Can Genetic Testing Affect Life Insurance?

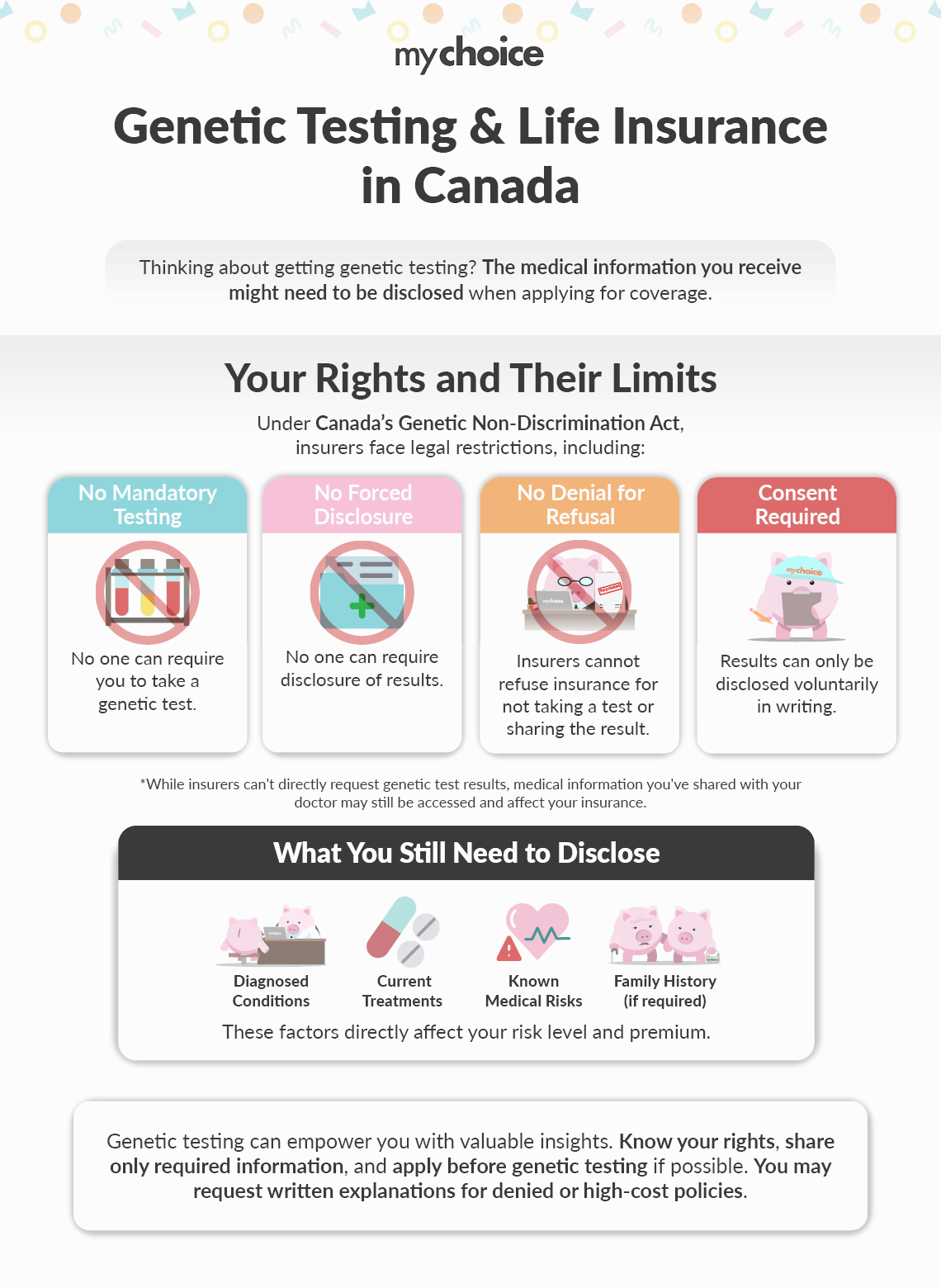

The Genetic Non-Discrimination Act prohibits insurers and other organizations from requiring you to undergo genetic testing or disclose genetic test results as a condition of providing services or entering into a contract. Violations can result in fines of up to $1 million or imprisonment.

The Law says:

- No individual can be required to take a genetic test.

- No one can require the disclosure of genetic test results.

- An insurer cannot deny coverage solely because an applicant refused genetic testing or declined to share genetic test results.

- A person can only disclose genetic test results voluntarily and on an informed consent basis, in writing.

“The conversation around genetic testing and life insurance often focuses on access to DNA, but that’s not really where underwriting decisions are made,” says Matthew Roberts, COO of MyChoice. “Insurers are ultimately pricing risk based on observable health signals such as family medical history, existing diagnoses, and treatment history. While Canadian law protects genetic test results from being directly required in most cases, related medical information may still become relevant during the underwriting process.”

What Medical Information Can Life Insurers Ask For?

Insurers need as much health information about you as possible when assessing you for life insurance. Under Canadian law, insurers generally cannot require applicants to disclose genetic test results, regardless of policy size.

However, if you’d like a larger policy, during the application interview, some insurers have been known to ask broad questions that can make you feel like you need to disclose genetic results. They might ask about:

- Your current state of health and lifestyle.

- The reasons you’ve visited a doctor recently.

- Your family’s medical history.

- What medical condition you’ve been diagnosed with.

- What treatments or medications you’re taking.

If you would like more life insurance coverage, with your consent, insurers may request access to relevant medical records during underwriting. If you’ve disclosed your genetic testing information to your doctor, that information might be shared with the insurer, especially if your medical records include diagnosed conditions, treatment plans, or documented hereditary risk factors.

This information can categorize you as a high-risk candidate and may affect your eligibility, underwriting classification, or premium pricing.

What Information You Need to Disclose

Applicants are generally expected to disclose relevant diagnoses, treatments, symptoms, and material medical information requested during underwriting. It’s what’s considered a ‘duty of utmost good faith.’ So, if you’ve learned through genetic testing that you’re at risk of Huntington’s Disease, a progressive, neurodegenerative disease, you may need to disclose related diagnoses, symptoms, or medical treatment if asked during underwriting.

If there’s a lack of clarity around your family history, you don’t disclose what treatment you’re undergoing, or you fail to mention you’re at high risk of a certain disease, that could constitute a material misrepresentation to the insurer. As a result, your application may be denied or your claim or policy voided at a later time.

What This Means for Canadian Life Insurance Applicants

Despite the Genetic Non-Discrimination Act, insurers may still review relevant medical information disclosed during underwriting or included in authorized medical records. That means that even if you don’t want to disclose information you’ve learned via genetic testing, there’s a certain medical information connected to diagnoses or treatment that may still become relevant during the underwriting process.

How to Protect Yourself When Applying for Life Insurance

It can be challenging knowing what to share and what not to share when applying for life insurance after having genetic testing. Here’s what you can do to protect yourself:

- Know your rights. If anyone requests your genetic testing results or tries to get you to undergo genetic testing, you have the right to refuse the request.

- Focus on facts: If you’re filling out insurance application forms, answer the questions asked as directly as possible without providing additional genetic information.

- Apply before you do genetic testing. If you are considering genetic testing, it may be helpful to review your insurance needs beforehand.

- Ask questions. If an insurer offers you a policy with a very high premium or rejects your application, ask for a written explanation.

- File a Complaint. If you feel you’ve been pressured into providing genetic information that led to a policy refusal, you can file a complaint with the Office of the Privacy Commissioner of Canada.

Additionally, you can read our guide on how to prepare for a life insurance medical exam.

Key Advice from MyChoice

- Be aware of your rights under Canada’s Genetic Non-Discrimination Act. Insurers usually cannot make you take a genetic test or ask you to share your genetic test results.

- Answer insurance application questions honestly and carefully. Only provide the information they ask for, and do not share extra medical details unless required.

- If your medical history is complicated, consider working with a licensed insurance advisor. Insurers may look at hereditary risks and medical history in different ways.