After the federal government’s 2026 trade reset with China, Canada announced it will let in up to 49,000 Chinese-made electric vehicles each year at a 6.1% tariff. This replaces the 100% surtax that was put in place in 2024.

This policy change means brands like BYD, MG, and other Chinese EV makers can now enter the Canadian market in larger numbers.

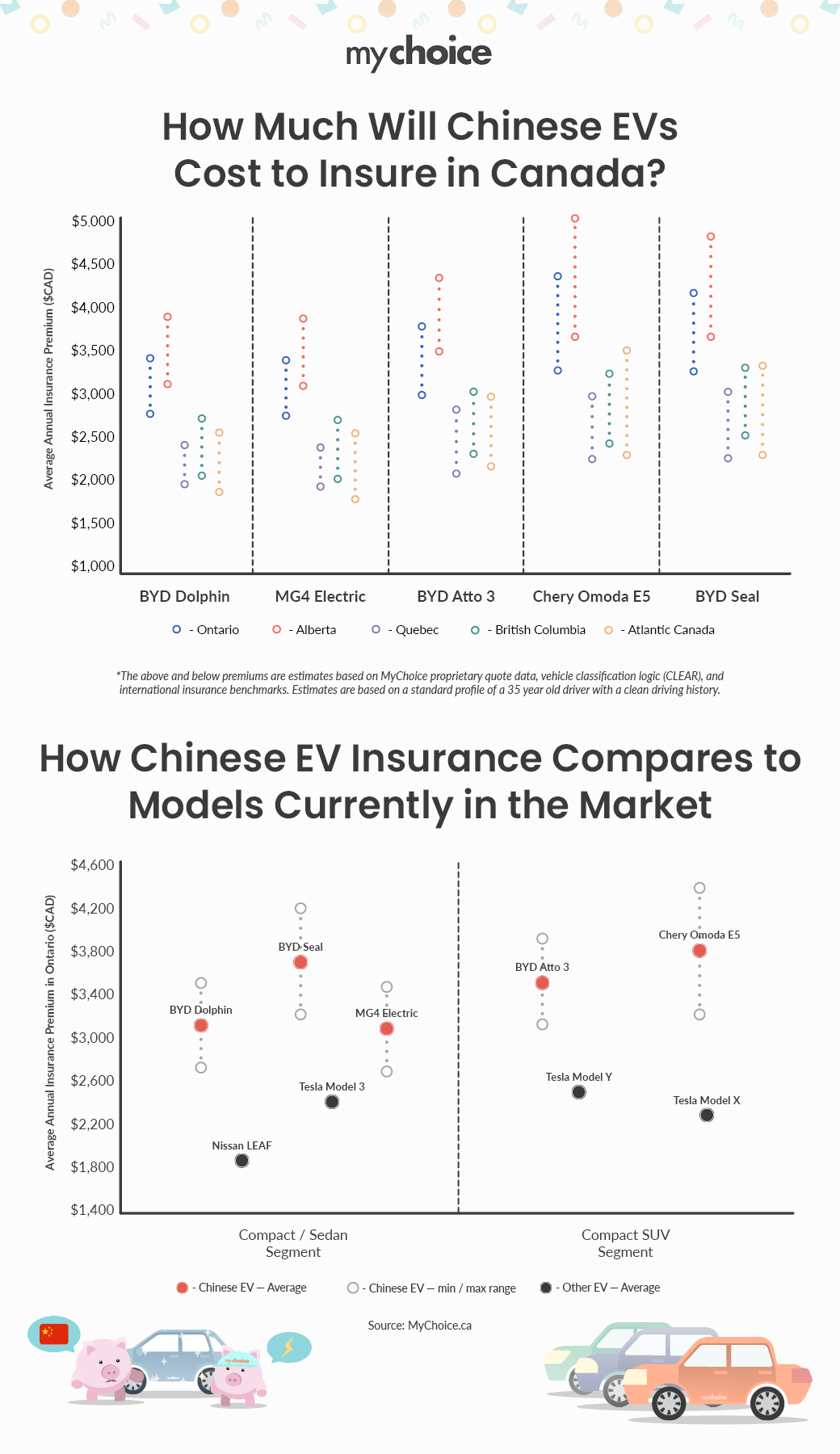

Lower prices might make the news, but Canadian drivers still have one big question: How much will it really cost to insure a Chinese EV here?

To answer that question, our team at MyChoice analyzed provincial EV insurance averages, CLEAR vehicle classification logic, repair severity data tied to EV calibration and battery complexity, and international insurance benchmarks from markets where BYD and MG already operate at scale. We then made a prediction on how insurers will likely price these vehicles over the next few years, based on how new models are typically introduced and classified in Canada’s auto insurance rating system.

How Much Will It Cost to Insure a Chinese EV in Canada?

Please note that the vehicles below are not yet widely available in Canada, so the car insurance premiums below are merely estimates of what they might cost to insure in Canada.

| Model | Segment | Ontario | Alberta | Quebec | British Columbia | Atlantic Canada |

|---|---|---|---|---|---|---|

| BYD Dolphin | Compact Hatch | $2,740- $3,480 | $3,126– $3,970 | $1,950– $2,450 | $2,050– $2,700 | $1,813– $2,573 |

| MG4 Electric | Compact Hatch | $2,700– $3,450 | $3,100– $3,950 | $1,900– $2,400 | $2,000– $2,650 | $1,780– $2,550 |

| BYD Atto 3 | Compact SUV | $3,065– $3,850 | $3,495– $4,391 | $2,100– $2,750 | $2,300– $3,000 | $2,191– $2,951 |

| Chery Omoda E5 | Compact SUV (New) | $3,226– $4,399 | $3,679– $5,019 | $2,250– $2,950 | $2,450– $3,200 | $2,311– $3,512 |

| BYD Seal | Mid Sedan | $3,226– $4,216 | $3,679– $4,810 | $2,300– $3,000 | $2,500– $3,300 | $2,311– $3,326 |

How We Estimated the Insurance Costs

Our methodology included our proprietary quote data, vehicle classification logic (CLEAR), and international insurance benchmarks.

Here’s how we did our research:

Why Budget EVs Won’t Be Automatically Cheap to Insure

“Insurance pricing isn’t based on the car’s retail price, it’s based on expected claim cost,” says Matthew Roberts, COO of MyChoice. “Even if Chinese EVs are cheaper to buy, insurers still have to factor in cost of replacing parts , repalceparts vailability and limited Canadian loss data. That’s why early premiums may be higher than many drivers expect.”

Even if a car costs $28,000 instead of $50,000, its insurance can still be more expensive. Insurance pricing depends on:

- Repair severity

- Parts logistics

- Calibration frequency

- Theft exposure

In some cases, lower-priced EVs may even reach “economic total loss” thresholds more quickly if repair costs account for a high percentage of the vehicle’s value.

Why Premiums Should Normalize by 2030

There are four conditions that could reduce premiums over time:

- CLEAR credibility improves as there is more claim data in Canada.

- There are more parts available on the market to service the vehicles.

- There are more independent repair networks available.

If these milestones are reached, we expect insurance premiums to move closer to regional EV averages by 2028 to 2030.

Key Advice from MyChoice

- Get an insurance quote before you buy a new-to-Canada EV. Early models can have unpredictable prices while insurers gather claims data.

- Look at the total cost of ownership, not just the sticker price. EVs usually cost a bit more to insure than gas cars.

- Shop around often. As CLEAR data gets better, different insurers may change their rates at different times.