It’s become an all-too-familiar spring scenario in Canada: you think you’re driving over an innocent puddle, and then your vehicle is banging and shuddering like it’s fallen into a crater. Between flat tires, dented wheels, alignment issues, and suspension damage, pothole repairs can cost thousands of dollars. And the biggest headaches for drivers come when it’s time to figure out who pays the bill.

To understand who actually pays for pothole damage in Canada, our team reviewed municipal claims procedures, Ontario’s road maintenance standards under O. Reg. 239/02, insurance claim practices for collision coverage, and CBC’s analysis of municipal pothole claim outcomes. We compared when cities may be legally liable, when auto insurance applies, and when drivers are most likely to pay out of pocket.

How Pothole Damage Works at a Glance

- Pothole damage often isn’t covered. Because of strict city rules and how insurance works, most drivers can’t easily get compensated for repairs.

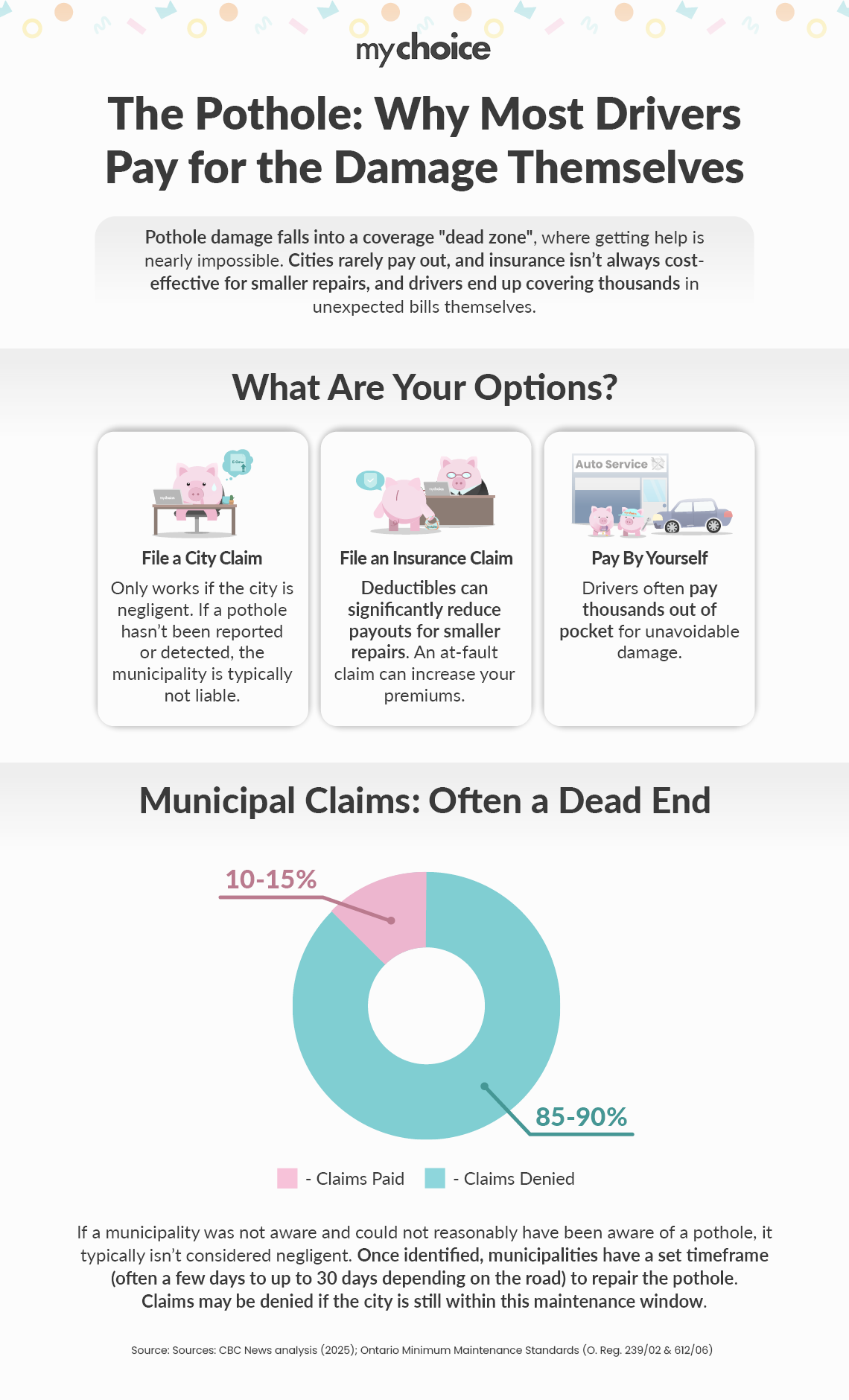

- Cities almost never pay out for pothole claims. In some Ontario cities, fewer than 10 to 15 percent of claims succeed because maintenance standards protect cities from liability.

- Timing also makes it hard for drivers. If no one has reported the pothole, the city usually isn’t responsible. Even after it’s reported, cities get a set time of up to 30 days to fix it, and claims during that period can still be denied.

- Insurance doesn’t really help with small pothole repairs. You still have to pay your collision deductible, and your premiums might go up, as it’s often considered an at-fault accident.

- Most of the time, drivers end up paying for repairs out of pocket.

Why Potholes Are a Coverage “Dead Zone”

There are three ways to attempt to pay for pothole damage, and two of them are rarely worthwhile.

One option is to file a claim for damages against the city. However, unless the municipal government can be found negligent — which is rare as it’s subject to a strict set of rules — this route is rarely successful.

Drivers can also file a claim with their auto insurance, but only certain types of coverage can be used toward pothole damage. By the time drivers factor the cost of the deductible as well as resulting rate increases, insurance can often be inefficient for smaller repairs, especially once deductibles and potential premium increases are factored in.

This creates what could be described as a ‘dead zone’ in coverage, where it’s usually drivers who end up footing the bill for these lofty and unexpected expenses.

Read More: When to File a Claim and When to Pay Out of Pocket

Filing a Pothole Repair Claim with a Municipality: The “First Driver Pays” Effect

Municipalities typically have online forms where drivers can file claims for pothole damage. However, these claims are rarely successful unless the city is found to be negligent. If a municipality was not aware, and could not reasonably have been aware, of a pothole, it typically won’t be held liable for damage.

Once a report is filed, a city has a set amount of time to fix that pothole. An Ontario regulation mandates repair times of four, seven, or 30 days, depending on the pothole’s size and location. During this repair window, additional claims are often denied if the municipality is still within its allowed timeframe to address the issue.

CBC News analyzed claim data from four cities in northeastern Ontario in 2025 — North Bay, Sault Ste. Marie, Sudbury and Timmins — and found that in some Ontario municipalities, fewer than 10 to 15 percent of pothole damage claims result in a payout for an affected driver.

The unfortunate result is if you’re among the first drivers to come across a pothole, you’re almost certainly going to pay for hitting it.

Why Insurance Doesn’t Help with Repairing Pothole Damage

When a city doesn’t pay out, drivers assume the next fallback is their insurance. But there are plenty of reasons you might want to skip going through insurance for pothole damage.

Pothole damage is claimed under collision coverage, which is the type of insurance that covers single-vehicle impacts. This type of coverage isn’t mandatory in most provinces, so if you opted out of it when setting up your auto insurance, then you’re immediately out of luck.

Read More: A Guide to Collision Coverage in Ontario

If you do have collision coverage, then you’ll need to pay your deductible to start the insurance claim. This is where things get murky: if your deductible is $1,000 and you receive a $1,400 quote for repairs, you need to assess whether proceeding through insurance is worthwhile. Pothole damage is typically treated as an at-fault collision claim by insurers, which means your premiums could increase. In fact, an at-fault claim can lead to a significant increase in your auto insurance premium, depending on your insurer and driving history. This means filing a claim for pothole damage could leave you paying much more over time than it would cost to simply cover that repair cost yourself.

What This Means for Ontario Drivers Plagued by Potholes

It’s a frustrating reality, but when there’s pothole damage to be repaired on your vehicle, in many cases, drivers end up paying out of pocket for repairs. Some incidents are completely unavoidable, but the best defence overall is to check that you’re running the correct tire pressures, give driving your full attention, and look as far down the road as possible to detect potholes early and avoid costly collisions whenever you can.