When to Make a Car Accident Claim

The best times to make a car accident claim are when:

- You cause significant damage to your vehicle or another vehicle.

- You suspect the other driver is trying to commit insurance fraud.

- You sustain an injury or cause physical harm to other drivers.

On the other hand, there are instances under which you should not file an insurance claim, such as when:

- The damage to your vehicle doesn’t significantly surpass your insurance deductible.

- You can’t afford to pay for the damage.

- The damage caused is minor.

- You caused the damage by backing into a fixture.

Additionally, if you can’t afford the insurance rate increases that come with filing a car accident claim, you might be better off shouldering the repair expenses.

How Long After an Accident Can You Make a Claim?

In Ontario, you should notify your insurance company within 7 days of the accident, or as soon as reasonably possible. However, these time frames may vary according to different insurance companies.

Many insurers recommend reporting the accident within 48–72 hours, even if you are unsure whether you will file a claim. In Ontario, you typically have two years to start a lawsuit for injuries from a car accident.

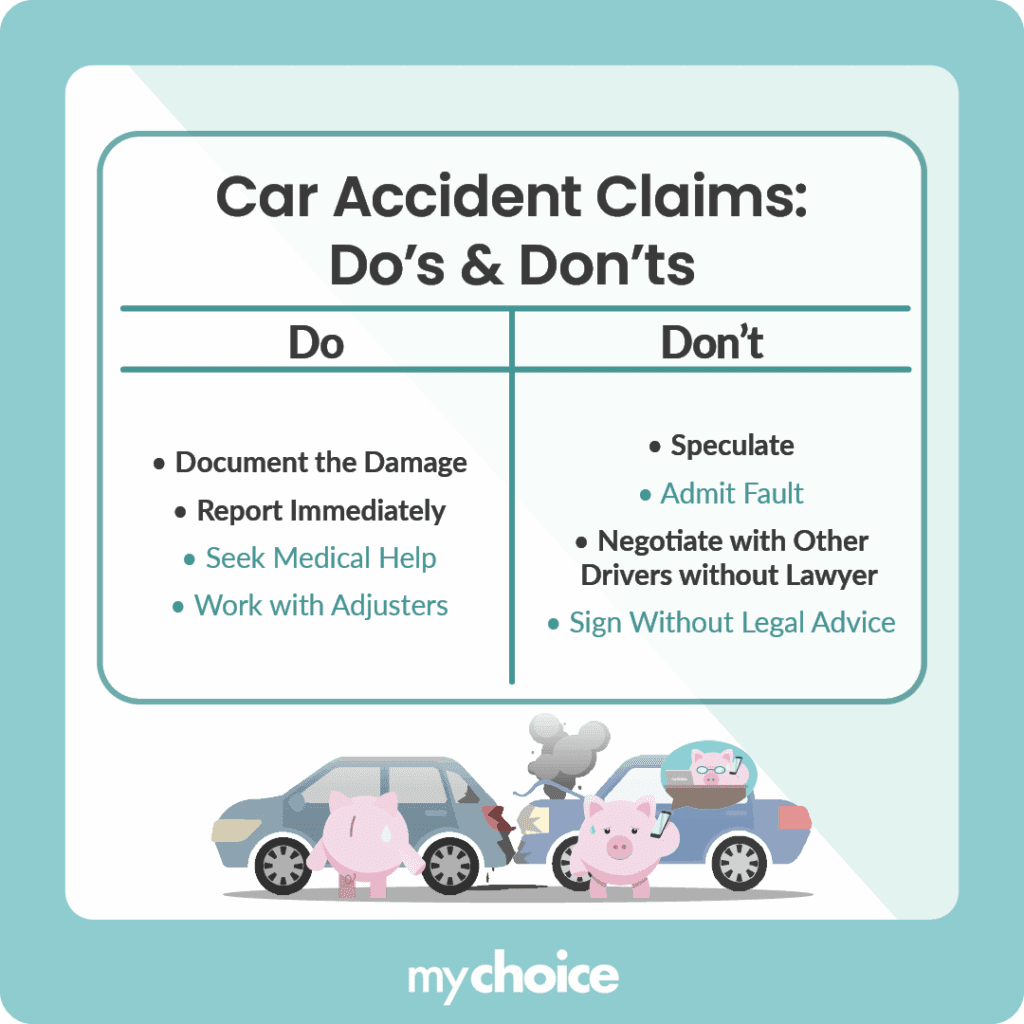

Car Accident Claims Do’s and Don’ts

There are several steps to making a car accident claim, so you’ll want to remember these dos and don’ts. Check out our guide to learn more about what to do immediately after a car accident.

The Auto Insurance Claims Process

The auto insurance claims process is more straightforward than you might anticipate. Just follow these steps:

- Pull over to a safe spot. If there is someone else in your vehicle and they are injured, do not move them. Read more about how to safely pull over onto the side of the road in our guide.

- Call 911 immediately. Then, call your insurer and provide them with as many details about the accident as possible.

- Answer any questions your insurance adjustor asks. They will provide an estimate for the damage and repairs.

- Review auto repair shops and determine your schedule.

- Settle and close the claim.

What Is Covered in Case of Injury?

Ontario auto insurance policies include mandatory Accident Benefits coverage, which provides compensation for medical expenses, rehabilitation, and income replacement regardless of who was at fault.

These settlements can cover the following:

- Income replacement

- Caregivers

- Rehabilitation or physical therapy

- Medical bills

- Compensation for other expenses like home maintenance or educational costs

If the accident results in death, your family can expect to receive monetary support for the funeral and additional living expenses.

What Your Insurance Company Pays

Insurance companies pay one of two fees:

- The cost to repair damage caused to your vehicle

- The actual cash value of your car at the time of the accident

The actual cash value refers to the cost of replacing your vehicle with another car in a similar condition. Your insurance company will review your car’s mileage, age, and overall condition to determine this cost. If investigators determine that you are at fault, you must pay your entire deductible. If you have optional coverage, here is what you can expect from the claims process.

How Claims Affect Your Insurance Rates

Drivers making a car accident claim for the first time who are not at fault won’t typically see an increase in their insurance premiums. In other situations, you might be subject to an increase depending on the damage sustained, any injuries, the claim type you file, and the fault determined.

According to MyChoice internal data, drivers in Ontario see an average premium increase of 96% after an at-fault collision.

If an insurance company finds you at fault for an accident, this can also stay on your record for a few years and impact your rates.

Where to Get Your Vehicle Repaired

When you receive compensation, you can repair your vehicle at any shop. However, your insurance company might recommend a body shop of their choice to fit the estimated budget. The benefit of employing a shop that works closely with your insurance company is that they can ensure the job is done satisfactorily.

Can You Cancel an Active Claim?

While you can cancel an active claim, it will depend on how far along the process you’re in. You can no longer cancel a claim if you’ve already received compensation. In addition, you cannot withdraw the existence of a claim on your driving record after processing it.

How Many Auto Insurance Claims Can You Make in a Year?

There is no strict limit on the number of claims you can file, but frequent claims can increase your premiums or lead to policy non-renewal. However, you’ll want to keep this number to a minimum, or else your company might suspect insurance fraud.

How Long Does it Take to File an Insurance Claim?

Filing an insurance claim can take 30 minutes to an hour, including the call to your adjustor. However, the actual settlement can take between weeks and months. Ultimately, how long it’ll take to receive your compensation depends on the damage’s extent and whether the parties involved file complaints or appeals.

What to Do if Your Claim Is Denied

Your insurance company can deny a claim. Claim denial typically happens for the following reasons:

- You provided inaccurate or misleading information.

- You were not a licenced or authorized driver.

- You were using a personal vehicle for commercial or business purposes.

- You broke the law.

- You needed to catch up on insurance payments.

- You don’t have the appropriate insurance plan.

- You committed insurance fraud.

You can contest these findings with the Automobile Accident Benefits Service or apply for a new claim appropriate to your existing coverage.

What to Do if You Don’t Have an Insurance Policy

You can still make a claim if you don’t have an auto insurance policy or are not listed secondarily on another insurance policy. Alternatively, you can get temporary insurance.

Consider the following circumstances and to whom you can submit your claims application:

| Accident Circumstance | Where to File a Claim |

|---|---|

| Driving a company vehicle | Insurance company contracted by your business |

| Passenger in an uninsured vehicle | Other driver’s insurance company |

| Passenger in someone else’s vehicle | Company that insures the vehicle |

| Pedestrian | Company that insures the vehicle at fault |

| N/A | Motor Vehicle Accident Claims Fund |

Find out more about insurance rules when you drive someone else’s car and what you should do if you can’t afford insurance.

Key Advice from MyChoice

- Report accidents to your insurer even if you’re unsure about filing a claim. Early reporting helps protect your coverage and ensures you meet insurer requirements.

- Document everything at the scene of an accident. Photos, witness information, and police reports can help support your claim and simplify the claims process.

- Maintain adequate coverage on your policy. Optional coverages like collision or comprehensive insurance can help protect you financially if an accident occurs.