An at-fault accident can affect far more than the cost of repairing your vehicle. It may change how your insurer assesses your risk, increase your premium at renewal, affect your eligibility for certain discounts or programs, and remain relevant when you apply for coverage with another insurer. Read on to learn how much one at-fault accident may increase your auto insurance in Ontario, how insurers determine fault, how no-fault insurance actually works, and how long an accident may affect future quotes.

To prepare this article, our team looked into MyChoice’s Ontario quote data for a clean driving record versus a record with an at-fault accident, then checked the insurance explanations against Ontario’s Fault Determination Rules (O. Reg. 668), the Insurance Act, and current FSRA guidance.

How Much Will My Insurance Go Up With an At-Fault Accident in Ontario?

On average, Ontario drivers see their car insurance premiums increase by 96% after a single at-fault accident.

However, the rate of your car insurance premiums’ increase after an at-fault accident will depend on several factors, such as:

- Your driving record: Generally, drivers with a clean record will have a lower premium increase compared to drivers who’ve been in multiple at-fault accidents.

- Accident forgiveness: An eligible Accident Waiver endorsement, commonly known as OPCF 39 in Ontario, may prevent the first qualifying at-fault accident from being surcharged while you remain with the same insurer. It does not erase the claim, and conditions vary.

- Cost of property damage involved: In Ontario, if your car accident involves property damage and meets specific criteria, your insurer may deem it a “minor claim” and protect your rates from increasing. To qualify for protection under insurance rules, the accident must meet the following requirements: damage to your vehicle (including associated property) does not exceed $2,000, and it is paid out of pocket by the at-fault driver, no personal injuries are sustained, and no payment is made by any insurer. Note: This rule is separate from the province’s police reporting threshold, which allows drivers to forgo police reporting for property damage under $5,000 as long as there are no injuries or damage to public property.

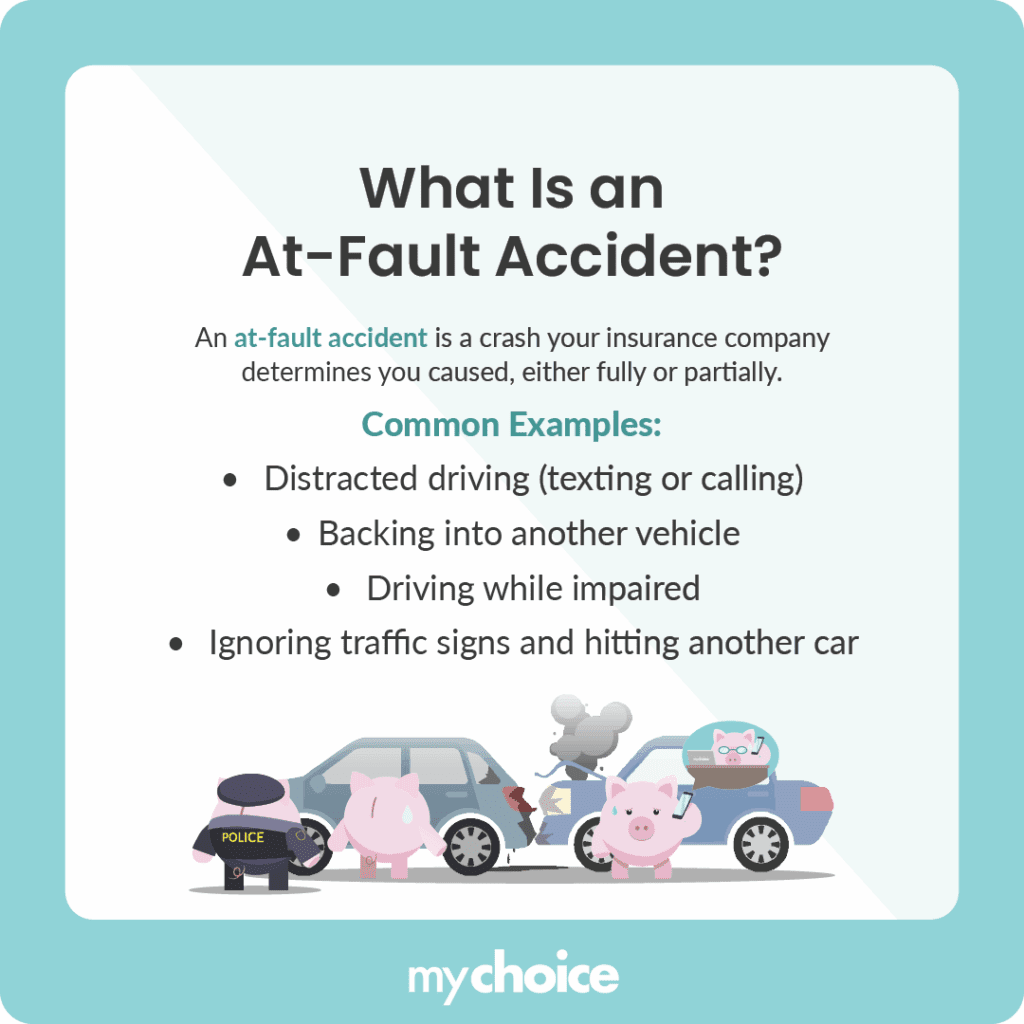

What Is an At-Fault Accident?

An at-fault accident is a car accident where your insurance company determines that you are wholly or partially responsible. This means that your actions or inactions caused the car accident to take place.

Common car accidents where you may be considered at fault include:

- Distracted driving, such as texting or calling while on the road

- Backing into another car in a parking lot

- Driving while impaired

- Colliding into another car after failing to obey traffic signs

What Is No-Fault Insurance?

No-fault insurance simply means that drivers deal directly with their respective insurance companies to settle a car accident claim, instead of having each other’s insurance companies dispute who’s responsible and who should pay. This insurance system was adopted by Ontario and other provinces to simplify the claims process and speed up the process of compensating drivers.

Despite the name, “no-fault insurance” does not mean nobody is found at fault. Insurers still assign fault under Ontario’s rules because the percentage can affect how vehicle damage is settled, whether a deductible applies, and how an at-fault loss may be treated at renewal.

While a police report may have an independent finding of fault or “no-fault” in car accidents, this is used to decide if there was a violation of the Highway Safety Act. This is not the same as your car insurance company’s findings for the claims process or future premiums.

How Will a Car Insurance Company Determine Who Is At Fault?

In Ontario, a car insurance company will assign a claims adjuster to decide who is at fault in a car accident. Your claims adjuster may do the following to establish who is responsible:

- Take statements from you and any other drivers involved

- Examine the police report

- Note physical evidence found at the scene of the accident

- Consult a collision reconstruction company for a better understanding of what happened before and during the car accident

All of the information gathered by these means will be compared by your claims adjuster to the Ontario fault determination rules. Together, these will help your insurer decide who is responsible for your car accident.

What Are Ontario’s Fault Determination Rules?

Ontario’s Fault Determination Rules, a regulation under the Insurance Act, set out written and illustrated collision scenarios that insurers use to assign fault. The rules apply to insurance claims independently of any traffic charge or civil lawsuit.

Apart from covering collisions on roads and highways, the rules also have guidelines for collisions at parking lots and intersections. The act also outlines how to apply these rules in circumstances that aren’t covered by the diagrams.

Using these rules and the fact-finding means listed above, car insurance claims adjusters determine which driver is responsible for an accident.

While 0%, 50%, and 100% are the most common assignments, Ontario’s percentage-based system also allows adjusters to assign fault in increments of 25% and 75% in shared responsibility scenarios, such as specific intersection or lane-change collisions.

If I’m Not At Fault, How Much Does Insurance Increase After an Accident?

If you’re found to be wholly not at fault (0% responsible) or at least less than 25% at fault for a car accident, it’s unlikely that your car insurance premiums will increase. However, even if you’re found to not be at fault, you’ll still have to file a claim with your insurer to cover any vehicle damage and the cost of medical care.

How Long Does a Car Accident Stay on My Driving Record in Ontario?

An accident itself does not add demerit points. Points are added only if the driver is convicted of an offence, and Ontario demerit points generally remain on the driver’s record for 2 years from the date of the offence. That government driving record is separate from an insurer’s claims and underwriting history.

Insurers separately consider at-fault accidents, claims, convictions, and other rating information. The period they ask about can vary by insurer and by the type of event, so do not assume the two-year demerit-point period determines how long an accident can affect a quote.

Many Ontario applications ask about at-fault accidents within the previous six years and Highway Traffic Act convictions within the previous three years, but underwriting questions and eligibility rules differ. Answer the application exactly as asked and confirm the relevant lookback period with the insurer or broker.

What Is Accident Forgiveness?

Accident forgiveness is an optional endorsement that may prevent a surcharge after an eligible first at-fault accident while you remain with that insurer. The accident remains on the claims history, and the endorsement does not erase traffic convictions, deductibles, or other policy consequences.

Note that accident forgiveness has the following restrictions:

- Most auto insurers won’t offer this add-on to your insurance policy unless you’ve been accident-free and claims-free for a specified period.

- Usually, only the first at-fault accident is forgiven. However, some insurers will reset your accident forgiveness after three or more years without accidents or claims.

- You may need to have been with your car insurer for a specified period.

- This feature may not travel with you if you switch car insurers.

- Accident forgiveness doesn’t keep demerit points off your record or prevent you from being charged for offences.

- It doesn’t cover insurance premium increases due to speeding tickets or other driving convictions.

Can a Pedestrian Be Found at Fault for a Car Accident?

In Ontario, the Fault Determination Rules (Regulation 668) explicitly state that the degree of fault for an insured is determined without reference to the actions of pedestrians.

While a pedestrian may be found ‘contributorily negligent’ in a separate court-based lawsuit, they are never assigned a percentage of fault under the regulated insurance rules used by adjusters to process claims and set premiums.