How Do You Pay for a Car in Canada?

You can pay for a car in Canada in one of three ways:

- Leasing: Leasing is like long-term rent. You borrow a car, make monthly payments, and return the vehicle once your lease is over. Sometimes, you can buy a leased car at the end of your loan period, but that isn’t always the case.

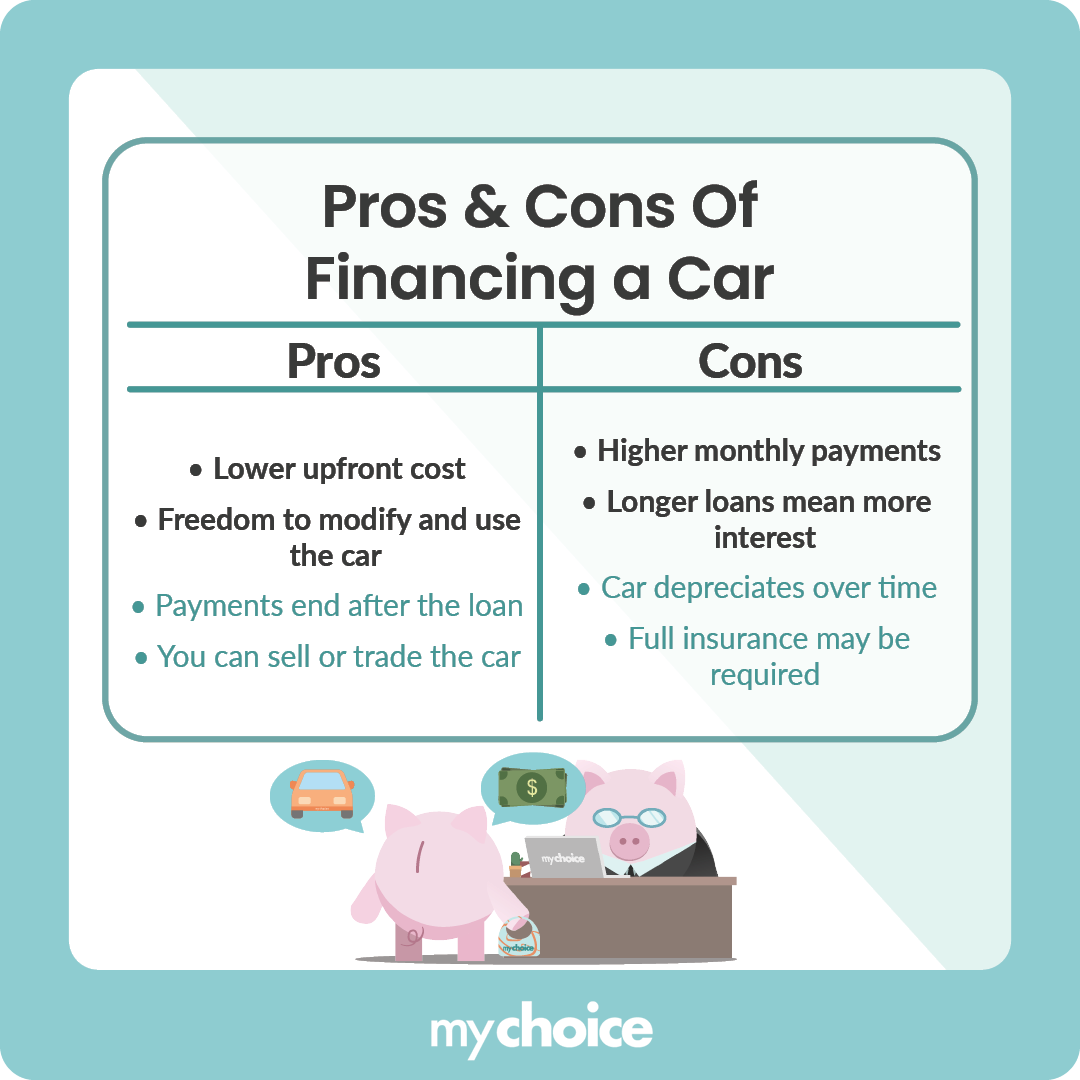

- Financing: Financing a car is like a mortgage. You sign a loan contract with a bank or other financial institution to get the money to buy your car. Then, you make regular payments to repay the loan’s principal and interest. Unlike leasing, financing a car means you can fully own the car once the loan is completely paid.

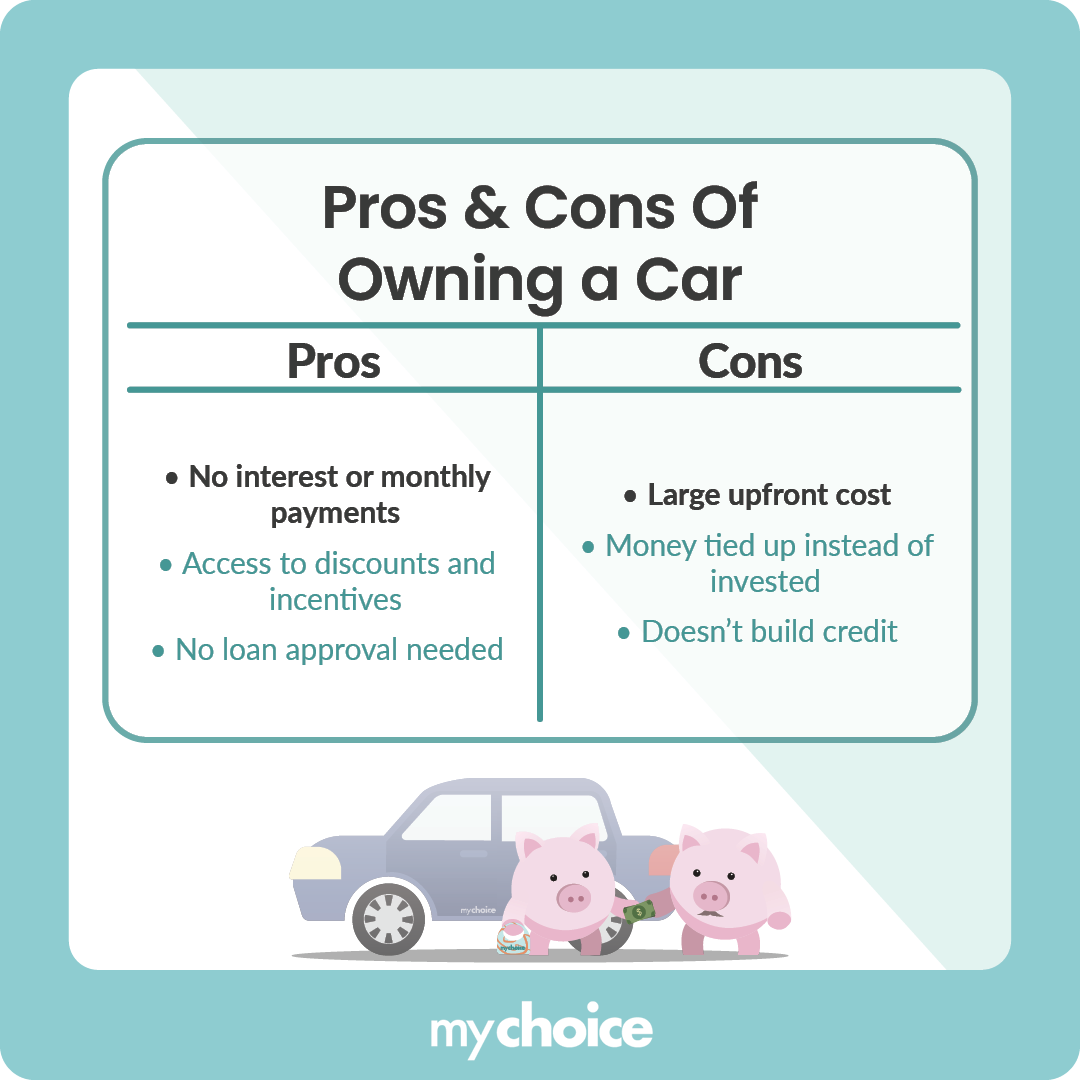

- Buying outright: This method is usually the simplest – you buy the car in full, and you own it the second the dealership agrees to the purchase. Not everyone has enough cash to buy a car outright sitting around, but, sometimes, it’s a good idea. Many dealerships have cash incentives, and you won’t be bogged down by loan interest.

Leasing and financing both involve monthly payments, but only financing is a loan. Leasing is a contractual agreement to use the vehicle for a set period. Read our comparison between leasing and financing a car to learn more.

What’s the Difference Between an Owned and Financed Car?

The main differences between an owned and financed car are your payment obligations and ownership status.

With an owned car, you don’t have to pay anything else besides the initial purchase price, and you fully own the vehicle. With a financed car, you still need to make regular loan payments, and you are the registered owner of the car, but the lender has a lien on it until the loan is fully paid off.

There are also other differences between owned and financed cars, like their insurance implications. Many lenders want you to get full coverage on a financed car because they want to protect their investments. Meanwhile, you’re only legally required to carry mandatory coverage, but many drivers still choose additional protection like collision or comprehensive coverage.

Owned vs Financed Car: How Should You Pay for Your Vehicle?

You should pay for your vehicle with the method that best suits your needs.

Financing your car is the more viable way to pay if you don’t have enough cash to make an outright purchase. However, the loan payments may end up costing more because the lender includes expenses and interest.

Meanwhile, buying a car outright is the most direct way to pay for your vehicle. You don’t need to deal with interest, and some dealerships even offer special prices for cash buyers.

That said, not everybody has enough idle money to buy a car with cash. Plus, you may miss out on money-making investments and projects if you use most of your cash to buy a car.

There are more benefits and drawbacks to either vehicle payment method. Let’s break them down here:

Car Insurance: Financed vs Owned

How you buy your car has insurance implications. Financed and owned cars have different insurance requirements because the number of people with an insurable interest in them differs.

On an outright-owned car, you’re usually the only person who has an insurable interest in it. This means you can dictate what kind of insurance coverage your car should have. As long as you have the mandatory Canadian auto insurance coverage, you can add extra coverage or skip them altogether, depending on your budget and needs.

With financed cars, your lender also has an insurable interest in the vehicle. Most auto loan lenders require full coverage insurance, which includes comprehensive and collision protection. This ensures that even if you get in an accident, the lender won’t experience a total loss on its investment.

Getting Insurance Coverage for Financed Cars

You need full insurance coverage on a financed car if your lender requires it. Different lenders have different insurance coverage requirements.

Check with your auto finance provider for more details. You can also have the lender get car insurance on your behalf, but that might be more expensive than shopping for a policy yourself.

Do Financed Cars Come With Insurance?

Financed cars don’t come with insurance by default. Some lenders or dealerships may offer insurance products, but auto insurance is not included in financing; you must obtain your own policy. That means you need to pay extra to get an insurance policy from the lender.

In most cases, you need to get a policy that meets the lender’s requirements by yourself. Lenders usually require mandatory, comprehensive, and collision coverage. Lenders require the latter two because they need to protect their investment in case of an accident.

In addition to lender-required coverage like collision and comprehensive, some optional endorsements (OPCFs) can provide extra protection. For example, OPCF 43 (waiver of depreciation) can cover the full replacement value of your vehicle if it’s written off, which can be especially useful for newer financed cars that depreciate quickly.

How to Deal With Accidents When Driving a Financed Car

The steps of dealing with accidents when driving a financed car are generally the same as when driving an owned car. However, you may need to inform your lender, depending on the terms of your loan agreement, especially for major repairs or total losses.

Here’s a quick step-by-step guide to dealing with accidents when driving a financed car:

- Check yourself, your passengers, and the other drivers.

- Call the local authorities and help them file an accident report.

- Contact your insurer to learn what’s needed to make an insurance claim.

- Check with your lender and follow their instructions, if any.

- Repair your vehicle according to the lender’s requirements.

- Pay your insurance deductibles, if any.

Read our article on what to do after a car accident to ensure you’re prepared.

Does Having a Financed Car Affect My Premiums?

Financing a car doesn’t directly increase your insurance premiums, but lender-required coverage (like collision and comprehensive) may increase your overall cost. You might also need a higher coverage limit because the lender requires it, raising your auto insurance rates.

What Happens to My Policy if I Don’t Make Payments on My Car?

If you stop making payments, the lender may repossess the vehicle, but your insurance policy will not automatically be cancelled. You must cancel or update it yourself. This happens because the lender will repossess your car, leaving you without an insurable interest in the car.

Can I Modify My Policy Once I Repay My Auto Loan?

You can modify your insurance policy once you repay your auto loan. The lender no longer has any say in your insurance coverage, so you can reduce or add insurance coverage according to your needs and budget.

Getting Insurance Coverage for Owned Cars

There’s a lot more leeway when you’re looking for insurance coverage for owned cars. You’re typically the only party with an insurable interest in the vehicle, so you can choose whichever policy add-ons fit your needs, as long as you have mandatory coverage.

Does Buying a Car Outright Affect My Premiums?

Owning a car outright doesn’t directly lower your insurance premium, but you may choose less coverage, which can reduce your overall cost.

Do I Need Full Coverage Insurance on an Owned Vehicle?

You don’t need full coverage insurance on an owned vehicle if you don’t want it. You’re the only one with an insurable interest in the car, so you can dictate what type of coverage you should and shouldn’t get.

Key Advice from MyChoice

- Choose your payment method based on your financial flexibility, not just monthly affordability — lower payments (like leasing) don’t always mean lower long-term costs.

- If you choose to finance your car, remember to include the cost of full insurance coverage in your budget, not just the loan payments.

- After you finish paying off your loan, check your insurance policy. You might be able to lower your coverage and save money on premiums.