A Large Population Means More Cars on the Road

With a population of roughly six million people, there will be a significant number of cars on the city’s roads at any given time. Therefore, there is a higher likelihood of an accident resulting in an insurance claim. Since insurance companies base their rates on historical trends in a given area, you will likely be made to pay for others’ mistakes even if you are a safe driver yourself.

Large Cities Attract Visitors From Around the World

On their own, congested highways increase the risk of an accident simply because there are more chances for one to happen. However, the risk of an accident increases even more when you consider that a tangible portion of those navigating Toronto’s highways isn’t native to the city.

These drivers may have little experience changing lanes, merging onto a highway, or taking other basic actions, leaving little room for error.

Fraud and Theft Are More Common in Urban Areas

Insurance fraud may not be something that you think about when shopping for auto coverage. However, when insurance companies lose money due to fraudulent claims, they recoup those losses by raising premiums for their other customers.

Toronto ranks above the provincial average for hijacking, with an average of 3.32 cars stolen per 1000 drivers each year.

How Good is Your Driving Record?

If you have recently gotten into an accident, received a traffic citation or filed a claim for any reason over the last six months, it could result in higher auto insurance premiums.

You may also be subject to a higher premium if you have been convicted of impaired driving at any point. Younger and new drivers with limited insurance and driving history usually pay higher premiums.

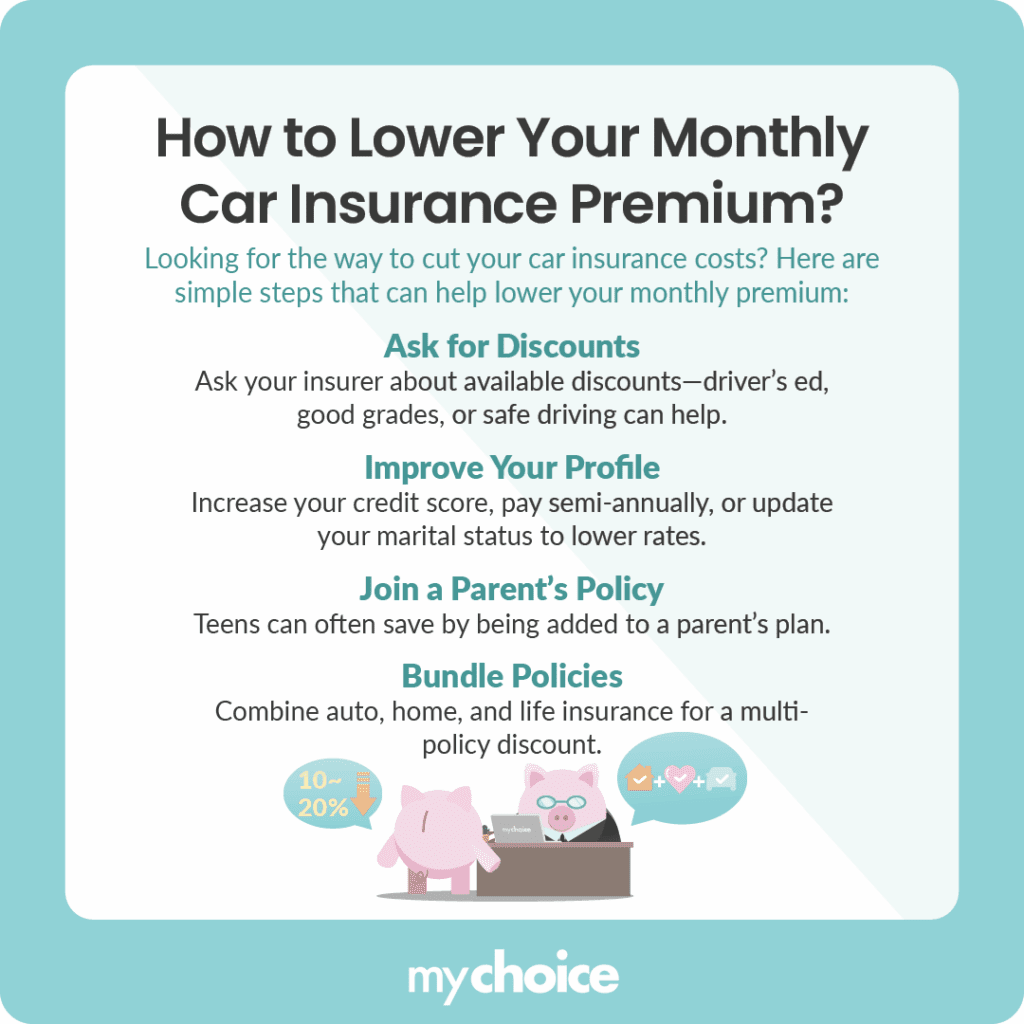

What Steps Can You Take to Reduce Your Monthly Premium?

The easiest way to reduce your car insurance premium is to ask your insurer about any available discounts.

In Ontario, the most significant savings come from bundling home and auto (or tenant/condo) insurance, which typically triggers a discount of 10% to 18%.

Choosing a less expensive vehicle that is cheaper to insure can also drastically reduce your auto insurance premiums.

Review Your Policy on a Regular Basis

It’s a good idea to review your policy every few months to make sure that you don’t have more protection than you need. When reviewing your policy, be aware of major regulatory shifts.

Since 2024, you can opt out of Direct Compensation-Property Damage (DCPD) coverage to save money, but this means you receive zero compensation if your car is damaged by another driver.

Additionally, effective July 1, 2026, most accident benefits (like income replacement) will become optional add-ons rather than mandatory inclusions.

Key Advice from MyChoice

- In Toronto, moving even a few blocks into a new postal code can change your rate by hundreds of dollars. Always get a fresh quote if you move within the city.

- While you might drop collision coverage on an old car, always carry at least $1 million to $2 million in Third-Party Liability. With the 2026 reduction in mandatory accident benefits, the risk of being sued for damages after a crash is expected to increase.