What Is a Car Insurance Deductible?

A car insurance deductible is the amount you must pay out of pocket toward a covered claim before your insurer pays the remaining costs.

For example, let’s say that you’re making a claim for a $1000 repair on your car with a $100 deductible. The total amount you can actually claim from your insurer will be $900, and you can only claim it after you pay the first $100. The other $100 will have been “deducted” from the claimable amount (i.e. shouldered by you), hence the term “deductible”.

How Do Car Insurance Deductibles Work?

Car insurance deductibles work in two ways:

- After confirming the total cost of repairs for your car, your insurance company will issue you a cheque amounting to the total cost of repairs, minus your deductible.

- Many insurance companies have ties with repair shops, and going to one of them could make the claims process easier. In these cases, your insurer will pay the shop directly for the costs of repair up to your claimable amount. You will then have to settle the rest (your deductible amount) with the shop upon picking up your car.

In both cases, while your insurer will shoulder the brunt of the cost, the deductible amount will come from you.

When Do You Pay Deductible Car Insurance?

You typically pay a deductible when filing a claim that includes a deductible under your policy, such as collision or comprehensive coverage. Some claims do not require a deductible, such as certain not-at-fault accidents under DCPD in Ontario, which often has $0 deductible.

Having a deductible can be helpful for costly repairs, as it establishes a “ceiling limit” to how much you’ll have to shell out, while your insurer covers the rest. But how about for instances where the cost of repairs totals less than your deductible?

Insurers take your deductible into account before shouldering any costs. Thus, if your deductible is higher than the cost of repairs, it may be more economical to just pay out of pocket instead of filing a claim.

In this sense, when you file a claim, the deductible is the portion of the repair cost you are responsible for paying when you make a claim.

Types of Auto Insurance Deductibles

Some of the most common types of auto insurance deductibles are:

These are just some of the different types of auto insurance deductibles out there. Make sure to talk to your insurance broker and ask the right questions so you can get the best deal for you.

Should You Get Deductible Car Insurance?

Whether or not you should get deductible car insurance is ultimately up to you. One advantage of getting deductible car insurance is that it can actually lower your insurance premiums.

In a nutshell, you can think about insurance premiums and insurance deductibles having an inverse relationship. That is, when one goes up, the other goes down. Your insurer may offer lower premiums if you agree to pay a higher deductible, which could save you money in the long run. If you don’t see yourself filing claims that often, this might be a good arrangement for you.

On the other hand, having a higher deductible means that you’ll have to shell out more each time you make a claim. Remember also that your deductible is considered first when making a claim, so setting your deductible too high could work against you in practice.

Here’s an example: let’s say you get involved in an accident and the total cost for repairs totals less than your deductible. If the repair cost is less than your deductible, the insurer will not pay anything, and you would typically cover the repair cost yourself.

Having car insurance with a deductible could benefit you by lowering your monthly premium, but setting it too high could defeat the purpose of having it in the first place.

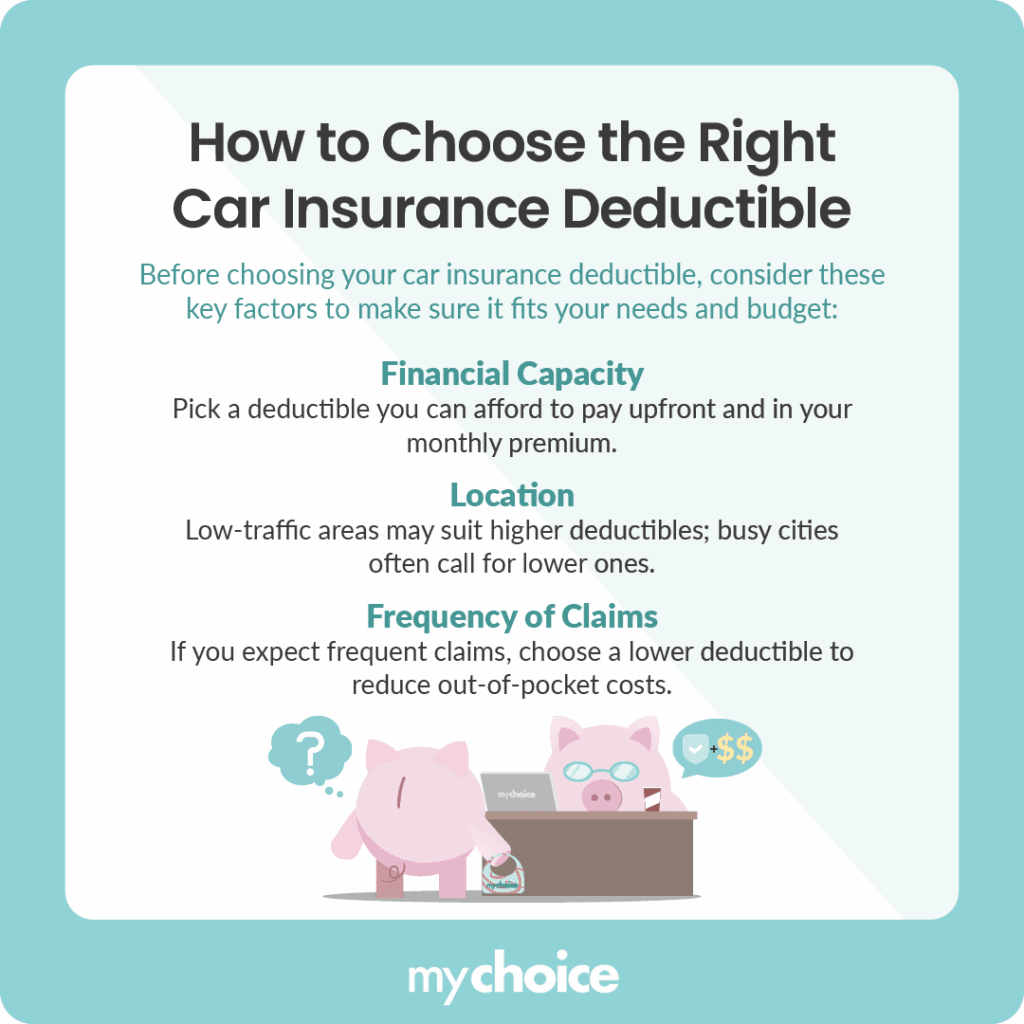

Factors to Consider When Setting Your Car Insurance Deductible Amount

Here are some factors to consider when setting your car insurance deductible amount:

Key Advice from MyChoice

- Pick a deductible you could actually pay if you had an emergency.

- If you want to lower your insurance premiums and you don’t file claims often, think about choosing a higher deductible.

- Don’t set your deductible too high. Smaller claims might not be covered at all, so you’d have to pay the full repair cost yourself.