Car insurance is mandatory in Canada. Whether you get your policy from a government insurer or a private company depends on where you live in the country.

The type of car insurance system available in your province or territory will affect your rates, coverage options, and ability to customize your policy.

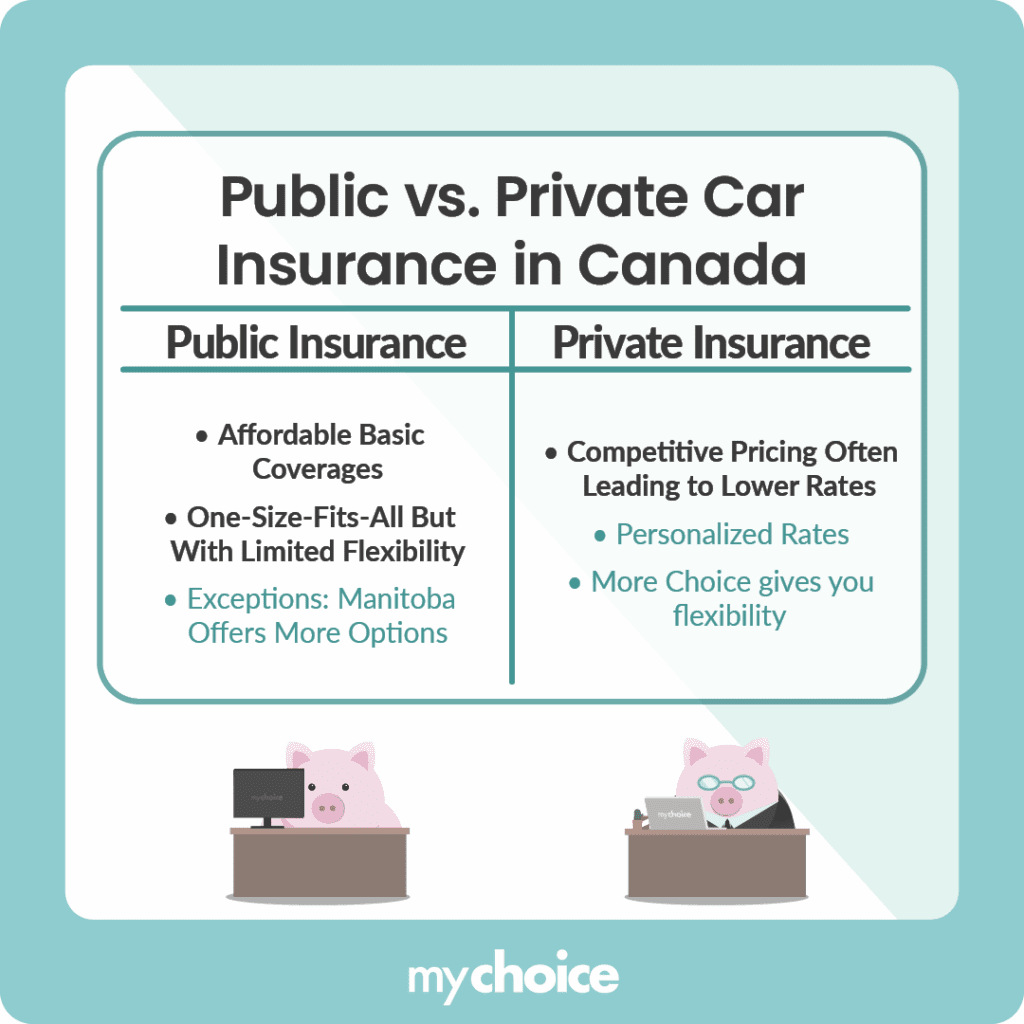

The infographic below shows the main differences between public and private auto insurance in Canada.

Overview of Auto Insurance Systems Across Canadian Provinces & Territories

| Province / Territory | Insurance System | Who Provides Mandatory Coverage | Who Provides Optional Coverage |

|---|---|---|---|

| British Columbia | Public | Public (ICBC) | Public (ICBC) |

| Manitoba | Public | Public (MPI) | Optional coverages & higher limits available from private insurers |

| Saskatchewan | Public | Public (SGI) | Optional coverages & higher limits available from private insurers |

| Québec | Hybrid (Public + Private) | Public insurer (SAAQ) provides injury/death coverage; private companies provide liability/property coverages | private insurers handle collision, comprehensive, liability beyond basic |

| Ontario | Private | Private | Private |

| Alberta | Private | Private | Private |

| New Brunswick | Private | Private | Private |

| Nova Scotia | Private | Private | Private |

| Prince Edward Island | Private | Private | Private |

| Newfoundland & Labrador | Private | Private | Private |

| Yukon | Private | Private | Private |

| Northwest Territories | Private | Private | Private |

| Nunavut | Private | Private | Private |

Why does Public Insurance exist in Canada?

Public car insurance ensures that every driver can get basic protection. The goal is to provide a steady, affordable level of coverage. This way, economic reasons and driving record problems won’t prevent people from driving. It also ensures that road crash victims receive compensation.

Which System is Better for Canadian Drivers?

The answer is that it depends on the angle you look at it from.

Public insurance guarantees access to coverage at affordable rates. Private insurance rewards low-risk drivers and encourages competition between the insurers. Each system optimizes for something different, and that difference shows up in pricing, behaviour, and outcomes.

Public car insurance works by spreading risk evenly across all the drivers. This keeps the insurance rates accessible even for high-risk drivers. This stability is effective, but it also means individual behaviour has less influence on the price.

In the private auto insurance system, risk is calculated and priced across different driver segments. This means that safe drivers with longer insurance histories pay lower premiums. In Ontario, for instance, a driver with a clean driving record pays, on average, 96% less in car insurance than a driver with one at-fault accident. While this is a more precise system, it can create pricing volatility. Premiums can rise rapidly in high-risk areas, creating affordability gaps. Insurers may also choose to cease operations entirely if they become unprofitable (i.e. Alberta).

Matthew Roberts, COO of MyChoice, puts it simply: “A public insurance system guarantees access to coverage. Private insurance rewards safe driving behaviour. The real debate isn’t about which system is better, but which outcome a province or territory is prioritizing.”

Key Advice from MyChoice

- Carefully review your coverage regardless of whether you live in a public or private insurance market.

- Understand your minimum coverage limits. If you move from a public province (i.e. Manitoba) to a private one (i.e. Ontario), remember that basic coverage in Ontario provides far less protection (liability only) than the same coverage in Manitoba (all perils).

- Shop around for cheaper rates if you live in a province with private insurance. Review your policy annually to ensure you aren’t overpaying.