Are Life Insurance Payouts Taxable in Canada?

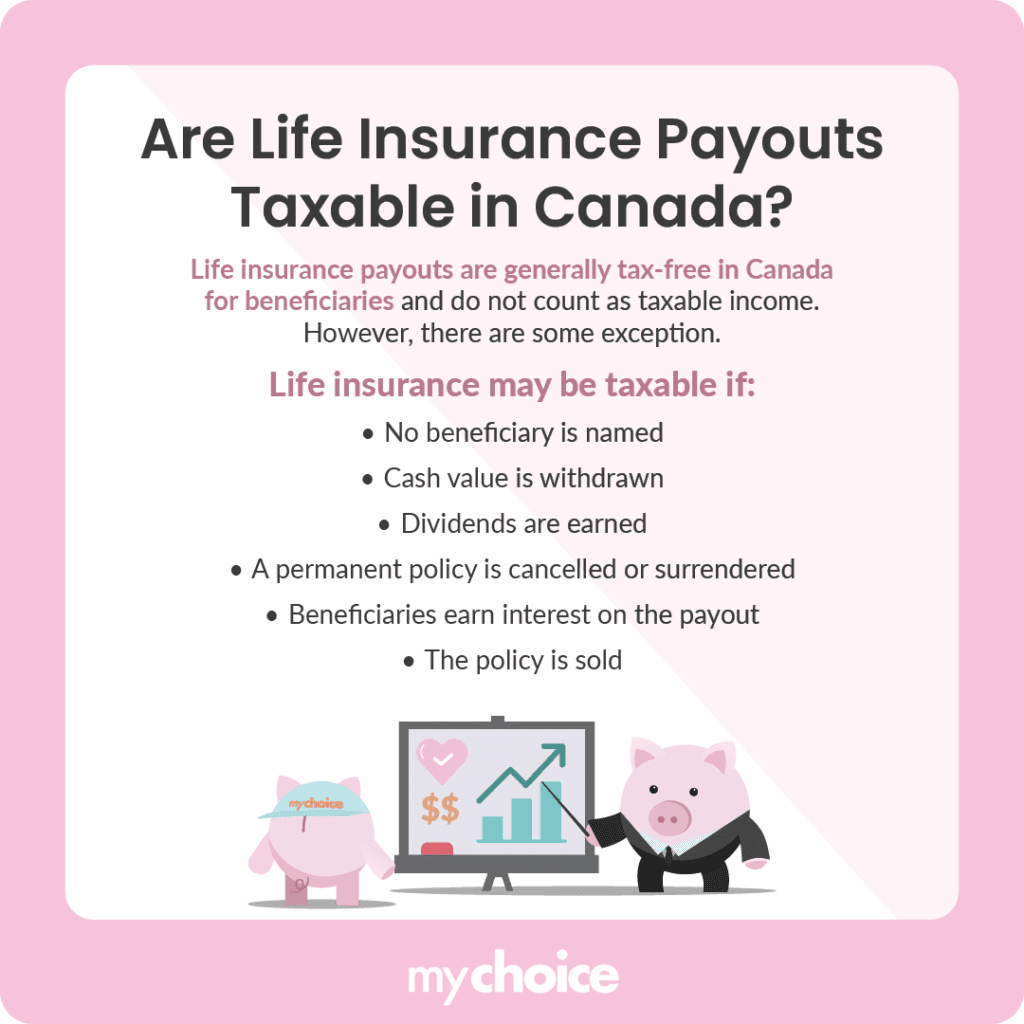

Life insurance payouts are generally not taxable in Canada. That said, you might have some additional questions.

Here, we’ll answer some of the most common questions about the tax consequences of life insurance in Canada.

Is Life Insurance Taxable Income to the Beneficiary in Canada?

Life insurance isn’t taxable income to the beneficiary in Canada. A death benefit paid out to named beneficiaries is tax-free, and they don’t have to report it as additional income.

Life insurance death benefits are generally not taxable in Canada. However, taxes may apply in related situations, such as:

- If the policy pays out interest after death, that interest is taxable

- If the policy has cash value withdrawals or surrender gains exceeding the adjusted cost basis (ACB)

- If the policy is sold or transferred, triggering a taxable disposition

- If the payout goes to the estate, it may be subject to probate fees (not income tax)

- If a corporation is the beneficiary, special tax rules apply (e.g., capital dividend account treatment).

Is There HST on Insurance Premiums?

Insurance premiums are generally exempt from GST/HST because they are considered financial services.

Life Insurance Taxes on Permanent Policy Cash Value

One of the benefits of permanent life insurance is that it builds cash value over time. You can withdraw this cash for various purposes when needed.

There are three common ways of withdrawing cash from a permanent policy, each with its own tax consequences. Let’s dive into each withdrawal method and examine how you’ll be taxed when you withdraw money.

Insurance Policy Withdrawals

Most permanent life insurance policies have a cash value you can take from. You can withdraw some or all of it for various purposes, usually with a fee. However, you’re subject to life insurance tax if you withdraw your policy’s cash value.

How much is the tax? It depends on how much you withdraw and your adjusted cost basis (ACB). Here’s a table with the details and a withdrawal example:

| Policy details | Value |

|---|---|

| Life insurance policy’s cash value | $100,000 |

| Policy’s ACB | $75,000 (75% of the cash value) |

| Withdrawal amount (example) | $20,000 |

| Withdrawal ACB | $15,000 (75% of withdrawal amount) |

| Taxable withdrawal amount | $5,000 |

As seen in the table above, you get taxed for the amount of money exceeding the ACB. In this case, $5,000.

Insurance Policy Loans

Insurance policy loans are another way to get money from your permanent life insurance. Unlike withdrawals, you can repay a policy loan, so you won’t reduce your death benefit.

Policy loans may trigger taxes if they create a policy gain, typically when the amount borrowed exceeds the policy’s adjusted cost basis (ACB).

Here’s a table for illustration:

| Policy details | Value |

|---|---|

| Life insurance policy’s cash value | $100,000 |

| Policy’s ACB | $75,000 (75% of the cash value) |

| Loan amount example | $80,000 |

| Taxable loan amount | $5,000 |

Your taxable life insurance cash value amount is $5,000 because you loaned $80,000, which is $5,000 over the ACB.

Insurance Policy as Collateral

You can use your permanent insurance policy’s cash value as loan collateral. Loans from a third-party lender using your policy as collateral are generally not taxable. However, policy loans taken directly from the insurer may have tax implications. Moreover, there won’t be any tax consequences if you can repay the loan during your lifetime.

If you die before repaying the loan, the proceeds from your policy will be used to repay the loan first.

Is the Cash Surrender Value of Life Insurance Taxable in Canada?

Your life insurance’s cash surrender value is taxable in Canada. You get taxed on life insurance cash surrender value because it counts as withdrawing cash from your policy. The Canada Revenue Agency (CRA) sees any cash value you receive as income, which is subject to tax.

Is Life Insurance Tax-Deductible?

Generally, life insurance premiums aren’t tax-deductible. However, there are some conditions where your life insurance premiums can be tax-deductible. This is a nuanced question; thus, we wrote a separate article in which we dive deep into the topic of whether life insurance is tax deductible in Canada.

Reporting Life Insurance Payouts on Tax Returns

Death benefits aren’t taxable – at least, in most cases. Usually, your beneficiaries receive the death benefit tax-free. They don’t have to declare it as taxable income, either.

Life insurance is taxable only under certain conditions we’ve covered earlier in the article. Here, we’ll cover what happens when your beneficiaries receive taxable death benefit payouts.

Reporting Policy Dividends

Any dividends or interest earned on the policy (or after payout) may be taxable, but the core death benefit remains tax-free. If you pass away with taxes owed on your life insurance dividends or interest, the insurer will give your beneficiaries a T5 slip. Then, beneficiaries have to report the income on their tax return.

Life insurance dividend income goes into lines 12000 and 12010, while interest income goes into line 12100.

What Happens When You Don’t Name a Beneficiary?

When you don’t name a beneficiary, your death benefit payout goes into your estate. If no beneficiary is named, the payout goes to the estate, where it may be used to cover debts, taxes, and probate fees. Moreover, it’s also subject to probate fees or estate administration tax.

All these costs add up, so your family or heirs might only receive a small part of your death benefit payout when all the costs are paid. Naming a beneficiary for your insurance payout ensures the money goes right to them, not your estate. Better yet, your beneficiary will receive your life insurance proceeds tax-free.

You don’t always have to name people as beneficiaries, either. You can name organizations like charities or communities as your beneficiaries.

Avoiding or Reducing Taxes on Life Insurance

Life insurance payouts are generally not taxable, so your beneficiaries often don’t have to avoid or reduce taxes. The best way to avoid taxes on your life insurance payout is to name beneficiaries, so your death benefit won’t go into your estate.

But if your policy pays dividends or you gain interest on it, your death benefit may eventually be subject to tax. There are usually a lot of tax consequences at play, so you might benefit from working with insurance advisors or tax accountants. They know how best to reduce or avoid taxes on your life insurance payout.

Making Life Insurance Claims Easier for Your Beneficiaries

Your family will likely have a hard time dealing with your passing. Unfortunately, claiming life insurance and dealing with the tax consequences can stress them out further.

But you can take measures to make things easier right now. Here are several things you can do to make life insurance claims easier for your family:

- Name your life insurance beneficiaries. This allows you to bypass the estate and ensure your beneficiaries fully receive your death benefit.

- Give your beneficiaries access to your insurance provider’s information and policy documents. This saves them a lot of time digging through paperwork when it’s time to claim the death benefit.

- Be detailed in your listing of beneficiaries. Include their full names and social security numbers to eliminate ambiguity. If your beneficiaries are organizations, list their full name, tax ID number, and complete address.

- Name contingent beneficiaries in case your primary beneficiaries can’t accept the death benefit.

- Check and update your life insurance policy after major life events like marriage and childbirth.

Key Advice from MyChoice

- Be sure to name a beneficiary. This helps you avoid probate and makes sure your payout goes straight to your loved ones in a tax-efficient way.

- Take time to learn how your policy’s cash value works before you withdraw or borrow from it, since this could lead to unexpected taxes.

- If you are considering a policy loan or using your policy as collateral, do so carefully. Some options may save you more on taxes than simply withdrawing money.

- Check your policy after big life changes like getting married, having children, or changing your financial goals. This helps keep your beneficiaries and coverage up to date.