles involved in the accident must have insurance and be clearly identifiable.

- The accident must have happened in Ontario.

Your DCPD coverage will activate if all four conditions are fulfilled.

Does DCPD Cover All Not-At-Fault Accidents?

DCPD doesn’t cover all non-at-fault accidents. If any of the four criteria aren’t met, your DCPD coverage won’t pay out. Two common scenarios are when the other driver is unidentifiable or uninsured.

In the case of hit-and-runs, your collision insurance will kick in. If the other driver is uninsured, you’ll be protected through your uninsured motorist coverage.

Key Facts About DCPD

DCPD insurance creates a fairer auto insurance landscape for all drivers. Drivers don’t have to wait long to get insurance coverage, and the burden of compensation falls onto the offending driver’s insurance company.

Here’s a summary of essential facts about DCPD insurance:

- DCPD insurance lets you arrange vehicle repairs with your insurance company. This means you’re dealing with people you know instead of another insurance company you might not be familiar with.

- DCPD insurance doesn’t impact your right to sue the other driver. So, you can still sue the other driver for injuries or other damages incurred in the accident.

- DCPD insurance doesn’t just cover your car. It also covers the loss of use and anything inside the car damaged in the accident.

- With DCPD insurance, your chosen insurer deals with the car repair process. This means you can choose your insurer based on how well they handle vehicle repairs.

- DCPD insurance speeds up the vehicle repair process since you don’t have to wait on compensation from the other person’s insurer.

- DCPD insurance regulations ensure transparency when determining accident faults. This means you know for sure who’s at fault for the accident.

Key Advice from MyChoice

- Think carefully before opting out of DCPD coverage. While removing it may lower your premium, you could lose important protection for not-at-fault accidents.

- Review your overall coverage before making changes. If you opt out of DCPD, you may need stronger collision or other coverage to avoid paying for repairs out of pocket.

- Compare quotes before adjusting your coverage. Shopping around can help you understand how much DCPD coverage affects your premium and whether keeping it offers better value.