The Canadian home insurance landscape is currently undergoing a structural realignment driven by a decade of escalating weather-related claims and aging housing supply.

Amid all this, the age and condition of a roof have become one of the first things insurance companies look at when evaluating both premiums and claims. While most insurers previously allowed asphalt roofs to reach 20 or even 25 years before tightening scrutiny, practical underwriting pressure now begins closer to the 15-year mark.

Most Canadian homeowners with comprehensive home insurance policies that include a guaranteed replacement cost are unaware that the age of their roofs can cost them thousands of dollars in losses.

That’s why our team at MyChoice decided to quantify what we call the “Roof Gap,” analyze how insurers apply RCV to older structures, and outline the financial risks for Canadian homeowners who delay roof replacement.

The “Replacement Cost Pressure Point”

If you recently serviced your roof and a disaster strikes, you are generally guaranteed to receive full replacement value, provided you have a comprehensive insurance policy with RCV coverage and the damage to your roof was caused by a covered peril.

However, when a roof is brittle and not in top condition, adjusters may narrow the scope of damage or challenge whether the storm or deterioration caused it.

That’s when your payout may go from a “Replacement Cost Value” (RCV) to “Actual Cash Value” (ACV).

Under RCV, the insurer pays to replace the damaged roof with brand-new materials of similar quality, minus only the deductible. Under ACV, the insurer pays only the depreciated value of the roof at the time of loss.

For a typical $20,000 roof replacement in the GTA or Calgary with a $1,000 deductible, the difference between an RCV payout and an ACV payout for a 15-year-old roof (with a 20-year expected life) is devastating:

| Factor | RCV Policy (New Roof) | ACV Policy (Aging Roof) |

|---|---|---|

| Current Replacement Cost | $20,000 | $20,000 |

| Depreciation Deduction | $0 | $15,000 (75%) |

| Policy Deductible | $1,000 | $1,000 |

| Insurance Payout | $19,000 | $4,000 |

| Homeowner Out-of-Pocket | $1,000 | $16,000 |

Why Delaying Your Roof Repairs is Exponentially Expensive

The cost of replacing a roof in Canada has decoupled from the general Consumer Price Index (CPI). While general inflation was approximately 18% over the last five years, residential building construction costs surged by 67%.

The Tariff and Labour “Transmission Cycle”

- Tariff Impacts: In 2025, Canada implemented 25% countermeasure tariffs on steel and aluminum from the US. For a standard 2,000 sq. ft. home in Ontario, these tariffs alone added an estimated $3,750 to the cost of a metal roof.

- Labour Shortage: BuildForce Canada expects a shortage of over 85,000 skilled workers by 2034. This shortage has pushed labour rates in cities like Calgary to an average of $43 per hour, with complex jobs reaching double that amount.

- Modular Rebuild Rates: Total residential reconstruction costs in most Canadian markets now range from $200 to $350 per square foot.

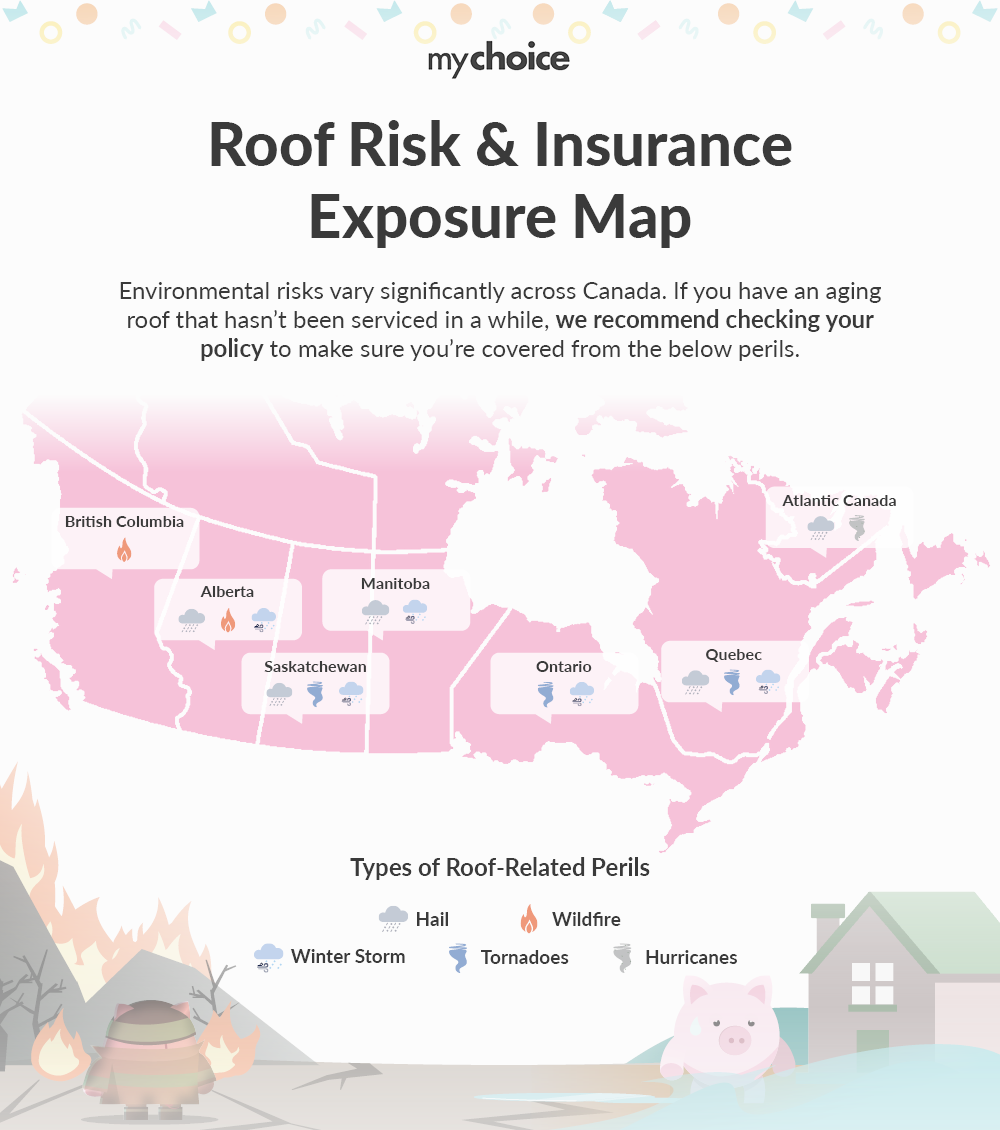

National Risk Mapping: Regional Vulnerabilities

Homeowners across Canada face distinct environmental threats that influence roof claim frequency and underwriting focus.

| Province | Primary Perils | Insurance Impact & Underwriting Trends |

|---|---|---|

| Alberta | Hail, Wildfires, Winter Storms | Highest national catastrophe loss costs; elevated scrutiny on roof age in hail-prone zones |

| Saskatchewan | Hail, Tornadoes, Winter Storms | High exposure to supercell roof damage |

| Ontario | Tornadoes, Winter Storms | Windsor–Ottawa wind corridor; high frequency of shingle uplift claims |

| Manitoba | Hail, Winter Storms | Significant summer storm losses; increased focus on roof condition in rural zones |

| Quebec | Hail, Winter Storms, Tornadoes | Record March 2025 ice storm losses (~$490M); ice damming remains a big problem |

| British Columbia | Wildfires | Highest rebuild costs nationally ($200–$350 per sq ft); wildfire interface risk limits underwriting flexibility |

| Atlantic Provinces | Hurricanes, Hail | Escalating wind claims; shift toward percentage-based hurricane deductibles. |

Key Advice from MyChoice

- Invest in impact-resistant shingles. In hail-prone regions (Alberta and the Prairies), Class 4 impact-rated shingles can reduce claim frequency and protect the integrity required for full RCV application.

- Perform annual maintenance review. Clear gutters and trim overhanging branches every spring and autumn. A well-documented maintenance history strengthens your position in a claim scenario.

- Review your insurance policy renewal documents. Review your policy for roof-related endorsements or settlement limitations. Even with RCV language, endorsements may modify how aging roofs are treated.