The increasing cost of living and higher mortgage rates force many cash-strapped homeowners to get very creative with how they pay off their mortgages, from adding tenants to allowing extra family members.

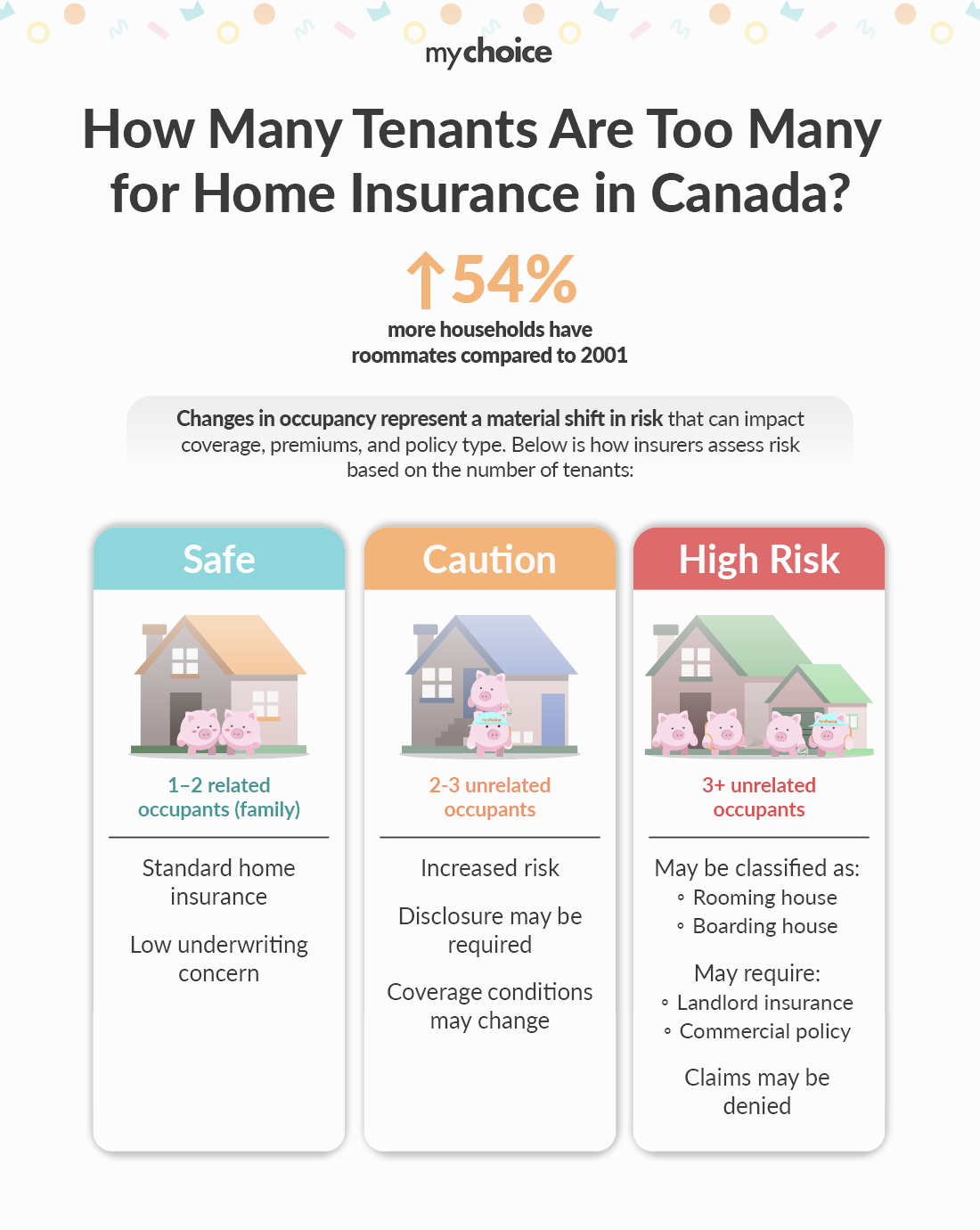

About 6.4 per cent of the population currently live in a multigenerational household, and 19.5 per cent of Canadians live in an intergenerational household with kids over age 20. As for the number of households consisting of roommates, they grew by 54 per cent between 2001 and 2021.

Why is Occupancy Important for Home Insurance?

The occupancy details of your home play a key role in how insurers assess risk and calculate your premium. Changes to who lives in your home and why they are living there can constitute a material change in risk.

For example, a home where one family lives is seen as less risky to insure than a place with several unrelated tenants. If the number or type of tenants living in your home changes, your insurer might review your policy, which could affect your coverage, price, or even the kind of insurance you need.

How many roommates are allowed under one home insurance policy?

Many homeowners don’t realize that home insurance policies limit how many unrelated people can live in a house before the property changes its designation.

While there is no universal rule, many insurers begin to flag properties with three or more unrelated occupants as higher risk. If too many unrelated tenants live in the home, it may be classified as a rooming or boarding house, which typically requires a different type of insurance policy.

This is where the distinction between home insurance and landlord insurance becomes important. A standard home insurance policy is designed for owner-occupied properties. Once you begin renting out rooms or bringing in tenants, the risk profile changes, and you may need landlord insurance, or a combination of both, depending on your living arrangement.

How Does it Differ for Condos?

Condos introduce an additional layer of rules beyond insurance, as both insurers and condo corporations may impose limits on occupancy.

Condo corporations often limit the number of occupants to prevent excessive wear and tear, property damage, and disruptions to other residents. These limits are influenced by municipal property standards and building codes, which may set minimum space requirements per occupant or guidelines around sleeping arrangements.

What Happens If You Cross the Occupancy Limit?

Exceeding occupancy limits or failing to disclose changes in your living arrangement can have serious consequences from an insurance standpoint.

If your insurer determines that your property no longer fits the original risk profile, your policy may no longer apply as intended. In some cases, claims can be denied due to misrepresentation or undisclosed material changes.

Key Advice from MyChoice

- Check your homeowner’s insurance to determine how many people, related or unrelated, can live in your home under your current policy.

- Look into your condo corporation’s rules as well as your own insurance policy to ensure you’re compliant with any occupancy restrictions.

- Let your insurer know of any living situation changes, such as new occupants, before and after they move in. This allows them to update your coverage, adjust your policy if needed, and ensure there are no gaps in protection. Failing to inform your insurer of material changes, such as adding occupants, can impact your coverage.