MAID Requests and Provisions Statistics in Canada

In Canada, just over 5% of people who died in 2024 received MAID – not a cause of death, but a health service provided as part of end-of-life care, accessible only in very limited circumstances, says Health Canada.

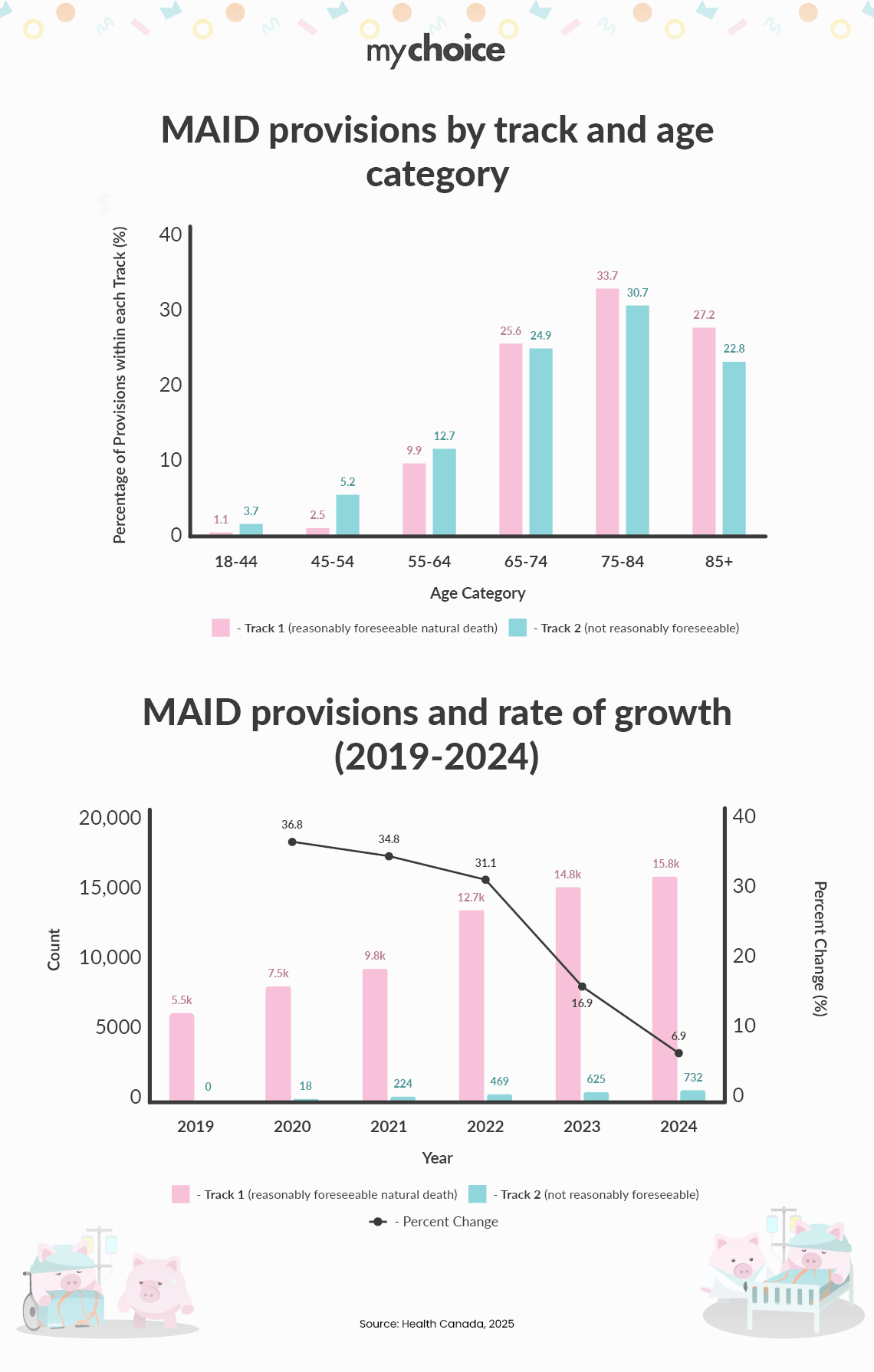

While the number of MAID cases has been increasing every year since 2019 (as seen in the below infographic, MAID was provided to 16,499 individuals in 2024, up 6.9% over 2023), the rate of growth in overall MAID cases has been declining since 2019, according to the government’s most recent annual report on MAID.

Originally approved for terminal illness in 2016, the government expanded MAID in 2021 to include non-terminal conditions. This category, called Track 2, made up only 4.4% of cases in 2024, with the most common underlying conditions listed as neurological and ‘other,’ such as diabetes, autoimmune conditions and chronic pain.

More than 95% of MAID cases were individuals whose death was reasonably foreseeable (Track 1) with most citing cancer as the underlying condition.

MAID eligibility

To be eligible for MAID in Canada, individuals have to meet strict criteria, including all of the following:

- be eligible for health services funded by a province, territory, or the federal government

- be at least 18 years old and mentally competent

- have a grievous and irremediable medical condition

- make a voluntary request for medical assistance in dying

- give informed consent to receive medical assistance in dying

Individuals requesting MAID are also subject to several procedural safeguards, such as having two independent medical assessments and making a written request that is independently witnessed.

In a case where medical practitioners determine that death is not reasonably foreseeable, extra safeguards must also be met.

How MAID Affects Life Insurance

From a life insurance perspective, choosing MAID does not, on its own, prevent a life insurance payout if all policy terms and disclosure requirements are met.

While many life insurance policies contain a “suicide clause” period, where they won’t pay death benefits if a person dies by suicide within the first two years, the Canadian Life and Health Insurance Association (CLHIA) noted in 2016 that MAID would not be considered “suicide” for the purposes of life insurance, as long as it takes place in accordance with the rules and processes set out by the government.

The Ontario government has also enacted legislation to prevent insurance benefits from being denied only because of a medically assisted death.

At the same time, even when MAID takes place within the rules, a claim may be denied if:

- Any misrepresentations were made when applying for coverage

- Certain medical conditions were excluded when the policy was issued

- The policy lapsed because premiums weren’t paid

Future Changes to MAID and Underwriting Questions

The issue of MAID eligibility is still evolving. For example, individuals whose sole underlying medical condition is a mental illness may also soon be eligible to apply for MAID, but not until March 17, 2027.

At the same time, the Alberta government recently tabled a bill that would limit the use of MAID to Track 1 cases where an individual’s death is reasonably foreseeable and likely to happen within 12 months.

The Federal government is still meeting on the topic of MAID expansion. The Canadian Parliament recently reconvened its special joint committee on MAID to review the eligibility of those whose sole condition is a mental illness and to assess the degree of preparedness for expansion.

At the moment, it is too early to know what an expansion of criteria might mean in terms of the number of individuals applying for MAID under Track 2 or whether/how this might affect life insurance underwriting and risk assessment.

But with this space continuing to evolve demographically and develop around areas like mental health, some in the industry note that insurers will have to stay adaptable, ensure policy language is clear, and underwriting and claims practices are consistent.

Key Advice from MyChoice

- Be transparent with your insurance company when applying for any life insurance products and ensure all information regarding underlying medical conditions is complete and accurate.

- Keep comprehensive records. Life insurance companies will require information on the underlying illness and a death certificate to indicate the underlying cause of death when MAID takes place, according to CLHIA. Insurance companies may also require documentation relating to the MAID process, consent and approvals.

- With this area continuing to evolve, it is always best to clarify the specific terms and provisions of your policy with your insurer.