Flooding has become a growing problem in Canada. According to the Government of Canada’s website, urban flooding from 2003 to 2012 resulted in over $20 billion worth of damage. In fact, water is the leading cause of home insurance claims in the country today, taking up 48% of all claims.

As such, homeowners and tenants should make sure they’re properly insured for all the different types of water damage. Here, we take a look at an oft-overlooked source of water damage: overland flooding.

Read on to learn more about overland water coverage, its cost, and whether it’s necessary for you.

What Is Overland Water?

Overland water is water that overflows from a body of freshwater, such as a lake or river, that enters homes, vehicles, or other types of property and causes damage.

Overland water is typically caused by heavy rainfall over short durations, extreme storms, and melting snow or ice. It can enter properties through windows and doors, rendering them unusable while flooded or under repair.

Understanding Water Damage Coverage

Overland flood coverage is not typically included in home insurance policies but can be purchased as an add-on for additional protection. Those who live near lakes and rivers or in low-lying areas are recommended to purchase this additional coverage, particularly as extreme weather is becoming increasingly common.

To better understand the differences between standard water damage coverage and add-ons, such as overland water coverage, review the basics of water damage coverage below.

Want to find out if home or auto insurance covers your car in storm damage? Read our home insurance guide to learn more. Looking to renovate your home or take out a new mortgage after significant overland water damage?

Overland Water Coverage vs Flood Coverage

In the insurance industry, overland water damage is distinct from flood water damage. The former describes water damage caused by freshwater, while the latter describes damage caused by coastal water or saltwater. This includes damages incurred from tidal waves and tsunamis.

Let’s break the differences down in this table:

| Overland Water Coverage | Flood Coverage | |

|---|---|---|

| Included in standard home insurance? | No, can be purchased as an add-on | No, can be purchased as an add-on |

| Type of damage it protects you from | Damage caused by freshwater | Damage caused by saltwater |

| Recommended for | People in areas with high flood risk | People living near the coast |

What Endorsement do I Need Based on Where I Live?

Overland water and flood coverage are usually available as endorsements to your existing home insurance coverage. While getting both is ideal to maximize your protection, sometimes budget concerns only allow you to choose one.

You should prioritize overland water coverage if you live in a flood-prone area. Some cities in Ontario that are at high risk of flooding include Ajax, Ottawa, Mississauga, Toronto, and Brampton. Fortunately, the Ontario Government is working on protecting its people with its flood resilience initiatives, which include better flood mapping, enhanced flood forecasting, and improved emergency response.

Meanwhile, flood insurance may be the better option if you live in a high-risk coastal community, generally in provinces with high sea-level rise levels like British Columbia, Nova Scotia, Newfoundland, and New Brunswick. Communities like Vancouver, Richmond, and Halifax County are examples of high-risk places for coastal flooding.

Who Is Eligible for Overland Water Coverage?

Unfortunately, not all property owners will be eligible to add overland water coverage to their home insurance policy.

Those who own or rent properties in high-risk flood zones may not be able to purchase this add-on, as the risk will be too high for the insurance provider. Typically, those who live within 100 meters of flowing bodies of water such as rivers or springs and those whose driveways slope downwards towards their house may be considered high-risk candidates.

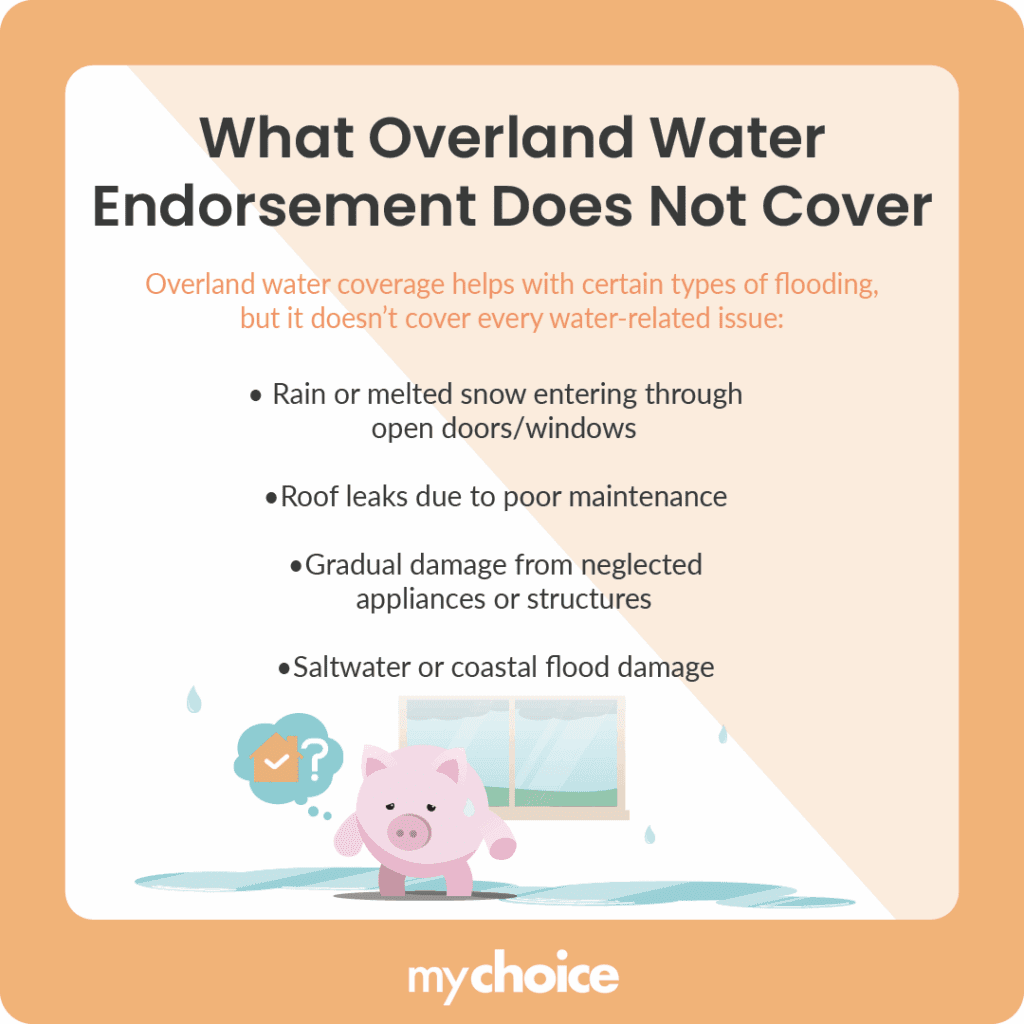

What Overland Water Coverage Doesn’t Cover

Take note that an overland water coverage add-on does not cover the following types of losses:

- Rainwater or melted snow that enters the property through an open door or window

- Water that leaks through a poorly-maintained roof

- Damages that accumulate over time from neglected appliances or structures

- Damages from saltwater or coastal floods

Should You Get Overland Water Coverage Even if You Live in a Condo or Apartment?

Even those living in mid- or high-rise dwellings such as condominiums or apartments can be affected by overland water flooding.

For example, an apartment building near a lake gets flooded by overflowing water after days of non-stop rain. The building’s lobby, elevator, and lower-level amenities are rendered unusable, so all tenants are advised to relocate while the damages are fixed. Cars parked in basement parking garages underneath condominiums may also become damaged by the floodwater.

Overland water coverage can cover any additional living expenses over the following weeks, such as hotel accommodations and food costs as well as damages to vehicles.

Should Renters Get Overland Water Coverage?

Renters can benefit from overland water coverage the same way landlords and homeowners can. Traditional home insurance policies do not typically cover overland water damage, so it’s good to purchase this add-on for your peace of mind.

This is especially important for those renting basement apartments, as well as those who rent houses with furnished basements or use their basement to store valuable items.

How Much Does Overland Water Coverage Cost?

The cost of overland water coverage will depend on whether your area is at high or low risk for flooding.

If you live near a body of water, at the bottom of a slope or hill, or in an area that sees a significant amount of rainfall and snow, you will likely face higher premiums. Typically, adding overland water coverage to your policy can set you back roughly $10 to $30.

Thankfully, there are ways to lower your premiums, including waterproofing your basement and purchasing sewer backup coverage.

If you want to find out how much home insurance typically costs in Ontario, read our blog to learn more. If you’d like to find out who the best home insurance providers are in your province, check out our list of the top home insurance companies here.

How to Prevent Water Damage in Your Home

Although water damage can happen suddenly and without warning, some types of water damage can be prevented or reduced significantly. Save yourself hundreds of dollars in water damage by following these tips:

Is Overland Water Coverage Mandatory?

Homeowners are not legally required to purchase home insurance in Canada. Thus, overland water coverage is not mandatory.

However, take note that most mortgage lenders will not offer a mortgage to borrowers without insurance.

Is Overland Water Coverage the Same as Flood Coverage?

Overland water coverage and flood coverage are not usually interchangeable in the insurance world. Check with your insurance provider to ensure your policy covers both types of flooding.

Overland water coverage refers to protection from damages incurred by overflow from a nearby body of freshwater, such as a river or lake. Flood coverage, on the other hand, refers to protection from damages caused by saltwater.

Can I Get Overland Water Coverage Without Sewer Backup Coverage?

You typically need to get both overland water and sewer backup coverage at the same time.

Most insurance providers allow policyholders to get sewer backup coverage alone. However, they won’t cover damages caused by sewer backups coming from overland water.

Does Overland Water Coverage Have Deductibles?

Some providers have deductibles for overland water coverage. This varies from provider to provider.

What Isn’t Covered by Overland Water Coverage?

Besides saltwater flooding, breaches of dams, levees, and other man-made structures are typically not covered by an overland water add-on.

How Can I Lower My Overland Water Premiums?

To lower your premiums, you can opt for a higher deductible, lower your personal property coverage, or opt out of personal property coverage for overland water. The latter means that your home will be covered for overland water damage, but any personal belongings inside won’t.

Key Advice from MyChoice

- Overland water coverage is an important add-on that all homeowners should consider, given the growing problem of flooding and extreme weather in Canada. This additional coverage can save you hundreds of dollars in damages should you find yourself in the unfortunate situation of overland flooding.

- Depending on your budget, you can get both overland water and flood coverage or just one.

- If you have to choose, assess your area and determine whether fresh or saltwater floods are more likely to happen.

- If you live near a body of water or in an area with lots of snow and rainfall, your water damage coverage costs may be higher.

- Use MyChoice to compare home, tenant or condo insurance rates or check out our insurance calculator to get the best rates in your area.