How Does Earthquake Insurance Work in Canada?

Earthquake insurance is not part of a standard home insurance policy. It’s typically offered as an optional top-up endorsement that you need to request for an extra charge, much like sewer backup or flood coverage.

Here’s a simple breakdown to help clarify what earthquake insurance actually does:

| Typically Covered | Typically Not Covered |

|---|---|

| Damage to your home’s structure from shaking | Flood damage caused by tsunami (unless flood insurance is added) |

| Detached buildings on your property (garage, shed) | Pre-existing damage or poor maintenance issues |

| Your personal belongings (furniture, appliances, clothing) | Fencing, landscaping, patios, or pools |

| Additional living expenses (hotel stays, food, rentals) | Damage due to unrelated causes (fire, theft) unless separately covered |

| Condo loss assessments due to earthquake-related damage | Damage outside your policy area or timeframe |

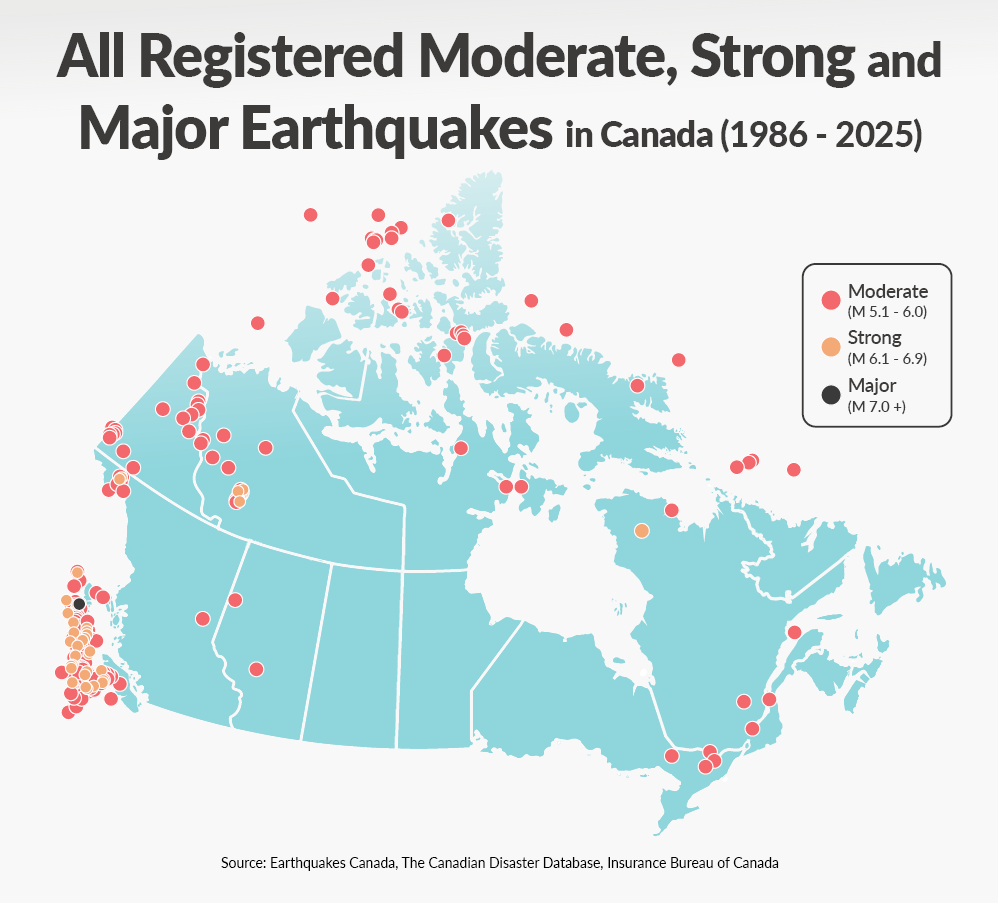

Which Parts of Canada Face the Highest Earthquake Risk?

Earthquakes are not equally distributed across Canada. While some areas are relatively stable, others face consistent and major seismic activity. Based on data from Earthquakes Canada between 1986 and 2025, here’s what we know about which parts of Canada face high earthquake risk:

How Much Does Earthquake Insurance Cost?

Earthquake insurance in Canada usually ranges from around $40 per year in low-risk regions to $400 or more annually in high-risk areas such as British Columbia, based on a home valued at $1 million.

Your insurance premium will ultimately depend on multiple crucial factors:

Who Should Seriously Consider It?

Earthquake insurance isn’t necessary for every homeowner, but for many Canadians, especially those in higher-risk areas, it’s a key form of protection. Here’s a breakdown of who should strongly consider adding it to their policy.

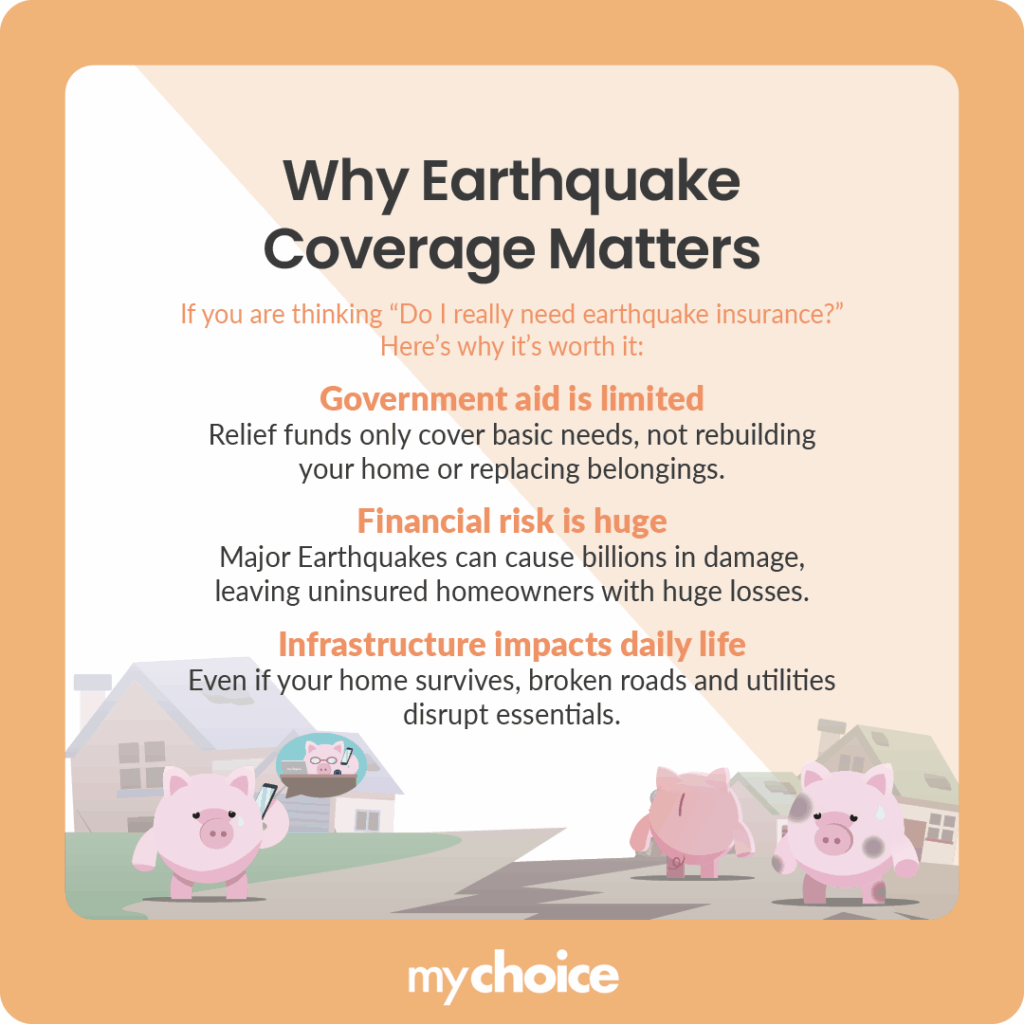

Why Having Earthquake Coverage is Important

Asking yourself, “Is earthquake insurance worth it?” Here’s why you shouldn’t leave yourself exposed to this potential natural disaster:

Key Advice from MyChoice

- Seismic retrofits like bolting your home to its foundation or strengthening walls can reduce quake damage and may lower your insurance costs. Ask your insurer if they offer discounts for earthquake-resistant upgrades.

- If a major earthquake disrupts your area, you may not have access to physical files. Save a digital copy of your policy and key contacts on your phone and on digital cloud storage.

- In the event of a claim, insurers will ask for proof of lost or damaged items. Keep a detailed inventory with photos or videos of your belongings, especially high-value items.