Why EV Write-Off Rates Are Increasing

Price parity between gas-powered vehicles and electric vehicles (EVs) may be upon us sooner than experts predicted. This is not only because EV prices are coming down, but also because the average price of gas-powered and hybrid vehicles is rising. Add in the return of federal government EV rebates as well as the price pressure of upcoming Chinese imports, and this gap will continue to narrow over the next couple of years.

This is good news for up-front EV affordability, but it has insurance implications. Lower new vehicle prices and increased supply are contributing to declining used EV values — with EVs experiencing faster recent depreciation than gas-powered vehicles.

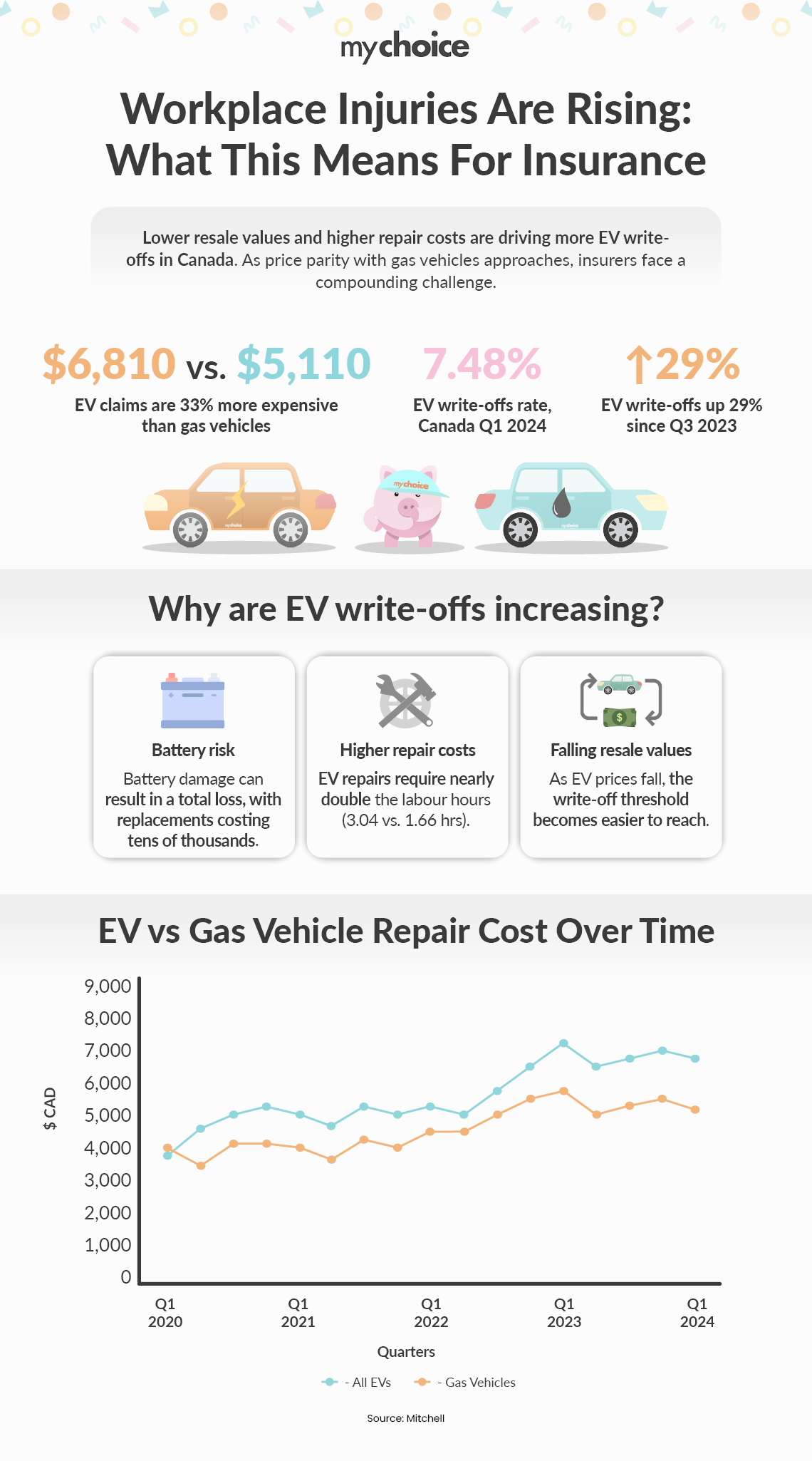

EVs are also prone to greater claim severity than gas cars. According to the most recent report from Mitchell, North America’s largest provider of collision repair information, EV average claim severity in Canada was $6,810 in Q1 of 2024 for EVs and $5,110 for gas cars, a 33% difference.

As insurers contend with lower resale values and higher repair costs, EVs are being written off more often than they once were.

Mitchell’s data shows the electric vehicle write-off rate in Canada was 7.48% of claims in the first quarter of 2024, an increase of 7% over the previous quarter and 29% from the quarter before that.

If your vehicle is declared a total loss, it’s important to understand your options. Learn how to handle a vehicle write-off situation.

Are EVs Written Off More Often than Gas Cars?

While EV write-off rates have increased, they remain broadly in line with comparable newer gas-powered vehicles. Mitchell’s data shows ICE vehicles from model 2021 and newer have similar write-off rates to EVs at 9.51% in the U.S. in the first quarter of 2024 (as opposed to 9.93% of EVs) and 7.44% over the same period in Canada (versus 7.48% of EVs).

What Causes an EV to be Written Off?

The most expensive and critical component of an EV is its battery. Following a collision, any battery damage is likely to result in the whole car being scrapped. Battery packs can’t be repaired, and replacements can cost tens of thousands of dollars. This is especially true of certain Teslas where the battery is mounted as a structural component of the vehicle and is therefore very complicated to replace.

On top of this, EVs cost more to repair than ICE cars on average because they require more labour. According to Mitchell’s data, EVs require 3.04 billable repair hours on average versus 1.66 hours for ICE vehicles. This is partly due to the extra handling required for the battery even when it’s not damaged as it needs to be fully de-energized and sometimes removed from the vehicle entirely to protect it during repairs. This can cause claim severity to be a higher percentage of the car’s total value, increasing the likelihood that repair costs exceed the vehicle’s value, resulting in a write-off.

What Does this Mean for Insurance Premiums on EVs?

EV insurance premiums in Canada already tend to be higher than those for similar ICE vehicles. These trends could put upward pressure on EV insurance premiums, although declining vehicle values may partially offset that impact.

“What we’re seeing is a shift in how insurers evaluate EV risk,” said Aren Mirzaian, CEO of MyChoice. “Higher repair complexity is pushing claim costs up, while faster depreciation is pulling total loss values down. That combination makes EV pricing more volatile and harder to predict — both for insurers and for consumers.”

Key Advice from MyChoice

- Understand depreciation risk, not just purchase price. EVs may lose value faster than expected, which can directly impact how much you receive in a total loss claim.

- Consider a waiver of depreciation (OPCF 43 in Ontario). This coverage ensures you receive the original purchase price (or replacement cost) if your vehicle is written off, protecting you from rapid early depreciation.

- GAP insurance may be even more important when you purchase an EV. If your vehicle is written off after a collision soon after you buy it, GAP insurance will cover the difference between what you still owe on it and what it’s worth when written off.