How Canada’s Multigenerational Households are Changing

- In 2021, 7.1 million people — one-fifth of Canada’s population living in a private household — lived in an intergenerational household, made up of parents and their adult children aged 20 and over.

- Ontario boasts the highest rate of intergenerational housing, with more than 23% of the province’s population living in this arrangement.

- An additional 2.4 million people lived in a multigenerational environment, with three or more generations of the same family.

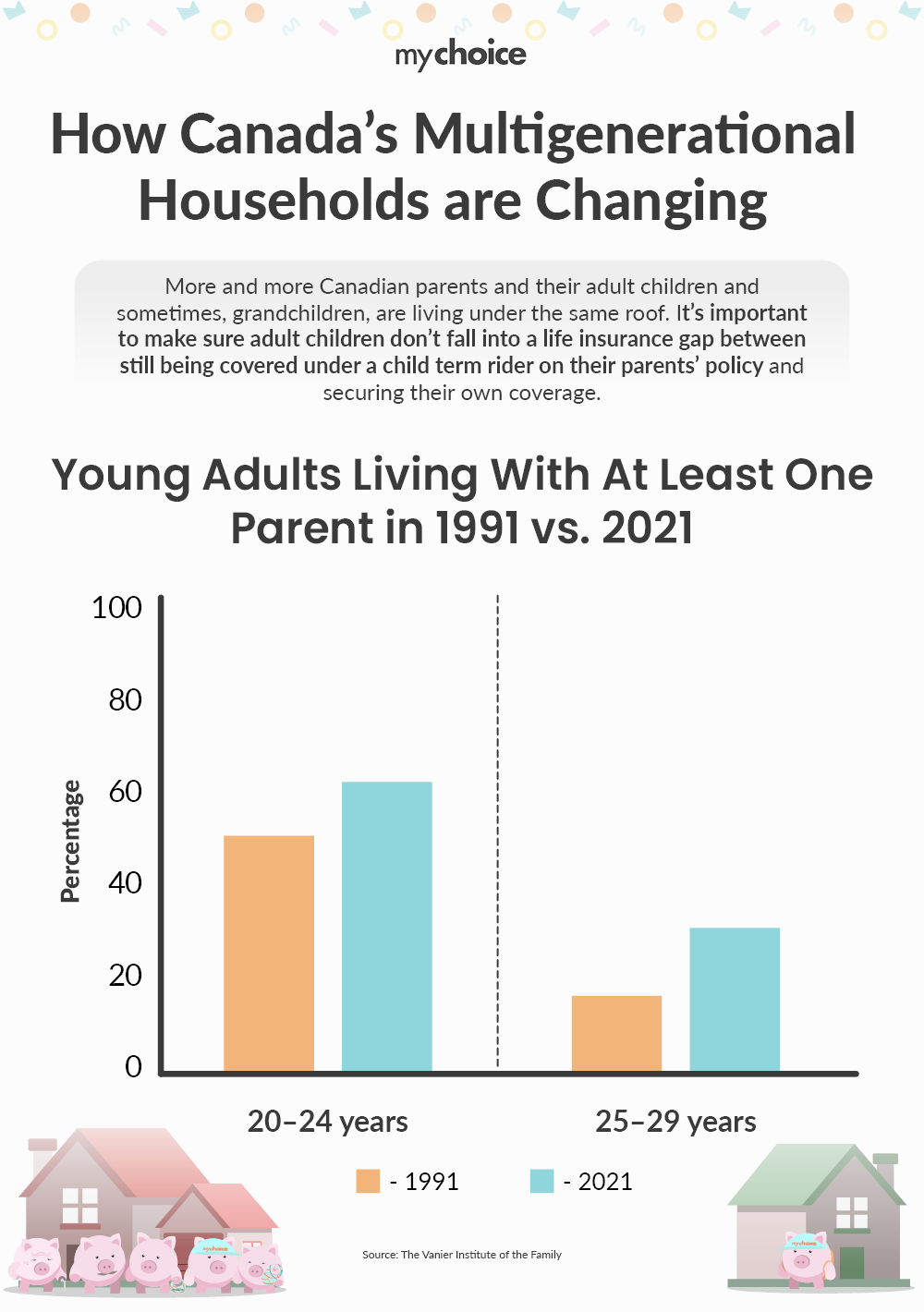

- Both categories have been on the rise in Canada in recent decades — the number of multigenerational households, for example, grew more than 21% between 2011 and 2021. Nearly 46% of young adults between 20-29 also lived with at least one parent in 2021, compared with 32% in 1991, according to The Vanier Institute of the Family.

Young adults in Canada aged 20-29 living with at least one parent

| 20-24 | 25-29 | |

|---|---|---|

| 1991 | 50.5% | 16.9% |

| 2021 | 62% | 31% |

Intergenerational households form for any number of reasons — in some cases, it looks like adult kids living with their parents to save money during post-secondary school. But as StatsCan notes, it may also be a strategy by parents and adult children to “share resources, manage expenses and provide mutual support.”

Commonly, it can also involve parents purchasing a house or co-signing on a property with an adult child to help them get a foot in the housing market.

In 2021, for example, Statistics Canada found that around one in six residential properties owned by people born in the 1990s were co-owned with their parents. Higher rates of co-ownership between parents and children were found in expensive urban markets like Toronto, Kelowna, Victoria and Vancouver.

In nearly 35% of these situations, parents and adult children co-owned a single property.

What is the Coverage Gap?

Depending on the circumstances, an adult child living at home may be covered on their parents’ life insurance policy, or they may be subject to a significant coverage gap, if they have yet to purchase their own insurance.

Some younger adult children living at home will fall under their parents’ life insurance policies under the ‘child term rider’ — an add-on to your primary insurance which will cover an adult child up to age 18 or 25, depending on the policy.

However, adult children over this age are required to purchase their own policies to ensure coverage.

But for many, this isn’t on the radar. For some young adults, other financial priorities such as a higher cost of living and servicing debt are causing them to delay applying for their own coverage.

Many consumers under age 40, as a recent survey by LIMRA and Capgemini found, are also postponing or skipping the traditional triggers for purchasing life insurance. For example, 63% have no immediate marriage plans, and 84% of both single and married people have no immediate plans to have a child.

What are the Financial Risks of the Coverage Gap?

Whatever the reason for putting off buying life insurance, this gap can lead to problems down the road for families.

A delay in securing adequate life insurance by an adult child can leave parents in a financial jam if the adult child passes away — especially in cases where they co-own a home together or where the adult child has taken on financial responsibilities in the family.

In this situation, parents would be left liable to repay the mortgage debt in its entirety or take on bills on their own, without the benefit of a life insurance payout, which could put their own retirement savings at risk.

Waiting to apply for life insurance can also be costly. Age and good health are the key factors insurance companies use to calculate premiums, but generally, younger, healthier people can lock in lower rates — so while procrastinating might seem like a budget-friendly option now, it can be a pricey decision later.

Key Advice from MyChoice

- Evaluate your life insurance coverage to determine whether your adult child is still covered under your policy’s ‘child term rider.’

- If the child term rider is near expiry, explore transitioning your rider into a permanent policy before your adult child reaches age 25.

- Weigh your family’s policy options and premium costs that are a good fit with your family’s needs and your budget. The good news is purchasing a policy in your 20s or 30s is usually cheaper than buying it later.