Did someone hit your car and drive off? Learn what counts as a hit-and-run, the penalties, and what you should do afterwards.

To prepare this guide, our team reviewed Ontario’s Highway Traffic Act and the federal Criminal Code and mapped the penalties associated with each. We also examined how the Insurance Act, the Ontario Automobile Policy (OAP 1), and the OPCF 44R endorsement decide which of your coverages responds when the other driver flees, and how Ontario’s Fault Determination Rules protect a not-at-fault victim’s premiums.

What is a Hit-and-Run?

A hit-and-run occurs when a driver is involved in a collision and leaves the scene without stopping, providing identification, or offering assistance if required. Drivers leave the scene for many reasons, including:

- They don’t have insurance.

- They are driving with a suspended or expired licence.

- They are worried that they caused the accident.

- They are in a rush because of an emergency.

- They were intoxicated and did not want to get pulled over for a drunk driving charge.

A hit-and-run is not the same as careless driving. Learn more about the latter in our guide.

Does Auto Insurance Cover a Hit-and-Run?

Mostly yes, but which one of your coverages goes into effect depends on what was damaged and whether the driver is ever found.

Here’s how each coverage responds when the other driver can’t be found:

| Coverage | Pays for your vehicle? | Pays for your injuries? | Works if the driver is never identified? |

|---|---|---|---|

| Accident benefits (partly optional) | No | Yes — medical, rehab, income replacement | Yes |

| DCPD (mandatory unless you opt out) | Normally yes, but not for hit-and-runs | No | No — driver must be identified and insured in Ontario |

| Collision coverage (optional) | Yes, minus your deductible | No | Yes |

| Uninsured automobile coverage (mandatory) | Only if the driver is identified but uninsured ($300 deductible) | Yes, up to the $200,000 statutory minimum | For injuries, yes; for vehicle damage, no |

| OPCF 44R endorsement (optional) | No | Yes — tops up serious injury compensation to your liability limit | Yes, with corroborating evidence |

Note that DCPD coverage applies only when the at-fault driver is identified and insured in Ontario, so it typically does not apply to hit-and-run cases where the driver is unknown.

Why Does OPCF 44 Matter Here?

OPCF 44R (aka the Family Protection Coverage endorsement) tops up your injury compensation to the same limit as your own third-party liability coverage (commonly $1 million or $2 million) when the at-fault driver is uninsured, underinsured, or never identified.

Will a Hit-and-Run Raise Your Insurance Premiums?

If you’re not at fault for a hit-and-run incident, filing a claim won’t raise your insurance rates. Fault in Ontario is assigned under the province’s Fault Determination Rules, a regulation under the Insurance Act, and insurers cannot surcharge you for a claim recorded as not-at-fault, which is why the police report matters.

Read More: How is Fault Assigned After a Car Accident

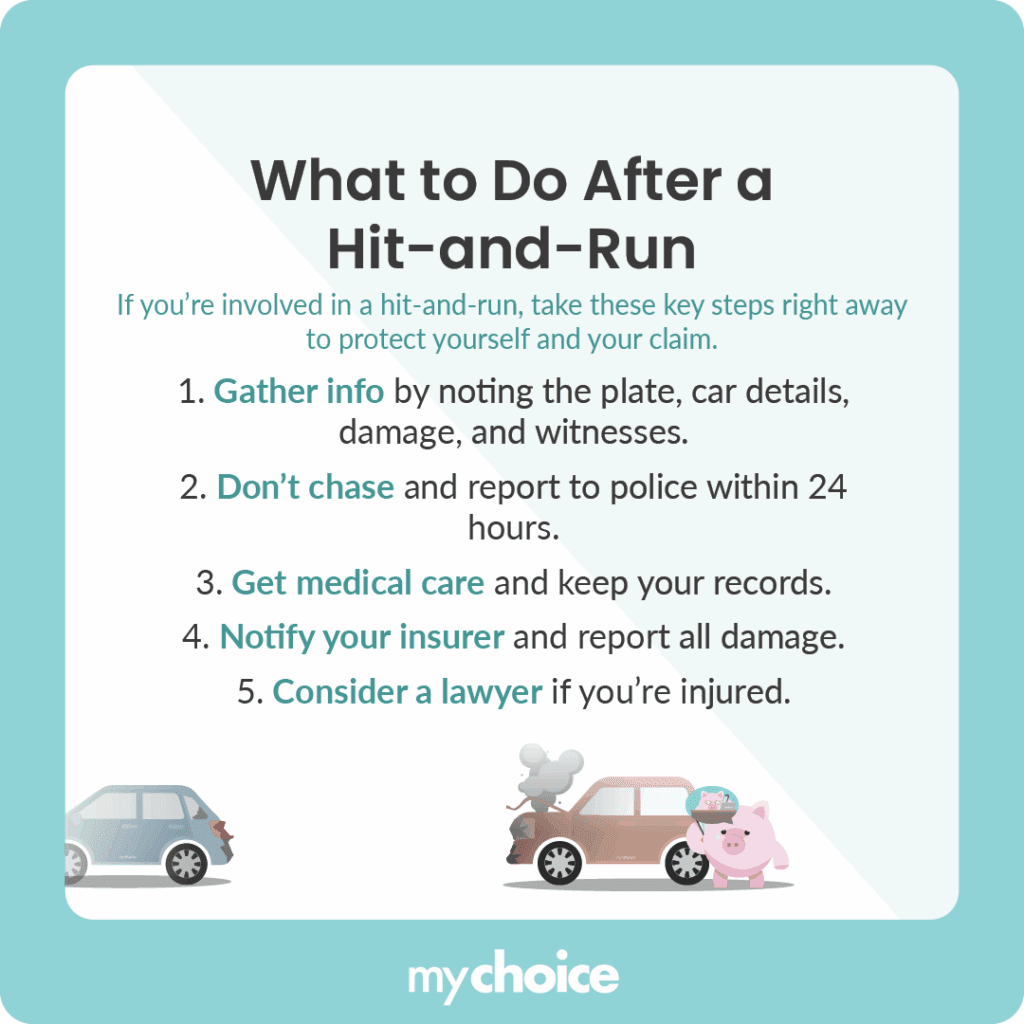

What Should You Do After a Hit-and-Run?

After experiencing a hit-and-run as a victim, follow these steps immediately after the incident.

How To Report a Hit-and-Run Accident in Ontario

Even if you don’t sustain any injuries or damage to your vehicle, reporting a hit-and-run accident to the police is essential. Ontario law requires all drivers involved in a hit-and-run to report it, regardless of the physical consequences (or lack thereof).

In addition, you must file a police report within 24 hours of the accident to maximize the odds of apprehending the perpetrator. Some insurers will only accept a claim if you file a police report.

Who Investigates a Hit-and-Run?

The Ontario police are primarily responsible for investigating a hit-and-run, though your insurance company will perform another investigation to determine culpability and the total cost of damages.

Until When Can You File a Hit-and-Run Claim?

The 24-hour figure applies to the police report. On the insurance side, the standard Ontario Automobile Policy requires you to notify your insurer within seven days of the incident, or as soon as you reasonably can. And if the fleeing driver is later identified and you want to sue them, the Limitations Act, 2002 generally gives you two years from the date of the accident.

What if the Hit-and-Run Happened in a Parking Lot?

If a hit-and-run occurs in a parking lot, perpetrating drivers will still be held liable for the incident. Check for security cameras if you fall victim to a hit-and-run in a parking lot. If you’re lucky, you might find video evidence of the accident, which you can then submit to the police and your insurance company.

Can’t find any security cameras in the area? Look for witnesses or security guards who can provide information.

What if the Fleeing Driver Was Drunk?

If the fleeing driver was impaired, they now face two separate Criminal Code offences:

- failure to stop (s. 320.16);

- impaired operation (s. 320.14).

Penalties can escalate depending on the level of damage. For instance, impaired driving that causes bodily harm carries up to 14 years in prison, and impaired driving can result in life imprisonment (Canada’s Criminal Code).

The severity of each punishment may vary according to the driver’s record and history. Additional instances of drunk driving can increase jail time, licence suspensions, and fees. Courts may order medical exams and physical inspections to determine the suspect’s behaviour and state during the incident.

Penalties for a Hit-and-Run in Ontario

Leaving the scene of a collision is a serious offence in Ontario, and it can expose a driver to two separate sets of consequences, one provincial and one criminal.

What to Do if You Cause a Hit-and-Run

If you cause a hit-and-run, the consequences will depend on the severity of your case. At the very least, your insurance company may raise your rates significantly and label you a high-risk driver. If your company considers you a significant liability, they might even cancel your policy.

Expect criminal charges if your actions caused serious injury or death. The best way to build a defence against a hit-and-run charge is to work with an experienced criminal defence lawyer.

Keep in mind that the legal-defence protection in an auto policy applies to civil lawsuits, not criminal charges, which means that paying for a criminal defence lawyer comes out of your own pocket.

Read More: A Guide to Demerit Points in Ontario