Electric vehicles (EVs) are growing in popularity due to their lower running costs, efficiency, and a host of other reasons. However, some people are still on the fence about the insurance cost of EVs. Are EVs actually more expensive to insure than gas-powered cars?

That’s what we’re here to answer. In this study, we analyzed data collected from mychoice.ca in 2025 to compare popular electric vehicle models with gas vehicles occupying similar niches among Ontario drivers. If you’re still torn between buying an EV and a gas vehicle because of insurance costs, we hope this helps you make an informed decision.

Methodology

For this study, we analyzed over 60,000 Ontario auto insurance quotes collected through MyChoice.ca, our online insurance comparison platform.

We compared multiple car models across three niches: Compact/Entry, Compact SUV, and Luxury SUV. This ensures we cover a good range of car type preferences.

For consistency, we focused on a standard driver profile: A 35-year-old married driver (male or female), fully licensed, and with a clean driving record. The driver owns the car outright and is looking for both comprehensive and collision coverage to ensure maximum insurance protection.

An Insurance Cost Comparison Between Popular EV and Gas Vehicles

With federal programs like the Incentives for Zero-Emission Vehicles (iZEV) and additional perks for businesses using EVs, the Canadian government continues to encourage electric vehicle adoption. While these incentives reduce the purchase price of EVs, they don’t address one of the most important ongoing costs of ownership – auto insurance.

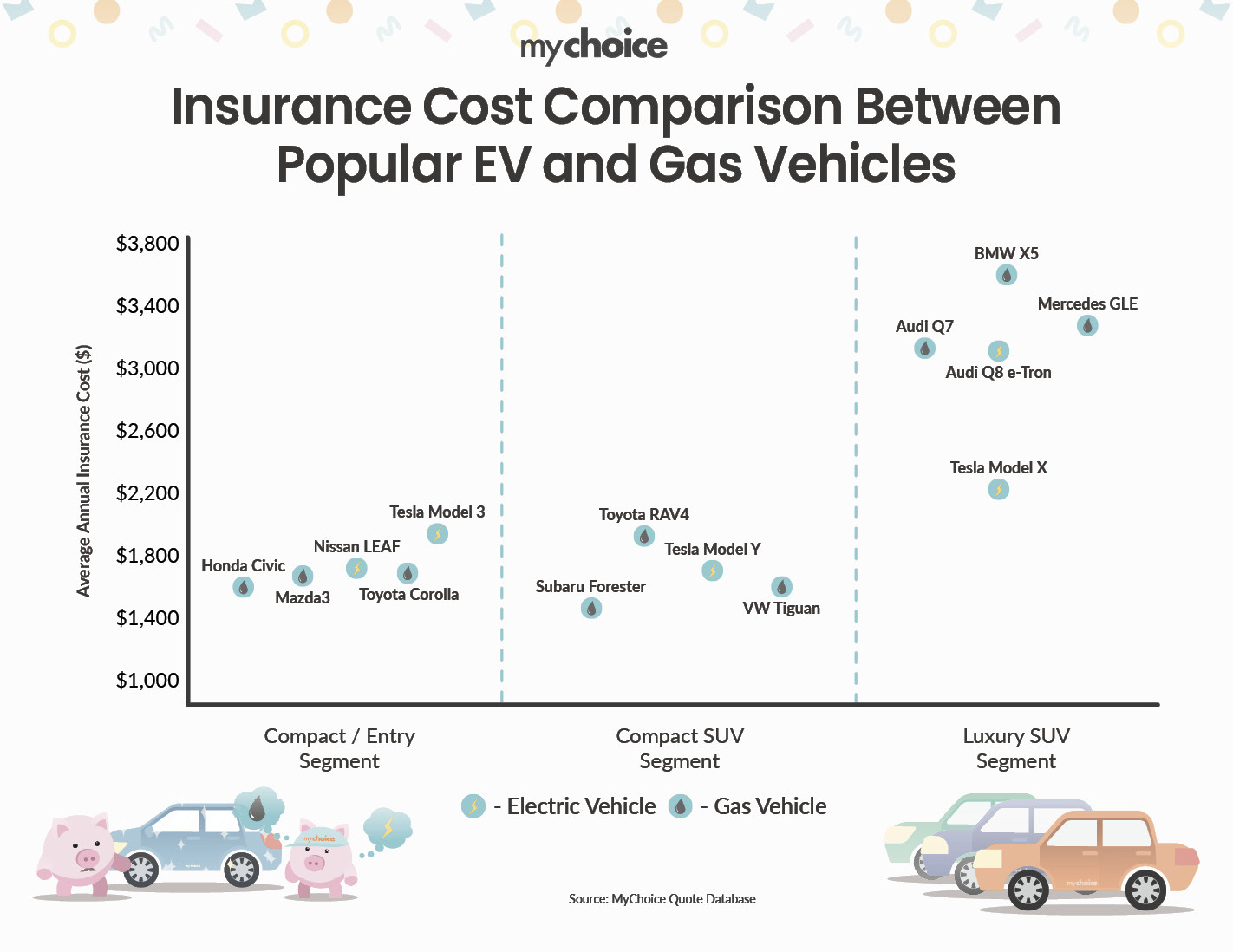

Compact / Entry Segment

| Car Model | Annual Insurance Cost |

|---|---|

| Tesla Model 3 (EV) | $1,776 |

| Nissan LEAF (EV) | $1,893 |

| Honda Civic (Gas) | $1,553 |

| Toyota Corolla (Gas) | $1,689 |

| Mazda3 (Gas) | $1,682 |

In the compact segment, EVs are clearly more expensive to insure than their gas-powered counterparts. The Tesla Model 3 costs about $223 more per year to insure than the Honda Civic, while the Nissan LEAF is roughly $340 more expensive than the Civic.

Even compared to higher-priced gas models in this category, the gap remains noticeable. The Model 3 costs about $87 more than the Toyota Corolla and roughly $94 more than the Mazda3. This shows that even when EVs compete directly with popular, mainstream sedans, their insurance premiums remain higher.

Compact SUV Segment

| Car Model | Annual Insurance Cost |

|---|---|

| Tesla Model Y (EV) | $1,746 |

| Subaru Forester (Gas) | $1,424 |

| Toyota RAV4 (Gas) | $1,843 |

| VW Tiguan (Gas) | $1,537 |

The compact SUV segment shows a more mixed picture. The Tesla Model Y is about $322 more expensive to insure than the Subaru Forester and $209 more than the VW Tiguan. However, it is actually $97 cheaper to insure than the Toyota RAV4.

The Model Y still sits toward the higher end of the segment, even if it narrowly undercuts one of the most popular gas SUVs in Canada.

Luxury SUV Segment

| Car Model | Annual Insurance Cost |

|---|---|

| Audi Q8 e-Tron (EV) | $3,114 |

| Audi Q7 (Gas) | $3,189 |

This is one of the rare cases where the gas-powered vehicle is slightly more expensive to insure than the EV. The Audi Q7 costs about $75 more per year than the Audi Q8 e-Tron.

It shows that insurance pricing isn’t driven purely by powertrain type. Vehicle value, repair complexity, and claim severity often matter more than whether a car is electric or gas-powered.

| Car Model | Annual Insurance Cost |

|---|---|

| Tesla Model X (EV) | $2,263 |

| BMW X5 (Gas) | $3,626 |

| Mercedes GLE (Gas) | $3,313 |

In this comparison, the gas-powered luxury SUVs are dramatically more expensive to insure than the EV. The BMW X5 costs about $1,363 more per year than the Tesla Model X, and the Mercedes GLE is roughly $1,050 more.

At this level of the market, insurance pricing is driven far more by vehicle price, theft risk, and repair costs than by fuel type alone.

What We Can Take Away From These Comparisons

While the data shows that EVs are often more expensive to insure than gas-powered vehicles, it’s not a universal rule. In most mass-market segments, EVs still carry higher premiums, but in luxury categories, the relationship can reverse entirely.

This means that any savings from fuel efficiency or government incentives can be partially offset by insurance costs. For many buyers, insurance becomes one of the highest hidden costs of EV ownership.

EVs still make financial sense for many Canadians, especially when long-term operating savings are considered. However, insurance pricing needs to be treated as a core part of the total cost of ownership, not an afterthought, when deciding whether to go electric.

Why Are EVs More Expensive to Insure in Ontario?

EVs can be more expensive to insure in Ontario, but not because they crash more or are prone to accidents. Let’s take a look at several key factors that make EV insurance expensive:

Note that even with those factors, EVs aren’t automatically more expensive to insure in Ontario. Insurance premiums for most mainstream EV models are usually comparable to those of gas vehicles. However, the cost rises for higher-end models, especially those with complex repairs. Another factor that may cause higher EV insurance rates is a higher number of insurance claims. The high insurance cost gap between high-end EVs and comparable gas vehicles is what you should factor into your purchase decision.

What You Can Do to Lower Your Insurance Costs as an EV Owner in Ontario

With a good feel of how auto insurance costs for EVs can be more expensive than gas vehicles, it’s a good idea to keep your rates down. Here are some top tips to minimize your insurance costs:

Key Advice from MyChoice

- Before buying an EV, consider insurance costs, which are generally more expensive than those for gas vehicles.

- If you decide to buy an EV, take steps to reduce your insurance costs, such as raising your deductible and installing anti-theft devices.

- Shop around for insurance policies with MyChoice to ensure you get the best deal for your EV auto insurance.

- Explore our list of the top 10 electric cars in Canada to see which models offer the strongest overall value once insurance is taken into account.