With extreme weather events on the rise in Canada, including a number of severe floods and storms in recent years, water-related damage has become one of the top home insurance claims. For some insurers, rising claims costs have led to higher deductibles for flooding and sewer backup coverage, which means homeowners may be increasingly paying 100% out of pocket for minor issues.

What Is “Deductible Creep”?

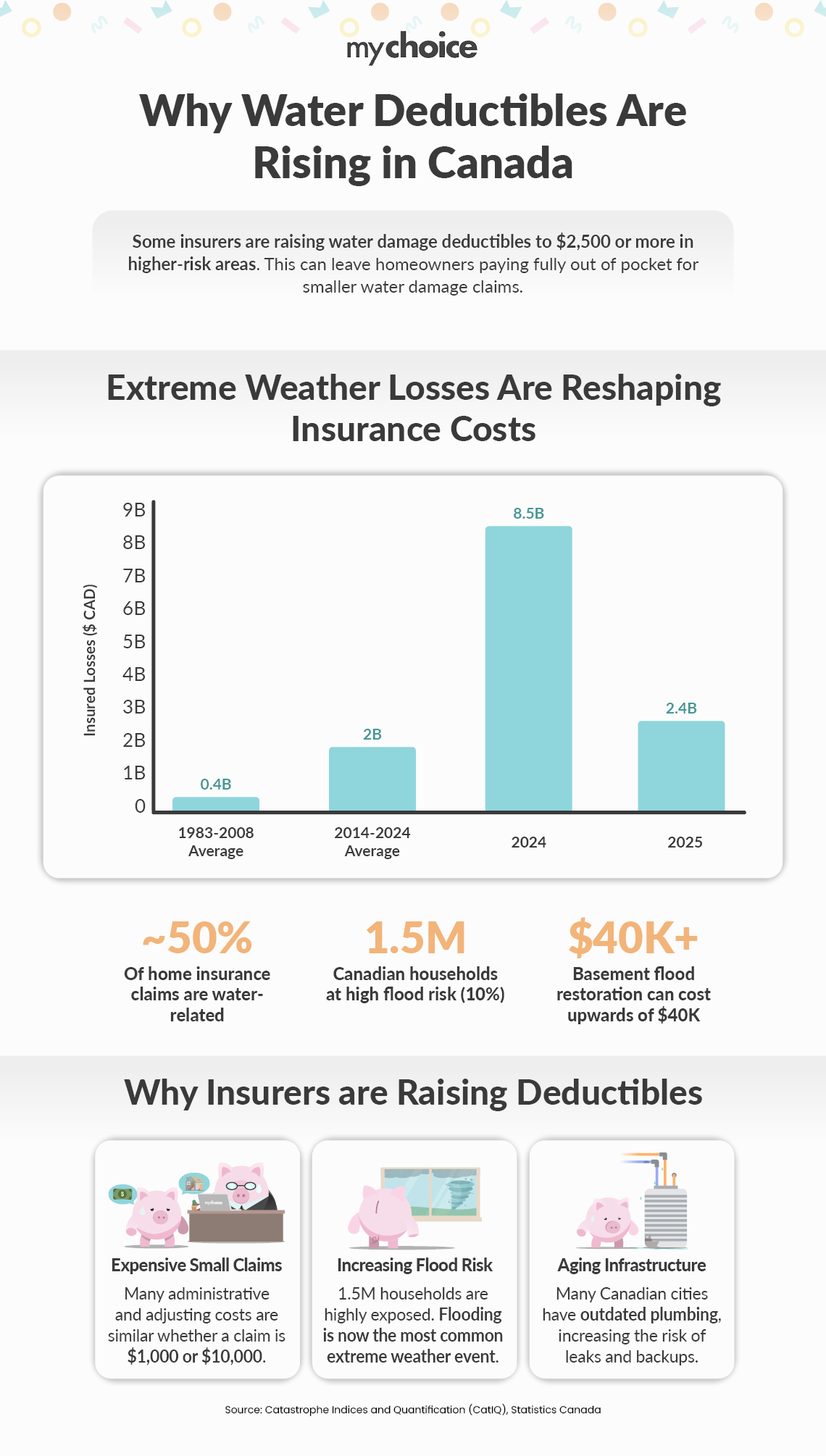

In 2025, insured damage caused by severe weather events in Canada exceeded $2.4 billion, according to Catastrophe Indices and Quantification (CatIQ). This follows record-breaking insured losses of $8.5 billion in 2024, including costly catastrophic events such as severe flooding in southern Ontario in July 2024 and flooding in Ontario and Quebec related to the remnants of Hurricane Debby in August 2024.

In some areas, the growing severity of extreme weather events may be reflected in higher premiums, but the increased risk of these claims for insurers is also causing ‘deductible creep.’

With the number of claims on the rise, some insurers have introduced higher deductibles for water-related endorsements, effectively shifting the cost of smaller, more frequent claims like burst pipes and minor flooding back onto homeowners. On a larger scale, higher deductibles may help insurers reduce exposure to frequent lower-severity claims.

For example, while your home insurance generally includes basic water coverage and carries an agreed-upon flat-fee or percentage-based deductible, an overland flooding endorsement or sewer backup coverage are specific, optional add-ons that carry a separate deductible.

The deductible for flood insurance is usually higher than the deductible for many other types of damage covered under home insurance policies, according to the Government of Canada.

At the same time, some insurers have been increasing mandatory minimum deductibles for these endorsements to as much as $2,500, or even more in high-risk areas.

Why Water Damage Is the Perfect Storm

It’s easy to understand why water damage claims are in focus for insurers.

Some 10% of Canadian households — 1.5 million — are estimated to be highly exposed to flooding. Flooding is now the most frequent extreme weather event in Canada, and extreme weather events in general, which used to be ‘unprecedented,’ are becoming more common.

As such, water damage is one of the most common claims for homeowners, accounting for a significant share of home insurance claims in Canada.

The average annual losses from water-related damage in the decade to 2024 were roughly $800 million, nearly double the yearly catastrophic claims average for 1983 to 2008, according to a StatsCan analysis cited above.

These claims have also been increasing over the last 10 years, resulting in higher reinsurance premiums for insurers and higher policy premiums for individuals, says StatsCan.

In some cases, this damage is significant and costly. Restoration after a basement flood can cost upwards of $40,000. But many water damage claims may not be catastrophic, yet can still cost thousands of dollars to repair, whether minor leaks requiring small repairs or flooding limited to a small space.

While some water issues are preventable through regular maintenance, severe weather-related claims may be hard to avoid, with flood risk increasing in many areas, water damage can be sudden, complex and involve a multi-step process to repair and restore. Water can seep into drywall quickly, cause damage to a home’s foundation and lead to other issues such as mould growth.

Many Canadian cities also have aging housing stock, including outdated plumbing, for example, which can increase the risk of leaks and sewer backups and lead to more water damage claims.

The Economics of Small Claims

For insurers, raising deductibles related to water damage means eliminating many smaller claims, which may be higher than the cost of the repair and require the same amount of resources to process as large claims, in terms of administrative costs and adjusting.

With smaller claims, insurers may need to dedicate more investigative scrutiny and administrative resources relative to their size to ensure they are valid, or face claims leakage — insurers paying out more on a claim than they should have.

For homeowners, small claims can also have a big impact. Making minor claims, especially several of them, can signal an ongoing problem with the property or increased geographical risk that may eventually lead to higher premiums.

Often, making a claim that is only slightly higher than the deductible is not worth it — but in an era where deductibles are rising, it is important for homeowners to be aware that they may have no option but to pay out-of-pocket for minor water damage.

Key Advice from MyChoice

- Take a close look at your water damage deductibles, not just your coverage limits.

- Keep in mind that flood and sewer backup coverage are often optional add-ons.

- Consider your options before filing a claim for minor water damage. If repairs only cost a bit more than your deductible, it might save you money in the long run to pay out of pocket.

- Put effort into regular maintenance and steps to prevent water damage. Updating your plumbing, keeping sump pumps in good shape, installing backwater valves, and fixing foundation problems can lower your risk of claims and serious damage.