What Is a Reserve Fund, and Why Do Condo Owners Depend on It?

In every province, condo corporations have to maintain at least one reserve fund (sometimes called contingency reserve funds), to cover major repair or replacement of the building’s common elements, such as the roof, parking garage, elevators, pipes, HVAC system and amenities.

As the Condominium Authority of Ontario notes, the reserve fund can’t be used for upgrades and alterations.

Part of condo owners’ monthly fees, or their payment towards the common expenses, is contributed to the reserve fund.

To make sure the reserve fund is healthy, condos are required to carry out reserve fund studies, which estimate the cost of the repairs and replacements and their expected life span in order to make a 30-year plan, and update these at least every three or five years, depending on the province.

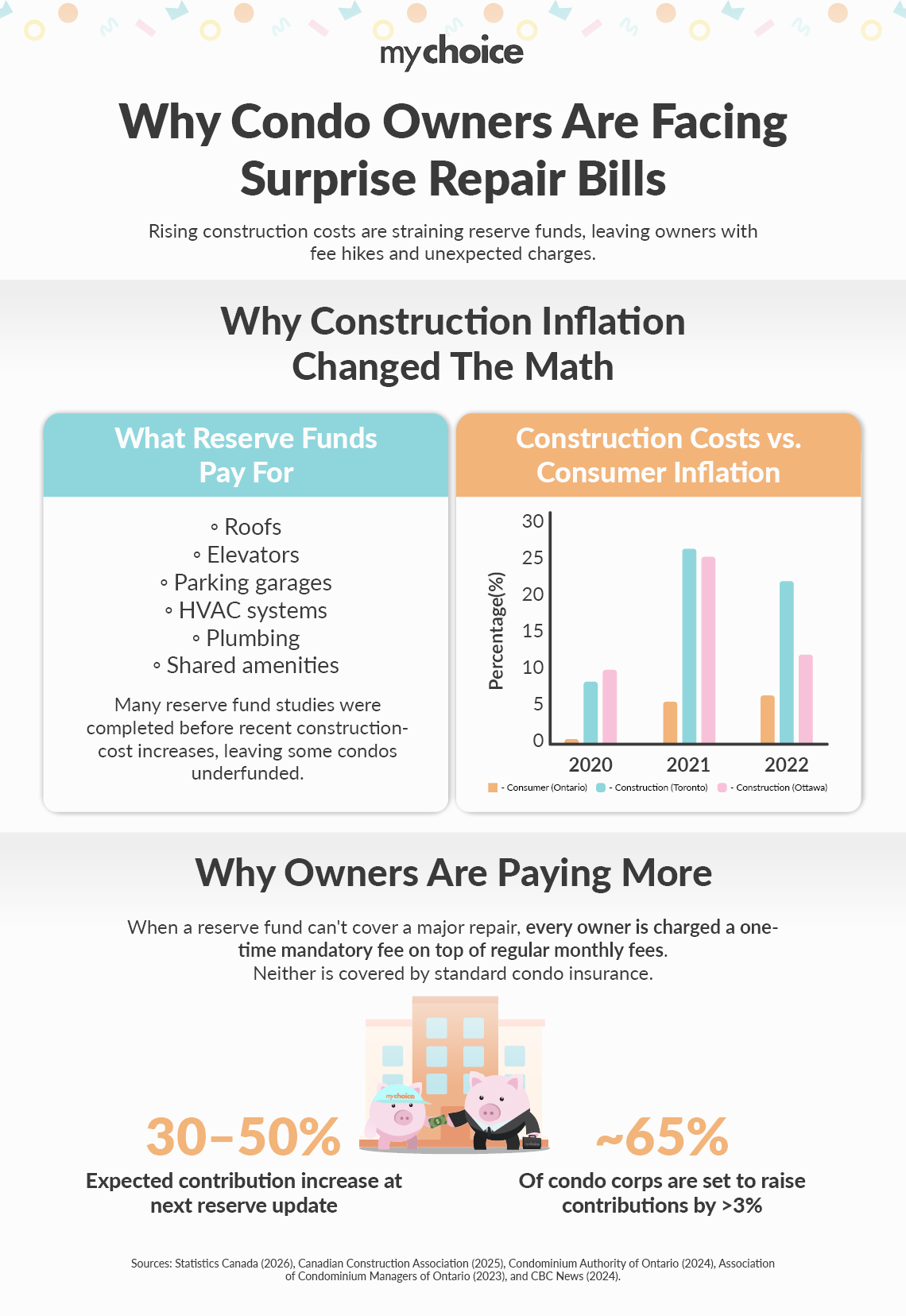

Why Construction Inflation Changed the Math

With construction costs rising in recent years, today’s repair costs may no longer align with forecasts set out a few years ago.

Since the pandemic, materials and labour costs have soared, and while they have come down from their peak, they are still growing faster than overall inflation.

From Q1 2020 to Q1 2026, StatsCan’s Residential Renovation Price Index, which measures the average price of eight residential project types, rose more than 56%.

Statistics Canada’s Building Construction Price Index (BCPI) rose 4.1% year-over-year in Q4 2025, led by metal fabrications, structural steel framing, concrete and plumbing.

Back in 2021, just over half of reserve fund studies used assumed forward-looking inflation rates between 1% and 2%, while 30% used rates between 2% and 3%, according to the Condominium Authority of Ontario (CAO)’s report on reserve fund survey findings, released in fall 2024.

This did start to change in 2022 and 2023 with:

- more than 35% of reserve fund studies using inflation rate assumptions of between 2% and 3%, and;

- the number of studies assuming rates between 3% and 6% also increasing compared with 2021

Nearly two-thirds of condo corporations also received recommendations to increase their reserve fund contributions by more than 3%.

Indeed, in a 2023 article, the Association of Condominium Managers of Ontario cautioned that reserve fund study updates will have to reflect the significant increase in costs, “even for those projects that are in the distant future,” via contribution increases and, in some cases, special assessments for those with substantial projects that can’t be deferred in the near term.

In one recent example, CBC reports that a London, Ont. condo owner’s monthly fees went up more than 35% in a year after the reserve study was updated. A $5,000 special assessment was also issued to each owner to replenish the condo’s reserve fund.

What Is a Special Assessment?

Unfortunately, in cases where either a major, unexpected expense happens or there is a large repair that goes over the amount set out in the reserve fund, condo owners may be on the hook by way of a special assessment.

As the Condominium Authority of Ontario notes, special assessments are one-time, mandatory fees that can be added to a condo owner’s common expense fees to cover budget shortfalls.

Your condo corporation decides how much you’ll have to pay, with each owner’s portion calculated using the same percentage used to calculate the common expenses fee.

The Condo Insurance Blind Spot

As a complement to the master condo or strata insurance policy that your building is required to have, which generally covers the building structure, common elements and certain original unit features, individual condo insurance policies cover your personal property, the cost of replacement to upgrades you’ve made to your unit and provide liability protection in the case that someone is injured inside your unit.

Some insurers also offer loss assessment coverage as an optional add-on to your policy. This insurance covers you in the case where there is damage to common areas (from disasters such as fires or storms), and repair costs exceed the master policy’s insured amounts or the condo is required to pay a deductible, and these costs are passed down to the owners.

It’s important to know, however, that this add-on only covers insured damage. It doesn’t extend to the cost of regular repairs (or special assessments) that would be covered by the reserve fund.

Key Advice from MyChoice

- Take note of how old your condo building is. Older condos often have a higher risk of expensive repairs to plumbing, parking areas, elevators, and other systems.

- You might want to add loss assessment coverage to your condo insurance. It won’t cover reserve fund shortages, but it could help with some assessments that come from insured losses.

- Before you buy a unit, ask about the reserve fund balance, upcoming projects, and whether there have been special assessments in the past.