What are Advanced Driver Assistance Systems (ADAS)?

Advanced Driver Assistance Systems (ADAS) are technology features that help drivers behave more safely or make the task of driving easier. Many of these features are now standard equipment on new vehicles.

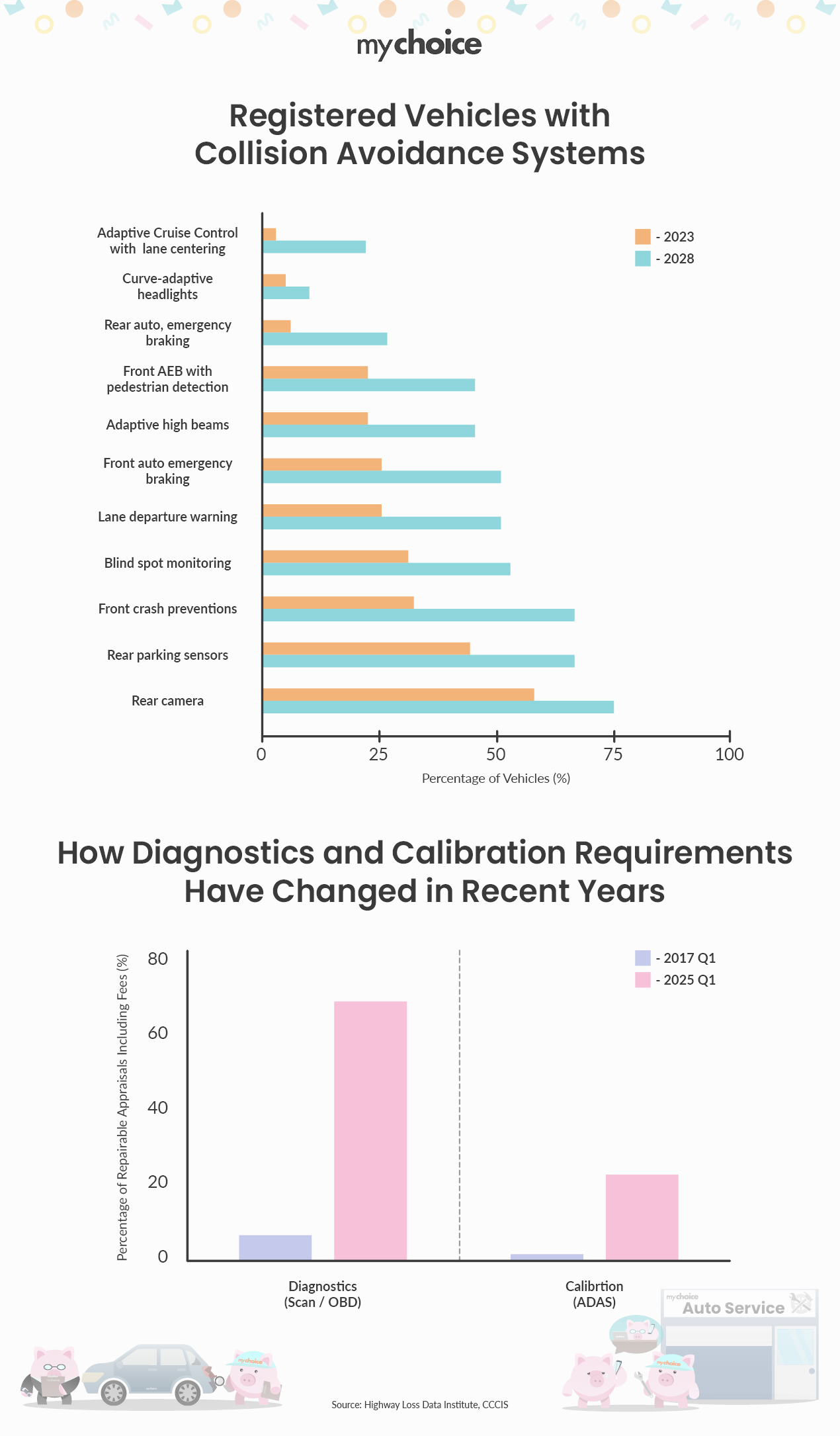

Backup cameras became mandatory on new vehicles beginning in 2018. Other ADAS features, such as forward collision warning, automatic high-beam headlights, and adaptive cruise control, are not legally required but have become increasingly common as standard equipment on new models. Blind spot monitoring, parking sensors, and highway drive assist systems are additional examples of ADAS that can have an impact on car insurance premiums.

Why is ADAS driving up collision repair costs?

Repairing ADAS after a collision involves more than simply replacing parts. Sensors, cameras, and other components also need to be calibrated to ensure these systems will function properly. Sensor calibration after an accident is a specialized skill in auto shops today, and it’s one that’s in increasingly high demand as these systems become more widespread.

According to data published by CCC Intelligent Solutions, just 0.9% of repairable insurance appraisals included calibration in 2017. That share increased to more than 23% by 2025, and direct repair programs report an even higher rate of 33% of appraisals now including calibration.

As demand for calibration has increased, auto shops have not kept up. Many still lack the specialized tools, software, and trained technicians required to execute these repairs. This means ADAS insurance claims that involve calibration often end up being seconded out to automaker dealerships or third-party vendors. As a result, the rates being charged for calibration have nearly doubled over the past five years and now average $500 per repairable vehicle.

On top of that, auto shops don’t always anticipate calibration costs when they prepare estimates for insurers. According to CCCIS data, less than 45% of initial repair estimates include ADAS calibration. This spikes the cost of insurance claims not only due to added and unexpected labour expenses but also because it delays repair completion, which adds to rental car costs as well.

What does this mean for insurance premiums?

The hidden repair costs of ADAS are causing insurance claim costs to spike. This is because:

- More cars are equipped with ADAS than ever.

- Many ADAS systems require calibration as part of their repair.

- Auto repair shops are not keeping up with the tools and training required for calibration.

- Cars that require calibration as part of repair are often moved to other shops, which creates delays and drives up labour and car rental costs

- Less than 45% of initial estimates include calibration, which means repair costs are becoming less predictable for insurers.

As these higher and often unexpected repair costs are passed on to insurers, this will inevitably be reflected in higher premiums. If you purchase a modern vehicle with ADAS, expect higher insurance premiums and longer repair times as a result.

Key Advice from MyChoice

- Ask repair shops whether ADAS calibration is required after an accident. Even minor damage to bumpers, windshields, or mirrors can affect sensors and cameras, requiring recalibration before the vehicle is safe to drive.

- Review your insurance coverage if you drive a newer vehicle. Vehicles equipped with ADAS might require sufficient collision and comprehensive coverage.

- Consider paying for a minor fix out of pocket. If the total repair cost is close to your deductible, paying out of pocket may make more sense than filing a claim.