How Much Does It Cost to Cancel Car Insurance?

On average, it can cost you 2% to 7% of your car insurance premium to cancel your policy before the renewal period. However, these charges can vary depending on the following factors:

- Any outstanding premium payments

- Non-refundable provider fees

- The time remaining on the term of your policy

Generally, the closer your cancellation date is to your renewal date, the lower the cancellation penalty because the insurer has already earned more of the premium. Read the fine print to see what fees are incurred if you cancel before that date and what requirements you need to submit for your policy cancellation.

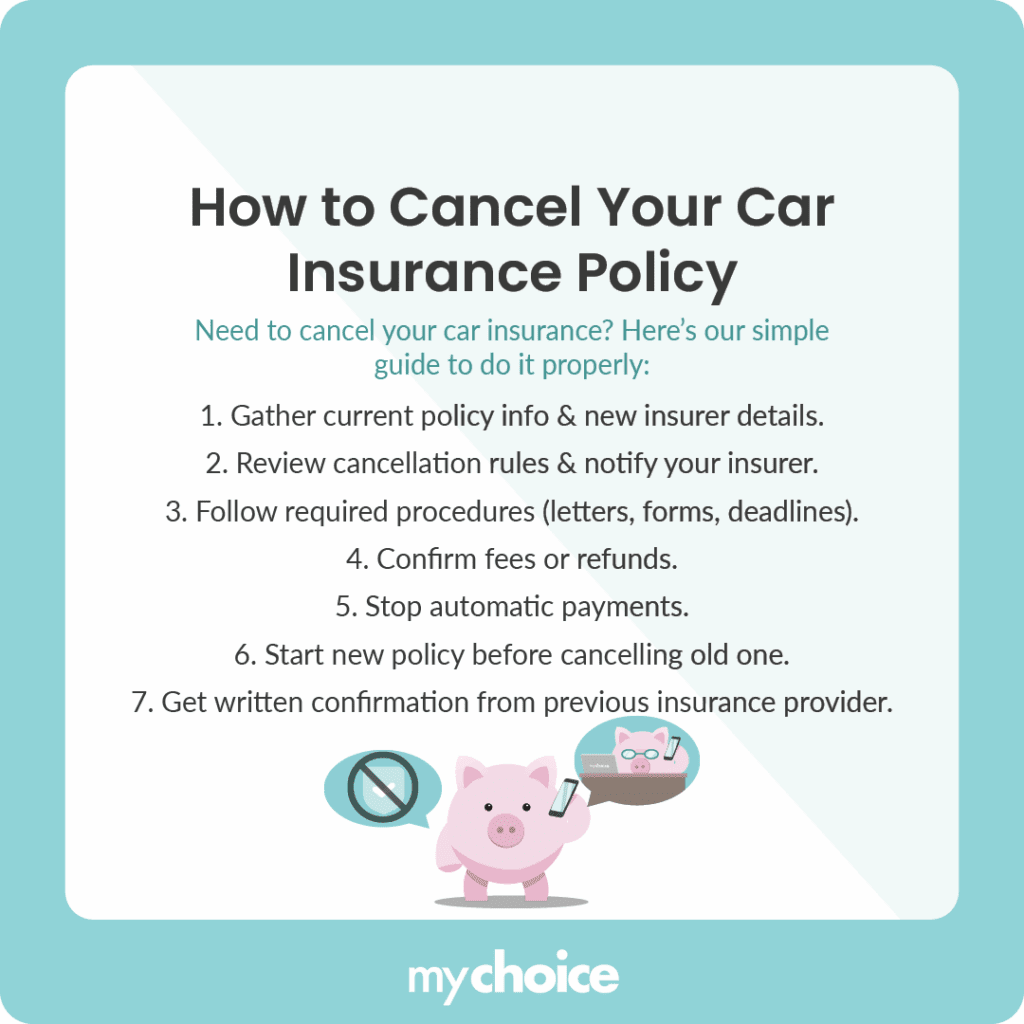

How to Cancel Your Car Insurance Policy

Planning to cancel your car insurance policy? Here are the steps that you need to follow:

Can I Get a Refund on My Car Insurance Policy?

If you paid your premiums upfront, you may receive a refund for the unused portion of the policy after cancellation, depending on the insurer’s cancellation method. You’ll be refunded the amount for the months you paid in advance. If you pay monthly, you may still owe outstanding premiums or cancellation charges depending on the insurer’s short-rate cancellation rules.

Companies will compute your refund either through short-rate cancellation or pro-rated cancellation. Here’s the difference between the two:

- Short-rate cancellation: You’ll receive part of your initial premium, but your car insurer will charge you a cancellation fee for cancelling your policy early. They may also deduct additional administrative fees.

- Pro-rated cancellation: You’ll receive a refund based on the remaining months you already paid for. E.g. if you paid for a year of coverage but cancelled four months before the renewal date, you’ll be refunded for that remaining time.

Can I Cancel My Car Insurance Without Incurring Charges?

Yes, you can cancel your car insurance without incurring extra charges by cancelling during your renewal period. It’s best to inform your insurer ahead of time that you’ll be cancelling your policy effective on the renewal date.

Can My Insurer Cancel My Car Insurance Policy?

Yes, your insurance provider can cancel your car insurance policy if you’ve missed payments, given misleading information related to your car insurance policy or paid past the due date.

Avoid headaches by paying for your policy on time. If you notice that you missed a payment or you received a late payment reminder from your insurer, address this by paying for it immediately. Note that some providers will charge late payment fees, while others may raise their rates or refuse to renew your policy when it’s up.

Can I Cancel My Car Insurance Policy With an Open Claim?

Yes, you can cancel your car insurance policy even with an open claim. However, note that you’ll still need to complete the claim and must pay cancellation fees to your insurer. A claim should also be disclosed to your new insurance provider, which can affect the rates they offer. Non-disclosure of your claim with your old provider can lead to the cancellation of your new policy.

Common Reasons to Cancel an Existing Car Insurance Policy

These are the most common reasons why drivers cancel their car insurance policies, even if they have to pay cancellation charges:

- More affordable premiums: You may have found a good car insurer that offers lower rates for the same level of coverage.

- Discounts by bundling: A car and home insurer may be offering a good discount if you get them to insure both your house and your car. Alternatively, you may have decided to get a multi-car insurance policy with a spouse or family member because it results in cheaper premiums.

- No more car to cover: You may have decided that you don’t need a car anymore, so the policy is equally unnecessary.

- Poor customer service: You may simply be unsatisfied with the way your insurer handles claims, customer concerns, and queries.

Key Advice from MyChoice

- Always secure a new policy before cancelling your existing one. Even a short gap in coverage can lead to higher premiums when you apply for insurance again.

- Check cancellation fees before switching insurers. In some cases, the penalties for cancelling early may outweigh the savings from switching providers.

- Consider cancelling at renewal whenever possible. Doing so can help you avoid short-rate penalties and additional administrative fees.

- Compare quotes with MyChoice before cancelling your current policy. Shopping around may help you find better coverage or lower premiums without unnecessary cancellation costs.