What Is All Perils Coverage?

All perils coverage, also called an all-risk policy, covers damage to your vehicle from both collision and non-collision events unless the cause is specifically excluded in the policy. It’s considered the broadest form of car insurance coverage. Because of its extensive protection, it’s typically more expensive than other car insurance policies.

All perils coverage also protects against theft by someone living in your household or an employee who uses or services the vehicle, which is normally excluded under comprehensive coverage.

While mandatory car insurance is a legal requirement to drive in Canada, all perils coverage is optional in most provinces. However, if you lease or finance a car, some financial institutions may require you to get this form of car insurance.

Comparing All Perils with Other Optional Coverages

Some providers may describe all perils coverage as a combination of collision and comprehensive insurance. But what are these types of coverage, and are there other types that protect your car from different risks?

The table below aims to explain the differences between these optional coverages.

| Coverage Type | What It Covers | Example Events |

|---|---|---|

| All Perils Coverage | Covers both collision and non-collision damage unless the cause is specifically excluded in the policy. | Theft, vandalism, fire, hailstorms, windstorms, falling objects, and collisions. |

| Specified Perils Coverage | Covers your vehicle only from the hazards specifically listed in the policy. If a risk is not listed, it is not covered. | Fire, lightning, theft, hailstorms, and windstorms. |

| Collision Coverage | Covers damage to your vehicle caused by a collision with another vehicle or object. | Crashing into another car, hitting a pole, guardrail, or tree. |

| Comprehensive Coverage | Covers damage caused by events outside your control, excluding collisions. | Attempted theft, vandalism, fire, falling objects, and weather damage. |

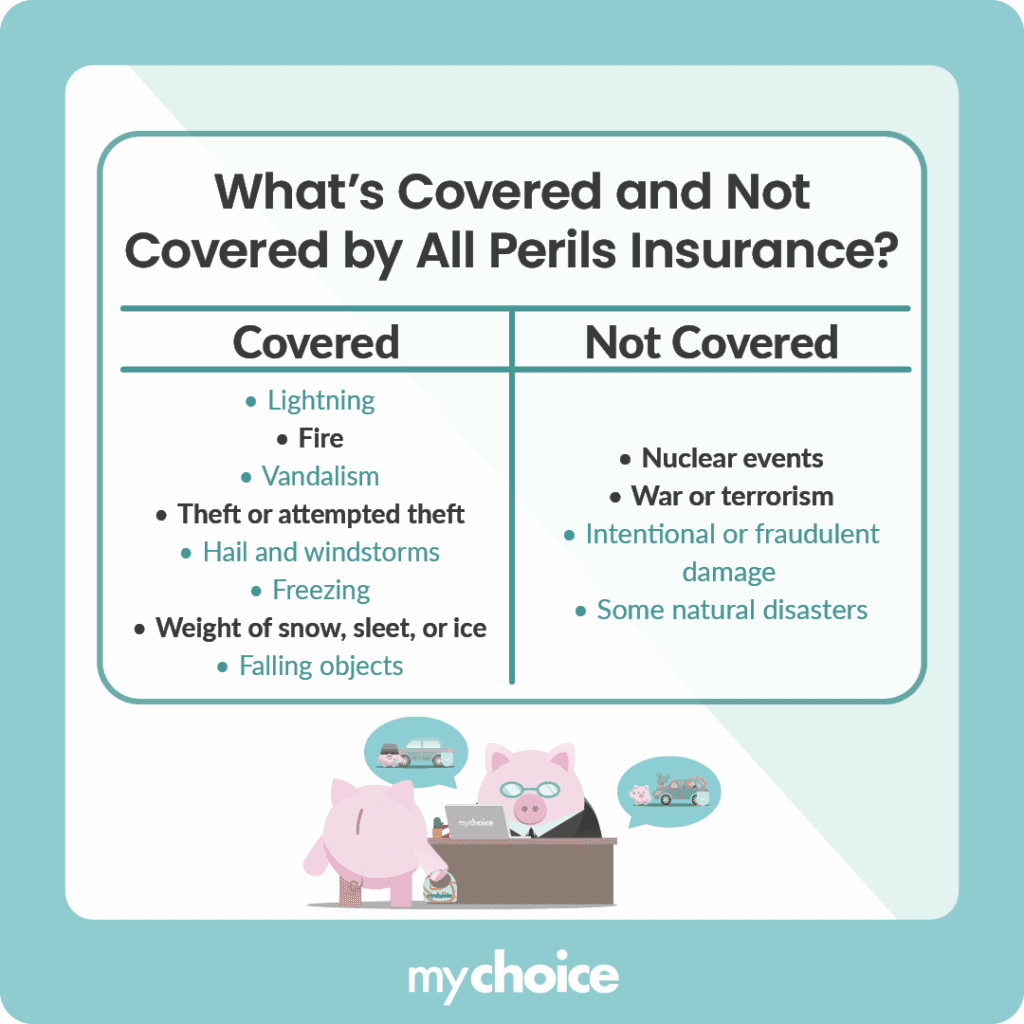

What Perils Are Covered By All Perils Insurance?

Examples of events commonly covered by all perils coverage include:

- Lightning damage

- Fire

- Vandalism

- Theft or attempted theft

- Hailstorms

- Windstorms

- Freezing

- Damage caused by the weight of sleet, snow, and ice

- Falling objects, such as tree branches or bricks

Note that the following risks are typically excluded by all perils coverage:

- Nuclear disasters (ex: plant meltdown)

- Terrorism and war

- Intentional or fraudulent damage or loss

- Some natural disasters, such as earthquakes and tsunamis

Is A Peril Different From A Risk?

Yes. A peril refers to the cause of the damage or loss, while a risk refers to the chance of sustaining a loss or damage due to a peril. However, note that insurance companies use these terms interchangeably.

How Much Is All Perils Coverage?

Because all perils coverage is so extensive, it will cost more than other forms of car insurance. However, the final estimate for your premium will depend on other factors, such as your driving history, the car being insured, and your insurer.

Insurers provide different quotes depending on these factors, so don’t forget to compare quotes before taking out a car insurance policy. This will help you choose the best option for your car needs and budget.

Should I Get All Perils Insurance?

Getting all perils insurance coverage can give you peace of mind as it covers most risks that would damage your car. However, it’s more expensive than other car insurance coverage types, so you may opt for less coverage to lower your insurance premiums. Ultimately, getting this kind of coverage depends on how much risk you’re willing to tolerate.

Whether you get all perils insurance or a different car insurance coverage, it’s important to shop around to get the best deal. You can use the comparison tool here on MyChoice to see how much all-risk coverage would cost from different insurance companies.

Key Advice from MyChoice

- All perils coverage may be worth considering for newer or high-value vehicles, where repair or replacement costs can be high.

- Compare all perils coverage with separate collision and comprehensive policies, since the cost difference may not always be large.

- Check your policy exclusions carefully, as certain events such as war, terrorism, or intentional damage are typically not covered.