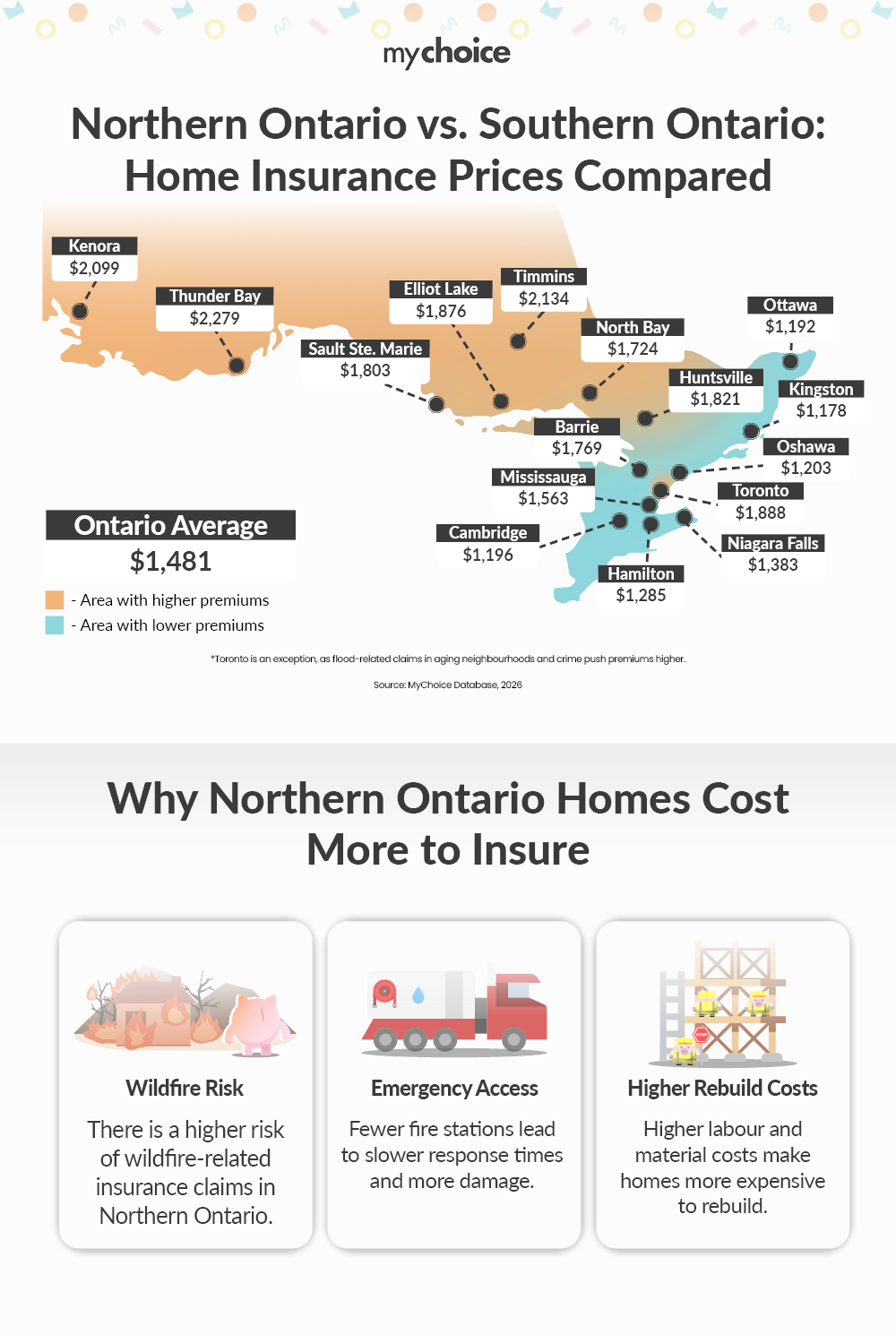

Year over year, home insurance premiums are on the rise across Ontario — but for homeowners in some Northern Ontario communities, the increase has been even more significant, as climate-related risks come face-to-face with concerns over the proximity to emergency services and high rebuild costs.

Climate Risk – One Piece of the Puzzle

In the northern part of the province, the increase in extreme weather events, whether severe storms, flooding or wildfires, is one reason for heightened claims risk.

Northwestern Ontario in particular has seen considerable wildfire activity over the last decade, with more than 2.2 million hectares burned since 2015, compared with some 287,000 hectares in the northeast, according to Ministry of Natural Resources data, via CBC.

In 2025, there were 643 wildfires in Ontario with 597,654 hectares burned, the vast majority of which were in Northwestern Ontario, including Ontario’s largest wildfire on record.

This is reflected in MyChoice’s wildfire risk score of cities like Kenora, which saw an increased risk of wildfires, scoring 6.2/10 in 2025, up from 5.4 in 2024.

Timmins and Sudbury remain on the lower end of the wildfire risk scale but still score a 4.8.

What Is “Service Proximity Risk” and Why Does it Matter?

For residential properties, having local fire support that can respond to emergencies quickly is not only necessary for safety, but can also help limit property damage and insurance risk.

Generally, living between eight and 13 kilometres or less from a fire station is ideal, in terms of being protected by fire services, as the Insurance Bureau of Canada told Sudbury.com, although each insurer is different when it comes to their level of acceptable risk.

In many Northern Ontario communities and surrounding areas with higher premiums, populations are often served by fewer fire stations, or they service large geographic areas. Many also rely on volunteers or paid-per-call firefighters alongside full-time employees.

In recent years, discussions to close and consolidate fire stations in the Greater Sudbury area, for example, led to concerns over higher insurance rates, as some homes would be located several kilometres further away from their nearest essential services. Some areas are also facing a volunteer firefighter shortage.

Fire Service Coverage in Selected Ontario Communities

| City | Population (approx.) | Fire Stations | Staffing Model |

|---|---|---|---|

| Timmins | ~42,000 | 1 career + 6 volunteer | Mixed (career + volunteer) |

| Kenora | ~16,000 | 3 | 1 full-time, 2 paid-on-call |

| Huntsville / Lake of Bays | ~20,000 | 5 | Primarily volunteer |

| Elliot Lake | ~11,000 | 1–2 (local coverage) | Mixed (full-time + volunteer) |

| Barrie | ~160,000 | 6 | Fully career-staffed |

| North Bay | ~53,000 | 4 | Majority full-time |

| Sault Ste. Marie | ~76,000 | 4 | Fully career-staffed |

| Thunder Bay | ~110,000 | 8 | Career + composite |

Smaller and more remote communities usually rely on volunteer firefighters, have fewer stations, and cover larger areas. On the other hand, bigger southern cities often have more stations close together and full-time crews, which helps them respond faster and keep losses lower.

This difference matters a lot for insurance. When response times are longer and there are fewer stations, claims can be more severe, especially during fires. As a result, insurance premiums may be higher.

Rebuild Costs: The Silent Driver of Premiums

When it comes to home insurance, it is the price of repairing or fully rebuilding a home after a loss that drives premiums, rather than a home’s market value.

And across the country, rebuild costs have soared over the last few years.

As data from StatsCan and ICBA shows, from 2019 until Q3 2025, residential construction costs jumped 69%, driven by factors like rising input costs, supply chain issues, labour shortages and more recently, tariffs.

More specifically, from 2021 to 2026, home replacement costs increased by 24% in Canada, according to Verisk Canada.

In areas like Northern Ontario, these expenses may be further intensified by a few factors, like:

What Does This Mean for Homeowners in Northern Ontario?

For Northern Ontario homeowners, factors like climate risk, proximity to emergency services and higher rebuild costs can lead to high home insurance premiums in general — and year-over-year increases that are larger in comparison to many other areas of the province.

Key Advice from MyChoice

- Review your coverage for climate risks. Most standard insurance policies do not cover important risks, such as overland water or sewer backup. If you live in a higher-risk area, adding this coverage is now more important than ever.

- Understand your rebuild value, not just market value. Insurance is based on how much it would cost to rebuild your home. Because labour and materials are more expensive now, check that your coverage matches today’s rebuild costs.

- Ask about fire protection grading and proximity. If your home is far from a fire station or has limited emergency services nearby, your insurance premiums may be higher. Knowing your risk level can help you compare options more easily.

- Invest in loss prevention measures. Adding things like sump pumps, backwater valves, fire-resistant materials, or monitored alarms can lower your risk and may also reduce your insurance premiums over time.