Home Insurance Inflation Rises 4.01% in Canada in 2026

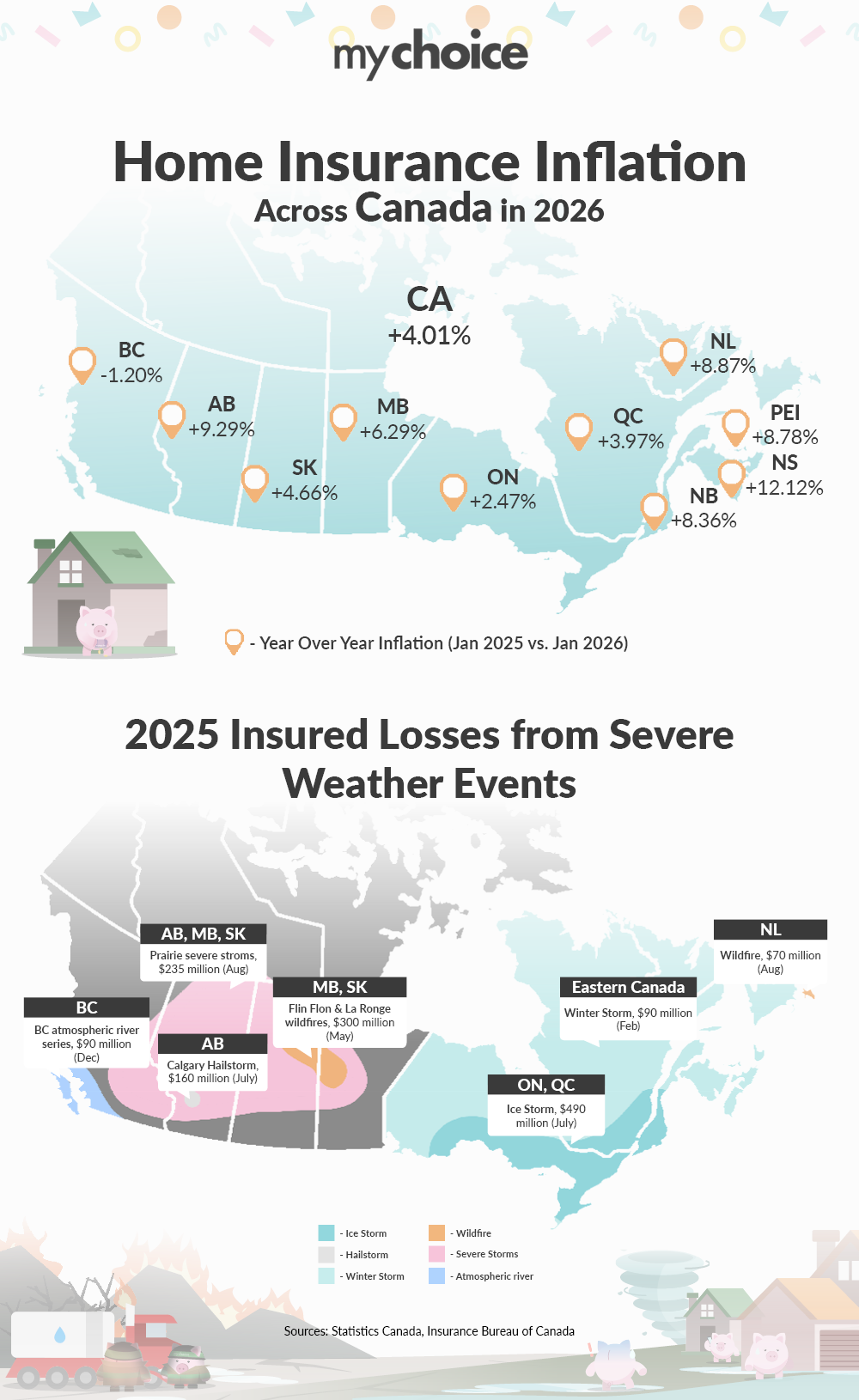

As we move into 2026, Canadian homeowners continue to face rising home insurance costs. National home insurance inflation came in at 4.01% year-over-year (January 2025 vs. January 2026), still well above the general inflation rate of 2.3%.

While inflation has cooled across parts of the economy, homeowners’ insurance remains under pressure from a combination of factors: a steady stream of weather-related losses, rising repair and rebuilding costs, and the growing impact of aging housing stock across Canada.

In light of these trends, MyChoice conducted a nationwide analysis of home insurance inflation using our proprietary quote data, alongside the Shelter Consumer Price Index. We reviewed provincial trends, examined the impact of 2025’s major weather events, and assessed how structural risks, such as renovation costs and home condition, continue to shape pricing.

Key Findings from the Study

- Home insurance premiums in Canada increased by 4.01% in 2026, continuing a multi-year upward trend.

- Atlantic Canada saw the highest increases, led by Nova Scotia (+12.12%), Newfoundland and Labrador (+8.87%), PEI (+8.78%), and New Brunswick (+8.36%).

- Alberta remains one of the most volatile markets, with premiums rising 9.29% following another year of severe weather losses.

- Ontario (+2.47%) and Quebec (+3.97%) saw more moderate increases, despite experiencing one of the most expensive weather events of the year.

- British Columbia was the only province to see a decline (-1.20%), though underlying risks remain elevated.

- 2025 weather-related insured losses exceeded $2.4 billion, marking another multi-billion-dollar year for catastrophic weather in Canada.

Atlantic Canada: A Region to Watch

One of the most notable shifts in 2025 was the growing risk profile of Atlantic Canada.

The Kingston wildfire in Newfoundland and Labrador, which caused over $70 million in insured damage, forced evacuations of more than 3,000 residents and impacted multiple communities. Historically considered a lower-risk region for wildfire, this event highlights how risk patterns are shifting geographically.

As a result, insurers are beginning to reprice risk more aggressively in the region, which is reflected in the double-digit premium increases seen across several provinces.

Beyond Weather: The Hidden Drivers of Insurance Inflation

While climate-related disasters remain a major factor, they are no longer the only driver of rising premiums.

Repair and Rebuild Cost Inflation

Construction and renovation costs continue to rise across Canada, making claims more expensive to settle. According to our recent study, many cities are experiencing 3%–6% annual increases in repair costs, with some markets reporting even higher increases.

From an insurance perspective, this means that:

- A roof replacement costs more

- Water damage claims are more expensive

- Full rebuilds require significantly higher payouts

Even in years with fewer disasters, higher claim severity alone can push premiums upward.

Aging Housing Supply

Another major, often overlooked factor is Canada’s aging housing stock. As highlighted in the above-mentioned study on housing conditions and insurance pricing, many Canadian cities face a trifecta of a high share of homes built before 1960, rising rates of deferred maintenance, and rising renovation costs.

In cities like Winnipeg, Montreal, and Regina, older homes combined with rising repair costs are creating a compounding risk effect. Older homes are more prone to water damage, electrical issues, and structural failures — all of which increase claim frequency and severity.

As Matthew Roberts, COO of MyChoice, notes: “Insurance pricing is no longer just about location and weather. The condition of the home itself is becoming a key risk factor. When repair costs rise, and maintenance is delayed, insurers are forced to price in that additional risk.”

Government Response and Market Stability

One of the most significant proposed solutions from the government has been Canada’s National Flood Insurance Program, designed to provide affordable coverage to the roughly 1.5 million households at high risk of flooding, many of whom currently struggle to obtain insurance in the private market. However, despite being first proposed in 2019 and reiterated in multiple federal budgets, the program has yet to be fully implemented. Industry groups and policymakers have continued to push for progress, but as of 2026, there is still no clear rollout timeline, and momentum appears to have slowed following consultations and election cycles.

At the same time, governments are investing heavily in climate adaptation infrastructure. Programs like the Disaster Mitigation and Adaptation Fund (DMAF) are funding projects such as upgraded stormwater systems and flood defences, including a recent $6.4 million investment in Nova Scotia aimed at reducing basement and surface flooding risks. These types of projects are critical, as flooding remains one of the most frequent and costly sources of insurance claims in Canada.

Wildfire resilience has also become a national priority. In 2025, federal and provincial governments jointly committed over $100 million to the FireSmart program, which focuses on reducing wildfire risk through community-level mitigation, vegetation management, and homeowner preparedness. The goal is not just to respond to fires, but to prevent them from causing large-scale insured losses in the first place.

What Can Canadian Homeowners Do Today

With multiple forces pushing premiums upward, homeowners should take a more proactive approach to managing their insurance costs.

- Review Your Coverage. Make sure your policy includes:

- Overland water protection

- Sewer backup coverage

- Replacement cost coverage

- Maintain Your Home

- Address small repairs early

- Upgrade outdated systems (plumbing, wiring, roofing)

- Reduce risk where possible

- Compare and Bundle Your Policies. Insurance pricing varies significantly between providers. Comparing quotes through platforms like MyChoice can help identify savings opportunities.

Raw Provincial Data:

| Province | Home Insurance Inflation (2025-2026) | Average Annual Home Insurance Premium (2026) |

|---|---|---|

| British Columbia | -1.20% | $2,253 |

| Alberta | +9.29% | $2,283 |

| Saskatchewan | +4.66% | $1,347 |

| Manitoba | +6.29% | $1,167 |

| Ontario | +2.47% | $1,458 |

| Quebec | +3.97% | $1,284 |

| New Brunswick | +8.36% | $970 |

| Nova Scotia | +12.12% | $1,034 |

| Prince Edward Island | +8.78% | $894 |

| Newfoundland & Labrador | +8.87% | $937 |

| Canada (National Avg) | +4.01% | $1,343 |