The guide below is based on the Insurance Bureau of Canada’s guidance on repairs, replacements and write-offs, including how salvage value factors into the write-off decision. We examined the OPCF 43 (Waiver of Depreciation) endorsement and its three payout benchmarks, and drew the tax treatment of a written-off business vehicle from the Government of Canada’s 2026 automobile deduction limits and CRA motor-vehicle expense rules.

Keep reading to learn how your car’s value is calculated, what OPCF 43 does and doesn’t pay, what happens when the settlement is smaller than your loan balance, and how theft and ADAS recalibration costs can tip a car into total-loss territory.

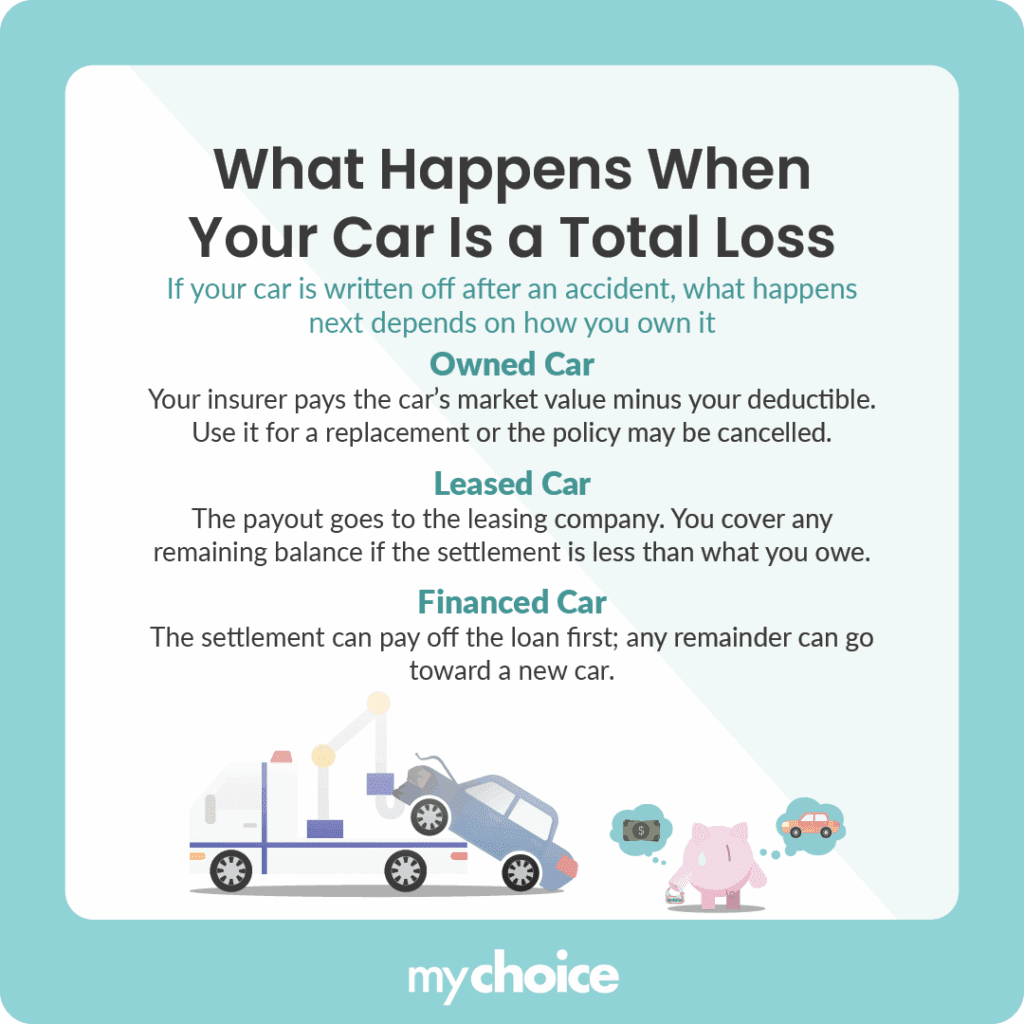

What Happens if Your Car Is Deemed a Write-Off?

If your car is deemed a write-off, your car insurance company will offer you a settlement check equivalent to the car’s value at the time of the collision. Here’s how your car is assessed by your appraiser and deemed a write-off:

- An appraiser from your car insurance company will compute how much your vehicle was worth before the accident. Note that this value may have gone down due to depreciation, which is one of the hidden costs of owning a car.

- Insurers calculate a total loss ratio by dividing the estimated cost of repairs by the vehicle’s actual cash value (ACV). Ontario doesn’t legislate a fixed cut-off. The 70% to 80% trigger you’ll often see quoted reflects common insurer practice, not a rule, and each company sets its own threshold based on where repairs plus expected salvage value land against the ACV.

- The appraiser decides if your car will be written off or repaired.

- If the appraiser deems your car still worth repairing, your car insurance policy will be used to cover the cost of repairs. However, if your damaged car’s estimated cost of repairs and salvage value exceeds your car’s pre-accident cash value, it will be written off.

- If your car is deemed a write-off, your car insurer will give you a settlement offer a settlement based on the car’s cash value.

After your damaged car is written off, it may be branded “irreparable” or “salvage”. Irreparable cars can never be repaired and driven on the road – they can only be used for parts. Salvage cars need repairs and inspection before they can be allowed on the road again. In Ontario, these brands are assigned under the Ministry of Transportation’s vehicle branding program (Highway Traffic Act). A salvage-branded vehicle must pass a structural inspection and be re-registered as “rebuilt” before it can legally return to the road.

Sometimes, insurers allow you to keep your damaged car as part of the write-off settlement if it has no safety or structural issues.

What You Can Do if Your Car Is a Write-Off

If your car is deemed a write-off, you may want to use the settlement cheque to cover the cost of a new car or dispute the company’s assessment. Here’s a quick breakdown of how each works:

- You can use the settlement cheque to purchase a new car, but this cheque will represent the depreciated value of your car, not its original purchase price. Cars start depreciating as soon as you drive them off the lot, so in many cases, your settlement cheque may not be enough to buy a similar, brand-new vehicle.

- With an active OPCF 43 endorsement, your insurer will pay the lowest of three specific amounts: the actual purchase price, the manufacturer’s suggested list price (MSRP) at the time of purchase, or the cost of a brand-new, similarly equipped replacement vehicle.

- If you accept that your car should be written off but disagree with the settlement amount offered, you can present your own list of similar vehicles and their values to your car insurer.

- If you think your car shouldn’t be written off and can still be repaired, you need to talk to your car insurance company. You’ll need to show evidence that the car will be safe to drive after repairs, as well as a lower estimate that makes the car worth repairing.

How Does a Car Insurance Company Determine My Car’s Value?

A car insurance company determines the value of your car by considering the following factors:

- Your car’s make, model, year, and odometer reading

- Engine type

- Overall interior and exterior condition, taking into consideration any prior damage

- Values for similar vehicles listed in industry publications, classified ads, and used car valuation databases, such as the Canadian Automobile Red Book

Newer and well-maintained cars usually get a higher assessed value, and the larger the amount you’ll get if it’s written off.

An Example of What the Settlement Math Looks Like

The figures below are used for illustrative purposes and don’t reflect a real quote. Your appraiser prices your specific car against comparable listings and guides like the Canadian Red Book, but the mechanics are exactly what happens in an Ontario total-loss file:

| Line item | Amount |

|---|---|

| Purchase price (three years ago) | $38,000 |

| ACV at the time of the loss (from comparable listings) | $26,000 |

| Repair estimate | $19,500 |

| Salvage value | $4,000 |

| Repairs + salvage vs. ACV | $23,500 vs. $26,000 (≈90%) — written off |

| Settlement: ACV minus $1,000 deductible | $25,000 |

| Loan balance still owing | $29,000 |

| Shortfall you owe the lender without GAP coverage | $4,000 |

That last line is the one that surprises people. The settlement cheque goes to the lender first, and if you’re underwater, you keep making payments on a car you no longer own. That shortfall is exactly what GAP insurance covers, and what OPCF 43 helps prevent on a newer vehicle by excluding depreciation from the payout.

My Car’s Damage Wasn’t Too Serious, Why Was It Written Off?

Even if the damage to your car doesn’t appear too serious, your car insurer may write it off and instead hand you a cheque due to the cost of recalibration.

Because of the increasing sophistication of automotive technology, many vehicles have sensitive electronic sensors that require recalibration during repairs. Recalibration can take tools, specialized knowledge, and more time to repair. Most of this comes down to advanced driver-assistance systems (ADAS). On many newer vehicles, even a windshield swap or a bumper repair requires camera or radar recalibration, and collision-industry estimates from Mitchell show calibration line items appearing on a growing share of repair bills.

Read More: How ADAS is Redefining Claim Severity in Car Insurance

If your car insurer considers the cost of repairs and recalibration too high, they may write your car off instead.

What if I Want My Car Repaired Instead of Written Off?

If you want your car repaired instead of written off, you need to talk to a representative from your car insurance company to reevaluate the claim.

If your car’s damage was minor and the car insurance company considers it worth repairing, the insurance company will typically:

- Cover the cost of repairs related to the accident

- Oversee your vehicle’s repairs at one of their preferred auto shops

- Expect you to cover any additional costs for part replacements if they’re better than your car’s parts before the accident

In most cases, car insurance companies refuse to repair a vehicle if there’s a safety issue that’s too serious or costs too much for them to repair.

What if I Want My Car Written Off and Not Repaired?

If you want your car written off and not repaired, you can disagree with your car insurance company’s appraisal of the cost of repairs. You have to provide a repair cost estimate high enough for the company to deem the vehicle too expensive to repair at any of its preferred shops.

Apart from the cost of repair, you should be able to show that the car is no longer safe to drive even after repairs and replacements. Typically, when a car insurance company sees too many safety issues, it will write off the car instead of covering repairs. Review your claim with a representative from your insurer to determine if the car is too expensive to repair or too risky to put back on the road.

What if I Want My Car Repaired at a Different Shop?

If you want your car repaired at a different shop, you’ll need to get an estimate for parts and labour approved by your insurer. Here are things to keep in mind if you want your car repaired at your preferred mechanic or shop instead of your car insurer’s preferred shops:

- Ask the shop for a written estimate for repairs, inclusive of labour and replacement parts.

- Get the estimate approved by your insurer.

- Once your car insurer approves this estimate, sign it with the mechanic of your trusted shop.

- Keep reviewing the process of your car’s repairs and any suggested recommendations from your shop’s mechanic. Note that during repairs, your mechanic may suggest additional upgrades like brake replacement or updating the exhaust. However, these additional repairs won’t be covered by your insurer.

Is a Written-Off Car a Taxable Expense?

Yes, a written-off car can be a taxable expense if you used it to earn business income. The types of claims you can make on your car are:

- Insurance

- Maintenance and repairs

- License and registration costs

- Fuel and oil costs

- Leasing costs, if applicable

- Interest on money borrowed to purchase the vehicle

- Capital cost allowance, if you own the vehicle

You can deduct only reasonable motor vehicle expenses with receipts to back them up. Make sure that if you also use your vehicle for personal purposes, the only deductible expenses are those incurred for business. (Source: Canada Revenue Agency, motor vehicle expense rules.)

For 2026, the ceiling for capital cost allowances (CCA) for Class 10.1 passenger vehicles has increased to $39,000 before tax, and the maximum allowable interest deduction remains at $350 per month for new automobile loans. These ceilings are set federally and revised each January. For reference, the 2025 Class 10.1 ceiling was $38,000. That’s why you should confirm the current prescribed amounts on canada.ca for the tax year you’re claiming it.

Is My Car Declared a Total Loss When It’s Stolen?

If your car is stolen and not recovered, your insurer will typically declare it a total loss and pay out a settlement based on its actual cash value. Even if the vehicle is recovered but severely damaged — such as being stripped for parts or re-registered with a different VIN — it may still be written off.

In fact, the Équité Association’s First Half 2025 Auto Theft Trend Report recorded 23,094 private passenger vehicles stolen in Canada in the first six months of 2025, with many of these cases linked to organized crime tactics like chop shops and re-VIN operations, which reduce recovery chances and increase the likelihood that insurers classify the vehicles as total losses.

What Insurance Coverage Do I Need to Be Protected Against a Total Loss?

To be protected against a total loss, you need both comprehensive and collision coverage. Both types of coverage cover vehicle repairs or replacements up to the vehicle’s actual cash value in the case of collisions with vehicles or objects, as well as other unexpected situations. You can also bundle both of these insurance protection packages into all-perils coverage.

Coverage Add-Ons That Can Reduce the Costs

In addition to collision and comprehensive coverage, there are two add-on insurance protection options that can soften the blow of your car getting totalled: