Can You Reinstate a Cancelled Life Insurance Policy?

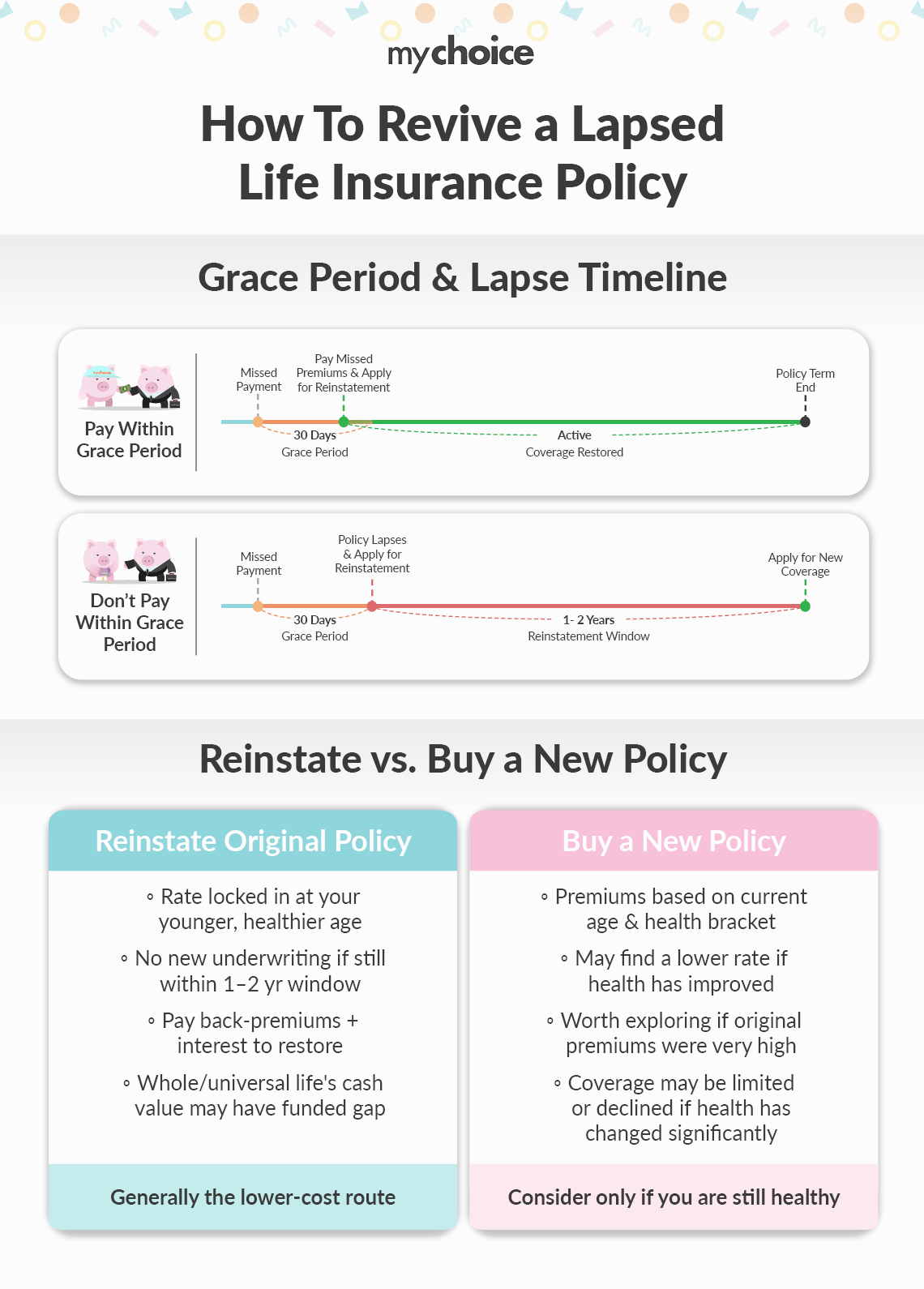

Yes, you can do so within the grace period after you pay your overdue premiums, including interest. If your insurer has cancelled your life insurance policy, request a reinstatement application.

If your policy has already lapsed, many insurers allow reinstatement for a limited period, often up to two years after the lapse date, although the exact timeframe varies by insurer and policy

During the reinstatement period, the insurer may request:

- A filled-out reinstatement application form.

- Payments for all missed premiums.

- Passing a health checkup and questionnaire, along with some medical information, such as blood work or blood pressure readings.

If the reinstatement period has expired, you will generally need to apply for new coverage and qualify under the insurer’s current underwriting requirements.

If My Life Insurance Coverage Has Lapsed, Should I Buy a New Policy?

Generally speaking, reinstating your original life insurance policy can yield a lower rate than buying a new one. That’s because when you first bought the policy, you were younger and likely healthier. Life insurance premiums generally increase with age.

In cases where you are still healthy, or healthier than when you first applied, and your premiums from your lapsed policy were very high, it can be a good idea to research what other providers are offering. You can use MyChoice to compare life insurance quotes before deciding whether to reinstate your existing policy or purchase new coverage. You may be surprised to find a considerably lower rate for the same amount of coverage – or a comparable rate despite the fact that you’re now older and in a new age bracket, from an underwriting perspective.

However, if your health has changed significantly since the policy lapsed, an insurer may decline reinstatement or require additional medical evidence before approving it.

What Happens If You Die During the Lapse Period?

If you die during the insurer’s grace period, your beneficiaries will still receive the death benefit in your policy. The insurer may deduct the premiums you failed to pay, along with interest, but the tax-free, lump-sum payment will still be paid.

If you die following the grace period, your policy will be considered terminated, and your beneficiaries will be paid nothing. As well, the premiums you paid into the policy will not be returned.

If you have a whole or universal life policy which accumulates cash value, the insurer may use these funds to keep the policy going. However, once that money has been used, the policy will officially lapse.

It’s a good idea for family members who are unclear on the status of a life insurance policy to contact the insurer immediately after the death of the policyholder to determine their next steps.

Can a Previously Lapsed Life Insurance Policy Affect Future Applications?

The answer is yes. A previous lapse may be considered by some insurers during underwriting, particularly if there have been multiple lapses or a history of missed payments.

They may:

- Request that you reapply all over again, including undergoing a medical exam. This could lead to higher premiums if your health status has declined since the last application.

- Deny coverage if you have had multiple lapsed life insurance policies.

How to Prevent a Life Insurance Policy from Lapsing

It’s easy to put in place a program that will prevent a life insurance lapse from ever occurring.

- Set up pre-authorized payments: By ensuring your payments are automated, you won’t miss any monthly or annual payments.

- Update any credit card changes. If your card expires or you receive a new credit card, be sure to let the insurer know right away.

- Read the fine print. Be aware of your insurer’s grace period to ensure you don’t pay beyond that time.

Key Advice from MyChoice

- If you miss a payment, get in touch with your insurer right away. Taking action during the grace period can often keep your policy from lapsing.

- Take some time to look over your policy’s grace period and reinstatement rules before you actually need them. These details can be different depending on your insurer and the type of policy you have.

- If your policy has lapsed, check how much it would cost to reinstate it and compare that to the price of getting a new policy before you decide what to do.

- Make sure your payment details are current, especially if you’ve changed banks, replaced a credit card, or switched accounts.

- Consider setting up automatic payments to reduce the risk of missed premiums and unintended coverage gaps.