How to Use Our Home Insurance Calculator

Below is a quick video showcasing how to use our home insurance calculator. Press “play” to learn how to save on your home insurance.

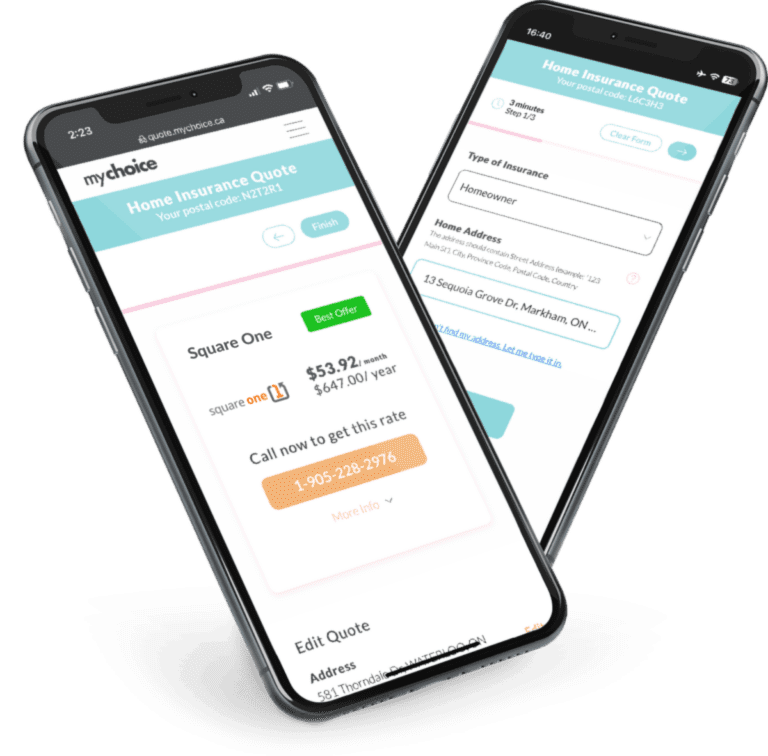

Estimate Your Home Insurance By Using Our Calculator

Navigating the complexities of home insurance can often seem daunting, with many homeowners unsure about the appropriate level of coverage for their needs. Using a home insurance calculator can simplify this process, helping to accurately calculate your premiums, identify the necessary coverage, and ensure you receive the best value from your home insurance policy.

For most Canadians, a home is not just a significant financial investment but also a cornerstone for family life and wealth accumulation. Given its immense value, the importance of safeguarding your property with the right homeowners insurance cannot be overstated.

Our versatile insurance calculator extends its utility beyond just home insurance, by offering savings across various property insurance types, such as renters or tenant Insurance and condo Insurance. Whether you’re looking to protect your family home or ensure your rental properties are covered, our calculator is designed to streamline the process and guide you to the most suitable insurance solutions.

How To Use Our Home Insurance Calculator

Using our home insurance calculator simplifies the journey to securing affordable home insurance.

By entering your details and providing as much information as possible, you’ll receive accurate quotes from Canada’s top home insurance providers. It’s a quick and easy process designed to save you money and hassle, with no obligation.

So How Much Home Insurance Do I Actually Need?

Most home insurance policies come with a default personal liability coverage of $100,000. However, MyChoice’s experts recommend a minimum total coverage amount of $1,000,000. Coverage amounts can go up to $5,000,000, depending on your needs. When calculating the coverage for the contents of your home, it’s recommended to take around 50% of the replacement cost for your home as a baseline.

Benefits of Using a Home Insurance Calculator

At MyChoice.ca, we believe that an informed choice is the best choice. Whether you’re buying a new home, moving, or renewing your policy, our home insurance calculator is designed to bring clarity, savings, and peace of mind to your insurance decisions. Start exploring your options today and take the first step towards securing your home and future with confidence.

How Does a Canadian Insurer Calculate Your Home Insurance?

The price of home insurance in Canada is influenced by a variety of factors, including your location, the type of property you own, and even your credit history. Below are some key elements that impact the cost of home insurance in Canada:

Home Insurance Terms You Should Be Familiar With When Using a Calculator

When it comes to home insurance, understanding the essential terms is crucial for navigating your policy and ensuring adequate coverage.

- Premium/Rate/Estimate/Quote: Your insurance premium is the payment you make to keep your insurance policy active, typically paid monthly or annually.

- Replacement Cost: This is the estimated amount required to rebuild your home from scratch in case of total loss. It varies based on your home’s unique characteristics and local construction costs.

- Actual Cash Value: This figure represents the replacement cost of your home minus depreciation, reflecting the current value of your home in its used condition.

- Endorsements: Optional additions or changes to your standard policy, allowing you to increase coverage or add new protections for specific items or situations.

- Deductible: The portion of a claim that you’re responsible for paying before your insurance coverage kicks in. Choosing a higher deductible can lower your premium.

- Depreciation: The decrease in value of your property or belongings over time due to use, wear and tear, or obsolescence.

- Perils: Specific risks or events covered by your home insurance policy, such as fire, theft, or natural disasters.

- Liability Coverage: Protects you in case someone is injured on your property or you cause damage to someone else’s property, covering legal costs and damages.

- Living Expenses: Coverage that helps pay for additional living costs if you’re temporarily unable to live in your home due to an insured disaster.

- Policy Limits: The maximum amount your insurance company will pay for a covered loss. It’s crucial to set limits that are adequate to cover potential losses.

These definitions provide a clearer understanding of common and essential home insurance terms, helping you navigate your policy with greater confidence.

Commonly Asked Questions About Home Insurance Calculators

How accurate will the estimate of my home insurance be when using a calculator?

They’re handy for getting an idea of how much you can roughly expect to pay for your home insurance, as they say, the devil is in the details – provide accurate information and the the quote will be as accurate as it can be. As you decide to purchase home insurance there could be some slight changes when finalizing policy details but for the most part, calculators are a great resource that all financially savvy Canadians should be taking advantage of.

What is the average price of home insurance in Canada in 2024?

As mentioned above, the cost of home insurance in Canada is influenced by a variety of factors and can significantly differ from one province to another, reflecting the unique risks associated with each region, such as local weather patterns, crime rates, and the cost of construction.

However, as per our recent quote data from early 2024, we have an average of $1,038 per year. You can see the provincial breakdown on this page.

Is it free to use a home insurance calculator?

It most definitely is, there is no obligation after using the calculator either.

If I calculate my home insurance multiple times will it affect my insurance?

No, your home insurance estimate will not be affected if you elect to do multiple insurance quotes.

If I live in a condo or rent can I still use a home insurance calculator?

Yes you can, our home insurance calculator offers the ability for dedicated condo and tenant insurance quotes as well.