What Is Term Life Insurance?

Term life insurance is an insurance policy that covers you for a specific time period. Common coverage periods include 10, 20, and 30 years.

Your premium is typically fixed for the duration of the term, but it may increase if you renew the policy afterward. But it may increase if you choose to renew the policy once it ends.

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance that covers you until you pass away. Your protection won’t expire as long as you continue to pay premiums.

Lifelong coverage isn’t the only feature of whole life insurance. Most permanent policies also have a cash value component. This means part of your premium payment is reinvested to generate this cash value. You can then use this cash value as a source of funds or loan collateral whenever you need money.

Due to the long protection period and cash value retention, permanent policies are usually more expensive than term policies.

Universal life insurance is another type of permanent life insurance, alongside whole life. Learn how universal policies compare to whole-life policies.

Term vs Whole Life Insurance: What’s the Difference?

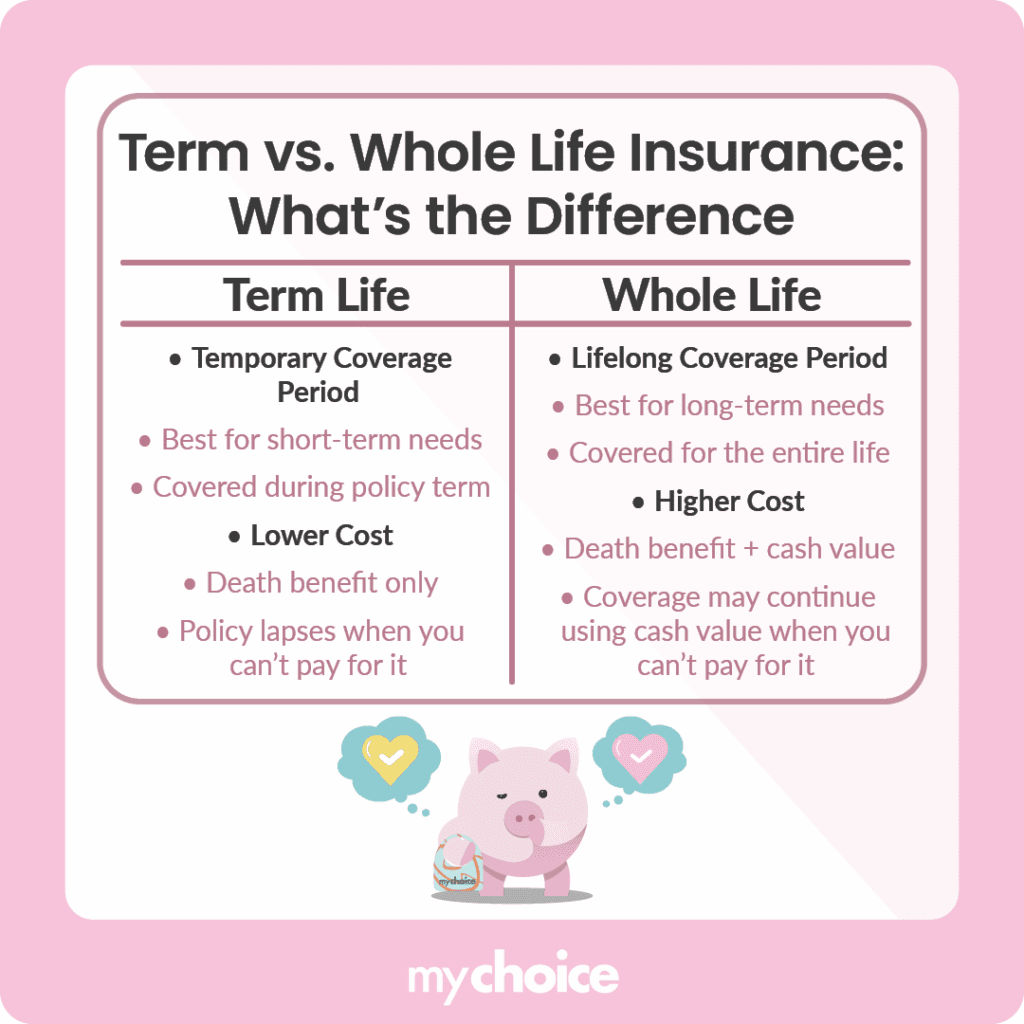

There are many differences between term and whole life insurance, as we’ve covered above. We’ll summarize most of the prominent distinctions in this table:

| Term life insurance | Whole life insurance | |

|---|---|---|

| Coverage period | Temporary | Lifelong |

| Best for | Temporary needs like mortgage or child’s education | Permanent needs like estate planning and retirement income |

| Guaranteed level premiums | Policy term | Entire life |

| Cost | Lower | Higher |

| Benefits | Death benefit only | Death benefit and cash value |

| Coverage after non-payment | Lapses after one month | may continue if sufficient cash value exists (depending on policy structure) |

Term vs Whole Life Insurance: Cost Comparisons

Cost is one of the primary concerns for insurance shoppers. As we’ve outlined, whole life insurance is significantly more expensive than term life insurance, but seeing the numbers side by side puts that difference into perspective.

Here’s a cost comparison between term 20 and whole life insurance for $500,000 coverage for a non-smoking individual across different age groups. Note that these rates don’t represent any one insurance company, and you should check with your insurer for detailed rate information.

| Age | Gender | Term-20 Life Insurance | Whole Life Insurance |

|---|---|---|---|

| 25 | Male | $27.00 | $209.25 |

| Female | $19.80 | $176.40 | |

| 35 | Male | $28.80 | $322.20 |

| Female | $22.05 | $276.30 | |

| 45 | Male | $63.45 | $522.00 |

| Female | $48.60 | $436.05 | |

| 55 | Male | $161.10 | $830.70 |

| Female | $115.20 | $663.75 |

Even from a young age, the cost of whole life insurance is already significantly higher than term life insurance, often several times more expensive depending on the payment structure. Taking a permanent policy is a major financial commitment, so be sure you’re financially ready to pay the premiums if you do.

Meanwhile, term life premiums are low when purchased at a younger age and remain fixed during the term, but new policies become more expensive as you age. That said, we recommend getting insurance at a young age to secure lower rates and save money.

Which Type of Insurance Is Right for Me?

There’s no one type of life insurance that’s right for everyone. The right insurance policy for you is the one that best suits your needs.

If you’re looking to get temporary insurance, then a term life policy is best for you. If you don’t mind shelling out more for lifelong protection and the investment component, whole life insurance is better for you.

Which Companies Offer Term and Whole Life Insurance in Canada?

Most Canadian companies offer term and whole life insurance. Ask your local insurance broker for more information about which company is the best for you. According to our most recent research on the top life insurance companies in Canada, Sun Life is popular for whole life insurance policies, while Primerica is famous for its term offerings.

Term vs Whole Life Insurance: The Bottom Line

Term life insurance and whole life insurance have their unique benefits and drawbacks. The most important thing when looking for life insurance is to choose the policy type that suits your needs.

Key Advice from MyChoice

- Pick term life insurance if you need coverage for things like a mortgage, replacing your income, or paying for your child’s education.

- It’s smart to buy life insurance early, since both term and whole life policies get much more expensive as you age.

- If you want to maximize returns, consider getting term life insurance and investing the money you save elsewhere rather than building cash value in a policy.