Does Home Insurance Protect From Tornado Damage?

Yes, home insurance does protect you from tornado damage. Most home insurance policies cover wind-related disasters such as tornadoes, hail, and storms, though other disasters like floods or earthquakes typically require additional coverage.

That said, it never hurts to double-check with your insurer and confirm that your policy has tornado protection.

What’s Covered by Your Home Insurance Policy?

Your home insurance policy usually covers your house, its contents, plus debris removal. Here’s a list of the most common things covered by home insurance:

- The building itself

- The contents of your home

- Detached structures, like a shed and fences

- Debris removal

Your insurer may also cover or reimburse living expenses if you can’t stay in the house during or after the tornado. You can also get optional pool and spa coverage if needed.

Every insurer’s range of coverage varies, so double-check with your insurance agent or representative to confirm what’s in your policy and what’s not. You might also need to pay a deductible before getting the promised amount of coverage.

What Happens if You Have to Evacuate

Your home insurance policy still works even if you need to evacuate. In some cases, policies reimburse living expenses for an initial period (often around 14 days for emergency evacuation), and longer if your home is damaged and requires repairs.

If your home needs repairs and you need to relocate longer, your insurer might extend your reimbursement period. Check with the insurance company to confirm the reimbursement limit.

Is Tornado Home Insurance in Canada Worth Buying?

Home insurance coverage for tornado damage in Canada is worth buying. Canada experiences the second-highest number of tornadoes in the world after the United States.

How many tornadoes hit Canada each year? Most weather experts estimate that Canada sees 60 to 100 tornadoes of varying sizes and severity each year.

The danger becomes even more pronounced if you live in an urban area around one of the country’s tornado-prone areas. In July 2021, a tornado in Ontario affected 110 properties, causing about $75 million worth of damage.

Home insurance in Ontario might be costly, but it’s worth getting in case another tornado like this hits. As you’ll want the best protection for your house, this makes choosing the best home insurance company even more important.

Making a Home Insurance Claim After a Tornado

Once the tornado has passed, you can get your home insurance paid out by making a claim. Here’s a general step-by-step on how to do so:

- Call your home insurance company representative.

- Clean the area around your house if possible. This helps prevent additional damage due to debris and water.

- Document the damage caused by the tornado. Note which areas are hit, and take photos to show your insurer later.

- Keep damaged items for the insurer’s assessment, as long as it’s safe to do so.

- Keep receipts and invoices for any costs you incurred during the cleanup process. You should also keep receipts of all living expenses incurred while away from home.

- Work with your insurance company to get the coverage paid out.

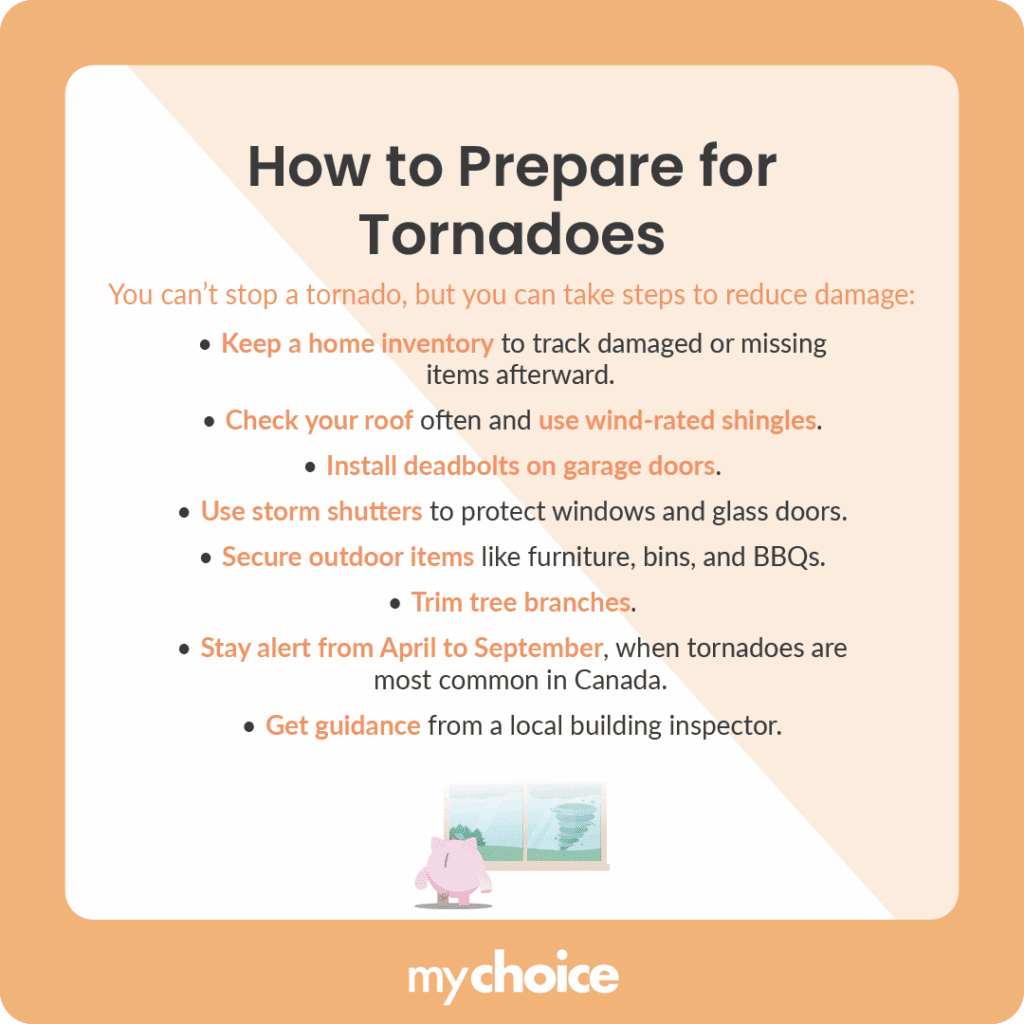

Preparing for Tornadoes

You can’t fully protect yourself from tornado damage if it passes through your area. But you can prepare for tornadoes and reduce the damage they cause when they hit.

Here are some tips to prepare your house for tornadoes:

- Keep an inventory list of the items in your house. This helps you note missing or damaged items when you check your home after the tornado.

- Inspect your roof regularly. Get wind-rated shingles and protect your vents. A well-maintained roof reduces the risk of shingles flying off and damaging your home or others around you.

- Get deadbolts for your garage doors to prevent the wind from opening them forcibly.

- Install storm shutters to protect your windows and glass doors from flying debris.

- Secure outdoor items like lawn furniture, garbage cans, and barbecue units. Unsecured outdoor items can turn into dangerous flying debris in a tornado.

- Trim your tree branches. A strong tree might not get uprooted, but branches can snap off and become flying debris.

- Be extra vigilant and prepared during tornado months. Tornadoes in Canada can happen year-round, but they most commonly happen from April to September.

- Ask for advice from a local building inspector. They know exactly what protective measures you can implement to reduce tornado damage, especially if your area is tornado-prone.

Key Advice from MyChoice

- Review your home insurance policy to confirm windstorm and tornado coverage, especially if you live in tornado-prone regions such as southern Ontario or the Prairies.

- Keep photos or an inventory list of your home and belongings. This can make it much easier if you ever need to file a tornado damage claim.

- Check the limits on your policy’s additional living expenses coverage to avoid potential gaps. These limits decide how much your insurer will pay if you need to move out temporarily.

- Make sure to keep your roof, windows, and outside structures in good shape. Insurers might deny claims if damage is caused by poor maintenance instead of the storm.