To create this article, our team reviewed Canadian health data and medical research on sleep apnea, including prevalence rates, diagnosis trends, and the condition’s impact on long-term health outcomes. We also drew on our experience helping Canadians compare life insurance options to explain how sleep apnea is assessed during the underwriting process.

Why Sleep Apnea Matters to Your Life Insurer

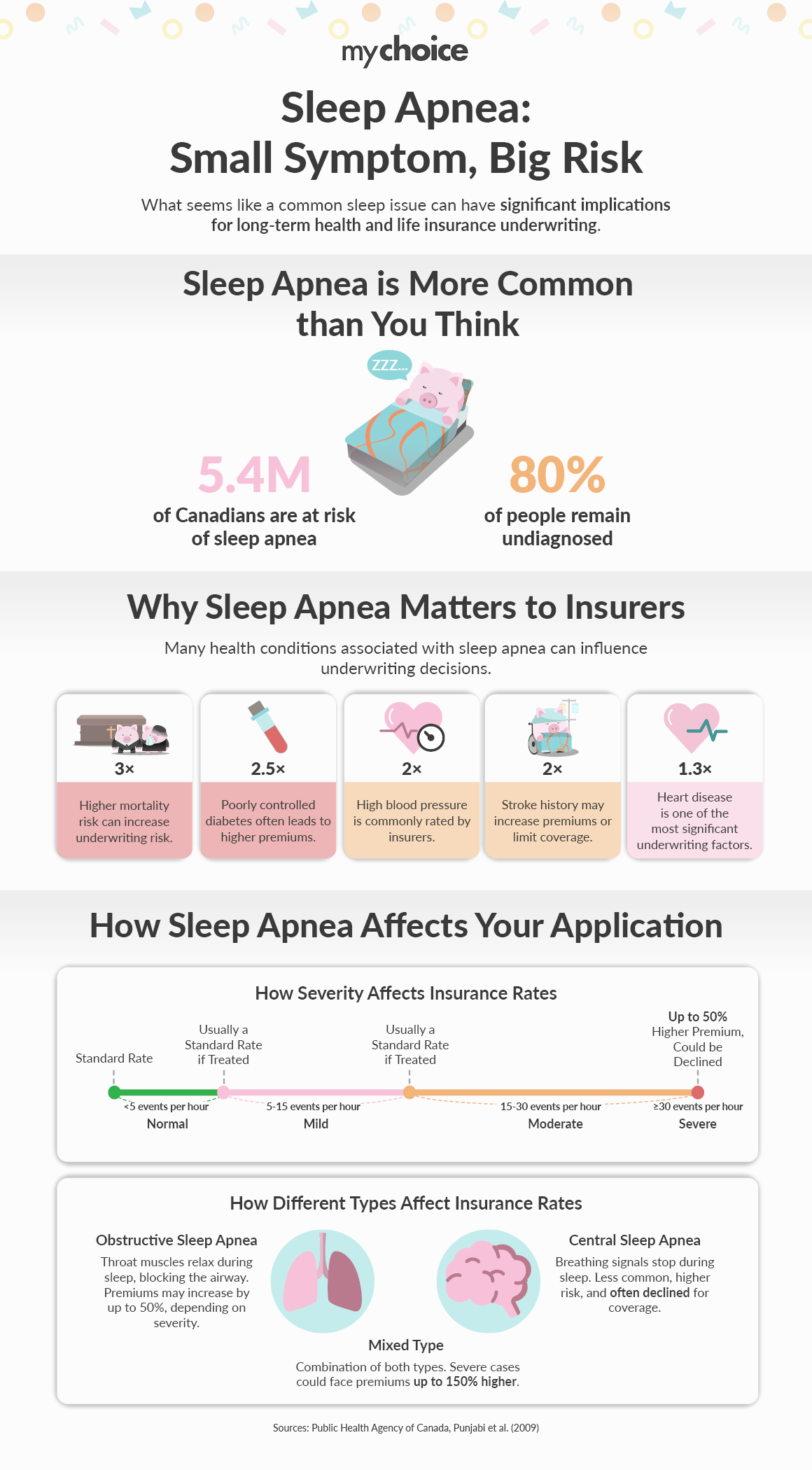

Sleep apnea can have a big impact on your health and potentially shorten your lifespan. Having the condition can leave you drowsy and more likely to have memory loss, reducing your concentration and raising your risk of motor vehicle accidents and work-related injuries.

This is why life insurers evaluate this condition during the underwriting process. They assess the severity of your sleep apnea using four factors:

- Severity: The Apnea-Hypopnea Index measures how many pauses in breathing you have per night.

- Treatment Compliance: This assesses whether you use a CPAP machine—which ensures your airway remains open—and delivers pressurized air.

- Last Sleep Study: Life insurers want to see evidence the sleep study was recent – such as within one to two years.

- Other health issues. This is to determine whether you have other conditions—such as high blood pressure or diabetes – which can cloud your overall medical picture.

Can You Still Get Insurance with Sleep Apnea?

It is possible to get life insurance with sleep apnea. Your situation depends on the insurer, the severity of your condition, how consistently you treat it, and your overall health.

Below are a few common cases based on the type of your condition:

Read More: How to Get Life Insurance After Being Denied Coverage

Is Sleep Apnea Common in Canada?

Sleep apnea is very prevalent in Canada, with 5.4 million Canadians living with, or at risk of, the condition. A disorder that stops your breathing for a few seconds – often many times per night, it has two causes:

- An airway blockage (obstructive sleep apnea). In this type, the muscles in your throat relax while you’re asleep, blocking your windpipe.

- A brain issue (central sleep apnea). With this form, your brain fails to send signals to allow you to keep breathing.

Because you’re usually asleep when it happens, up to 80 percent of people with sleep apnea aren’t formally diagnosed. It’s why the Canadian Lung Association urges anyone who is snoring loudly, gasping for air in their sleep and experiencing daytime drowsiness to be evaluated for sleep apnea. This involves undergoing sleep testing at a sleep clinic.

Once diagnosed, a person can successfully treat sleep apnea with a Continuous Positive Airway Pressure (CPAP) machine, which provides pressurized air through a mask to prevent upper airway collapse. Other treatment options include tongue-retaining devices that prevent the tongue from obstructing the airway, mouthguards and orofacial therapy.

How Sleep Apnea Affects Your Health

When sleep apnea causes you to stop breathing, this triggers you to wake up just long enough to resume breathing. But these frequent wake-ups, which many people are not aware of, can leave you tired and unrefreshed. Worse, untreated sleep apnea can cause:

- Heart arrhythmias (irregular heartbeat)

- High blood pressure

- Worsening of conditions such as diabetes

- Depression, bipolar disorder or mania

- Heart disease or damage to the heart

- Sudden cardiac death.

Overall, sleep-disordered breathing is associated with a higher risk of mortality due to heart disease, particularly in men aged 40-70.

Read More: How Strokes and TIAs Affect Life Insurance in Canada

What to Expect When You Apply

Here is the documentation you’ll need to have handy when applying for life insurance with sleep apnea: