How Much Is Renters Insurance in Ontario in 2026?

The average cost of renters’ insurance in Ontario is between $190 and $400 per year, depending on your city and personal circumstances. If you’re in the process of apartment hunting in Ontario, knowing how tenant insurance varies can better inform your budget decisions.

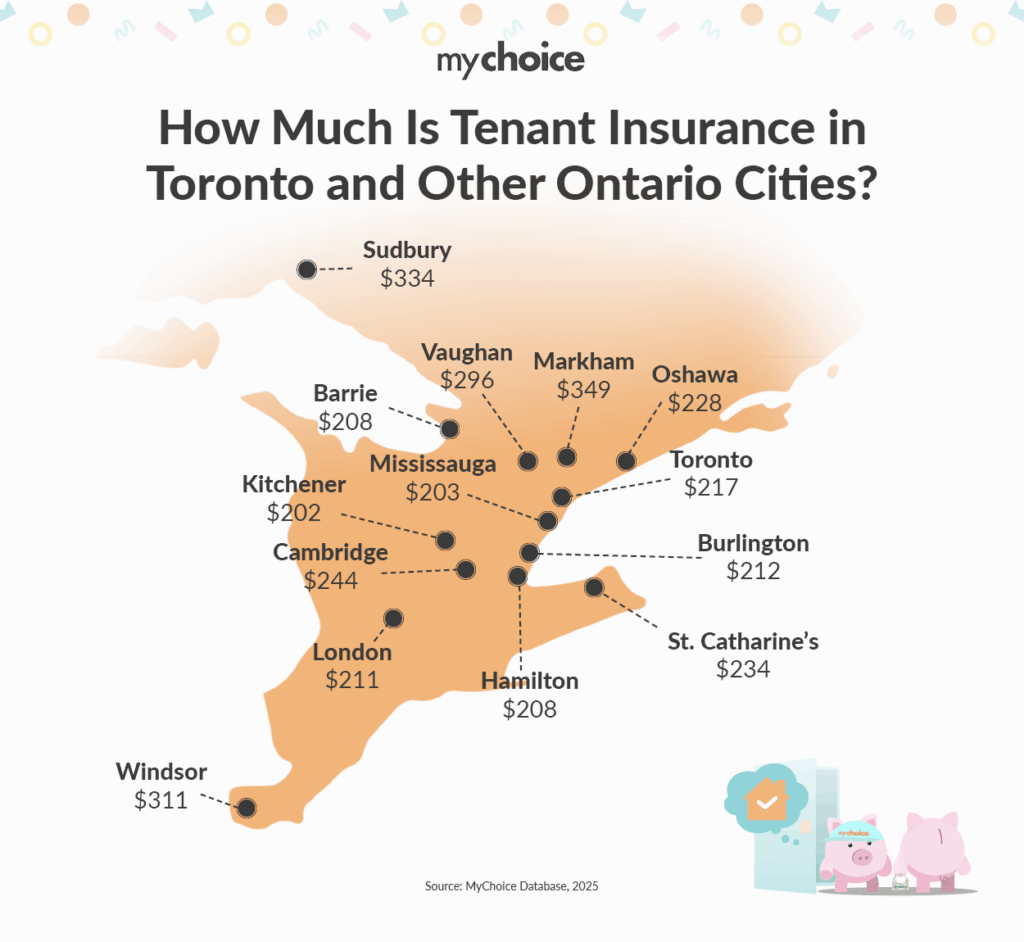

The Cost of Tenant Insurance Across Ontario Cities

Location is one factor that influences how much you pay for tenant insurance. Here are the average prices for renters’ insurance in Toronto and other Ontario cities.

| City | Average Rate |

|---|---|

| Barrie | $208 |

| Burlington | $212 |

| Cambridge | $244 |

| Hamilton | $208 |

| Kitchener | $202 |

| London | $211 |

| Markham | $349 |

| Mississauga | $203 |

| Oshawa | $228 |

| St. Catharine’s | $234 |

| Sudbury | $334 |

| Toronto | $217 |

| Vaughan | $296 |

| Windsor | $311 |

Ultimately, how much you pay for tenant insurance depends on your unique living circumstances. These are just general averages.