Methodology

Direct comparisons of life insurance premiums across countries should be interpreted with caution because life insurance products, underwriting practices, tax rules, healthcare systems and employer-sponsored benefits differ significantly between markets.

To improve comparability, MyChoice analyzed publicly available insurer quotes using a standardized applicant profile: a healthy 35-year-old male non-smoker with an office-based occupation purchasing a 20-year level term life insurance policy with a CAD $500,000 equivalent death benefit, no riders or optional benefits, and standard or preferred underwriting where available.

Are Canadians Paying More for Life Insurance Than the Rest of the World?

The answer is no. At first glance, Canadian life insurance can seem expensive. However, international comparisons suggest Canadians generally pay premiums that are broadly in line with other major developed economies.

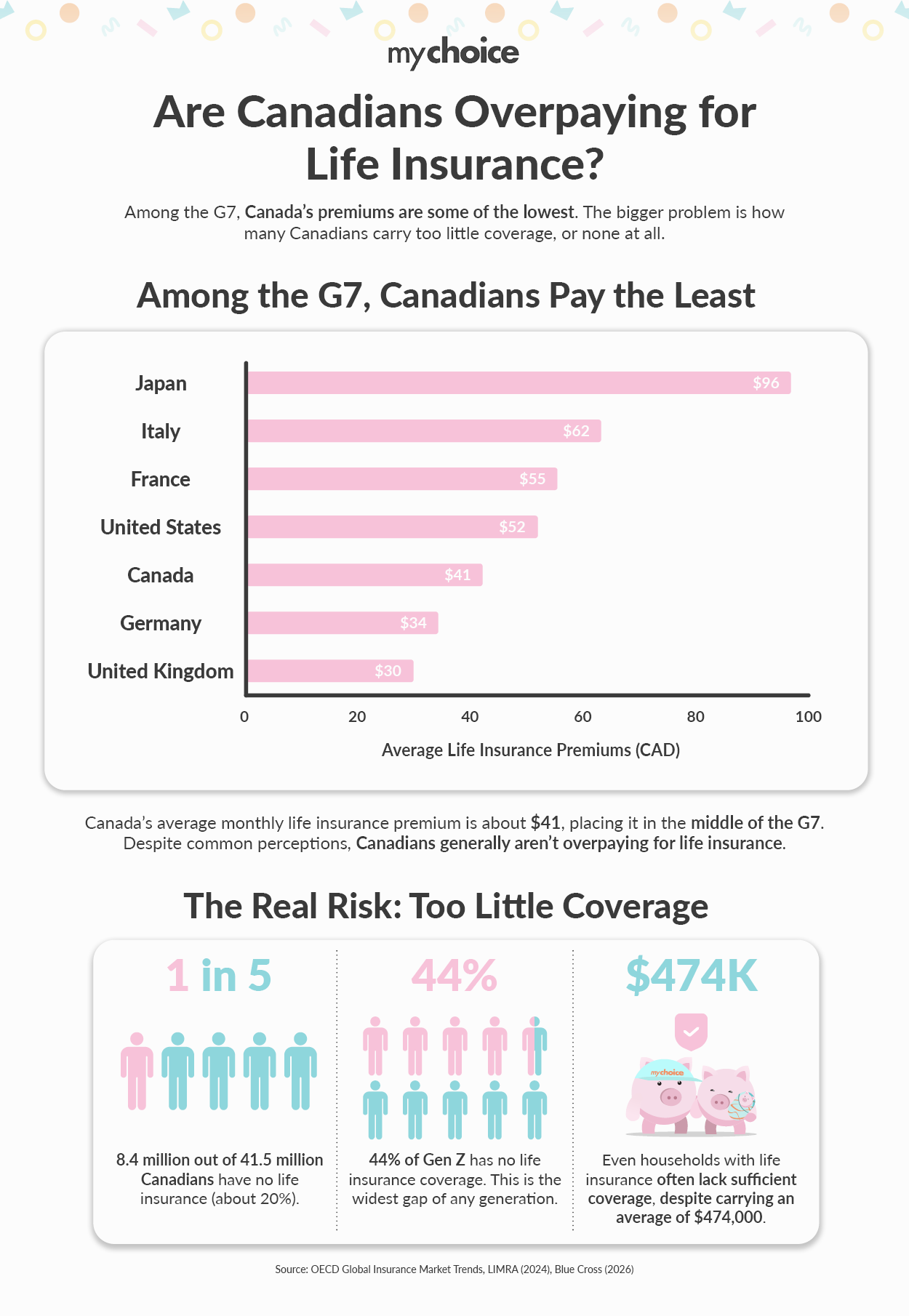

| Country | Monthly Premium (CAD) |

|---|---|

| United Kingdom | $30 |

| Germany | $34 |

| Canada | $41 |

| United States | $52 |

| France | $55 |

| Italy | $62 |

| Japan | $96 |

Canada ranks in the middle of the G7 for monthly life insurance costs. The United Kingdom and Germany have some of the lowest estimated premiums, while Japan has the highest among the countries reviewed.

Canada vs the U.S.: How do Premiums Compare?

Life insurance rates in Canada are comparable to those in the U.S.

In both countries, a healthy, 30-year-old non-smoker with $500,000 in life insurance coverage would pay between $20 to $50 a month. However, while Canadian term life policies increase at a steady pace upon renewal, American policies can soar on an annual renewal basis after the term expires.

Canada vs G7 Nations – Total Market Size

Canadians actually buy a significant number of life insurance policies. The total premium volume is estimated at $70.4 billion to $108.9 billion, depending on financial reporting.

Total premium revenue has continued to grow in Canada, reflecting strong demand for life insurance products. However, premium growth alone does not necessarily indicate whether pricing has increased or decreased over time.

Insurance Penetration: How Canada Compares

Life insurance penetration is the total value of life insurance premiums sold in a country divided by its gross domestic product. It’s a way of determining how life insurance impacts a country’s economy.

Countries such as Japan, the United Kingdom and France have higher levels of life insurance penetration than Canada. This reflects broader differences in financial systems, retirement planning, tax policy and consumer purchasing behaviour rather than premium pricing alone.

Canada’s Industry-wide market penetration is 3.8 percent, placing it in the middle of the pack.

- In the U.S., it’s between 3 percent and 5 percent.

- In the UK, it’s 8 percent.

- In Japan, it’s between 5 percent and 7 percent.

- In France, it’s between 5 percent and 7 percent.

Per Capita Spending on Life Insurance

Canada’s per capita life insurance, which is also known as insurance density, shows how much each person spends on life insurance.

In Canada, the average household has approximately $474,000 in life insurance coverage, while the life insurance premium per capita is $1,759 – much lower than other G7 nations such as the UK at $3,466, France at $2431 and Japan at $2,245. Compared to other G7 nations, Canadian spending on life insurance is relatively low.

| Country | Life Insurance Premium Per Capita (USD) |

|---|---|

| UK | $3,466 |

| France | $2,431 |

| Japan | $2,245 |

| US | $2,136 |

| Germany | $1,106 |

| Italy | $1,878 |

| Canada | $1,759 |

It’s important to note that life insurance represents only about 41 percent of Canada’s overall insurance market, compared with approximately 76 percent in Japan and 69 percent in Italy. Canadians generally spend a larger share of their insurance dollars on property and casualty coverage.

Canada’s Life Insurance Gap

Despite affordable premiums, a life insurance gap exists in Canada, meaning that there’s a big difference in how much life insurance Canadians have versus how much they need.

Many people falsely believe their employer-sponsored life insurance plans will provide adequate coverage to their families. Others incorrectly assume that life insurance is very expensive. Thirty-three per cent of Canadians actually overestimate premiums by over 300 percent. In reality, 20-year term life insurance for a healthy Canadian is often far more affordable than people expect.

As a result:

- 8.4 million Canadians have no life insurance coverage.

- Generation Z faces the largest protection gap, with 44 percent lacking coverage.

- Many households remain underinsured relative to their financial obligations and future income needs.

What Canada Can Learn from Other G7 Countries

Canada’s life insurance industry is growing. But there are still many Canadians who either have too little life insurance or no life insurance at all.

Other G7 nations have made progress on this front. In places like the U.S., employer-sponsored benefits and certain retirement accounts include life protection. In countries such as the United Kingdom, workplace pension auto-enrolment and widespread employer-sponsored benefits help many households build broader financial protection, although life insurance itself is not universally provided.

Key Advice from MyChoice

- Many people think life insurance costs more than it actually does. In fact, Canadians often overestimate the price, but Canada is about average among G7 countries for life insurance premiums.

- Take a look at the life insurance your employer offers. Workplace plans usually cover just one or two times your yearly salary, which might not be enough to fully protect your family’s future.

- Think about the protection your coverage offers, not just the monthly cost. Even a small payout now can give your family important financial support if something unexpected happens.