If you’ve ever wondered why your cousin in Winnipeg buys car insurance from a Crown corporation while you shop quotes from a dozen private companies in Ontario, you’re in the right place. Our article explains how public and private auto insurance systems compare across Canada.

We based our comparison on data from ICBC, Manitoba Public Insurance, SGI, and Québec’s SAAQ and Statistics Canada’s April 2025 analysis of auto insurance premiums and profitability for the province-by-province cost numbers, and our own Ontario quote database for what a clean driving record is worth in a private market.

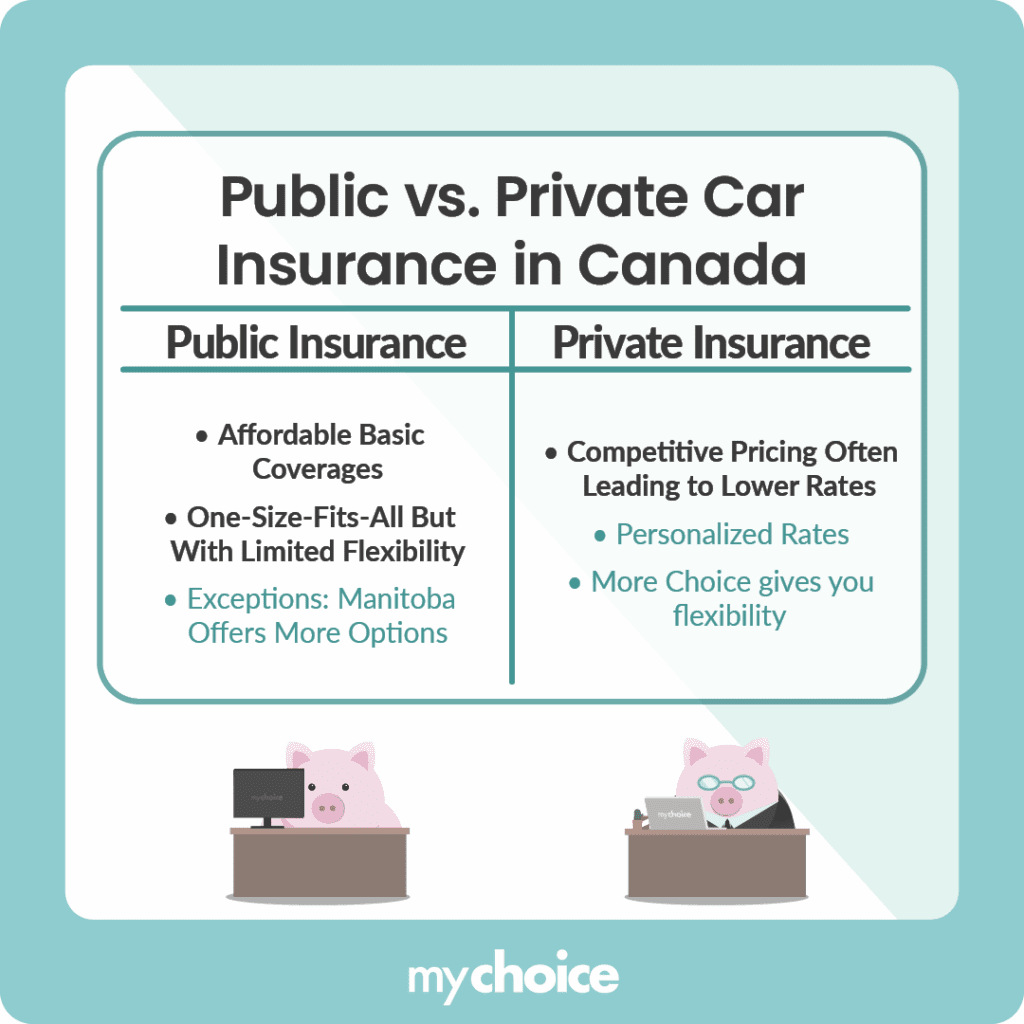

Which System is Better for Canadian Drivers?

If we’re looking at average premiums alone, then public provinces definitely win since insuring your car there is a lot cheaper.

Public car insurance works by spreading risk evenly across all the drivers. This keeps the insurance rates accessible even for high-risk drivers. This kind of approach keeps premiums more stable, but it also means individual behaviour has less influence on the price.

In the private auto insurance system, risk is calculated and priced across different driver segments. This means that safe drivers with longer insurance histories pay lower premiums.

In Ontario, for example, drivers with a clean record pay an average of $2,132 a year, while drivers with one at-fault accident average $4,178, 96% more, according to MyChoice data. The gap in premiums is a unique feature of the private insurance system where your driving record follows you. While this allows insurers to price policies more precisely based on individual risk, it can also create significant pricing volatility.

Insurers can also pull back their coverage when they begin incurring unsustainable losses. After Alberta paused rate increases in 2023, some companies limited issuance of new policies or left the province’s auto market altogether.

Matthew Roberts, COO of MyChoice, puts it simply: “A public insurance system guarantees access to coverage. Private insurance rewards safe driving behaviour. The real debate isn’t about which system is better, but which outcome a province or territory is prioritizing.”

What Do Drivers Actually Pay in Each System?

Here is the comparison of average auto insurance premiums across Canada’s public and private insurance systems. Since MyChoice only operates in private insurance markets, and to ensure an apples-to-apples comparison, we used Statistics Canada data for the below compariosn chart:

| Province | System | Average written premium (Dec 2024) |

|---|---|---|

| Ontario | Private | $2,068 |

| Alberta | Private | $1,818 |

| British Columbia | Public (ICBC) | $1,522 |

| Saskatchewan | Public (SGI) | $1,361 |

| Atlantic provinces | Private | $1,259 |

| Manitoba | Public (MPI) | $1,235 |

| Québec | Hybrid (SAAQ + private) | $1,044 |

Québec’s figure covers only the private half of its hybrid system. Injury coverage is funded separately through the licence and registration fees drivers pay the SAAQ.

Statistics Canada’s analysis ties the faster premium growth in the private provinces to rising repair, theft, and injury claims costs, which is the type of pressure the rate-regulated public insurers have absorbed differently, with ICBC holding basic rates flat into 2027 (ICBC).

Overview of Auto Insurance Systems Across Canada

The table below shows who provides mandatory and optional coverage in each province and territory.

| Province / Territory | Insurance System | Who Provides Mandatory Coverage | Who Provides Optional Coverage |

|---|---|---|---|

| British Columbia | Public | Public (ICBC) | Public (ICBC) |

| Manitoba | Public | Public (MPI) | Optional coverages & higher limits available from private insurers |

| Saskatchewan | Public | Public (SGI) | Optional coverages & higher limits available from private insurers |

| Québec | Hybrid (Public + Private) | Public insurer (SAAQ) provides injury/death coverage; private companies provide liability/property coverages | private insurers handle collision, comprehensive, liability beyond basic |

| Ontario | Private | Private | Private |

| Alberta | Private | Private | Private |

| New Brunswick | Private | Private | Private |

| Nova Scotia | Private | Private | Private |

| Prince Edward Island | Private | Private | Private |

| Newfoundland & Labrador | Private | Private | Private |

| Yukon | Private | Private | Private |

| Northwest Territories | Private | Private | Private |

| Nunavut | Private | Private | Private |

How Claims Work in Each System

Price is only half the comparison. The other half shows up after an accident happens, and public and private insurance systems handle that aspect very differently:

- British Columbia: ICBC has used its Enhanced Care no-fault model since May 2021. That means ICBC pays for injury treatment and wage-loss benefits no matter who caused the crash. In most cases, you also can’t sue the other driver, except in limited situations such as criminal driving.

- Manitoba: MPI’s Personal Injury Protection Plan has paid injury benefits on a no-fault basis since 1994 (Manitoba Public Insurance).

- Saskatchewan: SGI lets drivers choose between No Fault and Tort injury coverage, the only province where that’s a choice (SGI).

- Québec: The SAAQ compensates injuries no matter who was at fault, and lawsuits for bodily injury are off the table entirely. Vehicle damage runs through your private insurer under the province’s direct compensation agreement (SAAQ).

- Ontario: You claim accident benefits and not-at-fault vehicle damage from your own insurer, and keep a limited right to sue an at-fault driver for serious injuries.