The Growing International Operations of Canadian Insurers

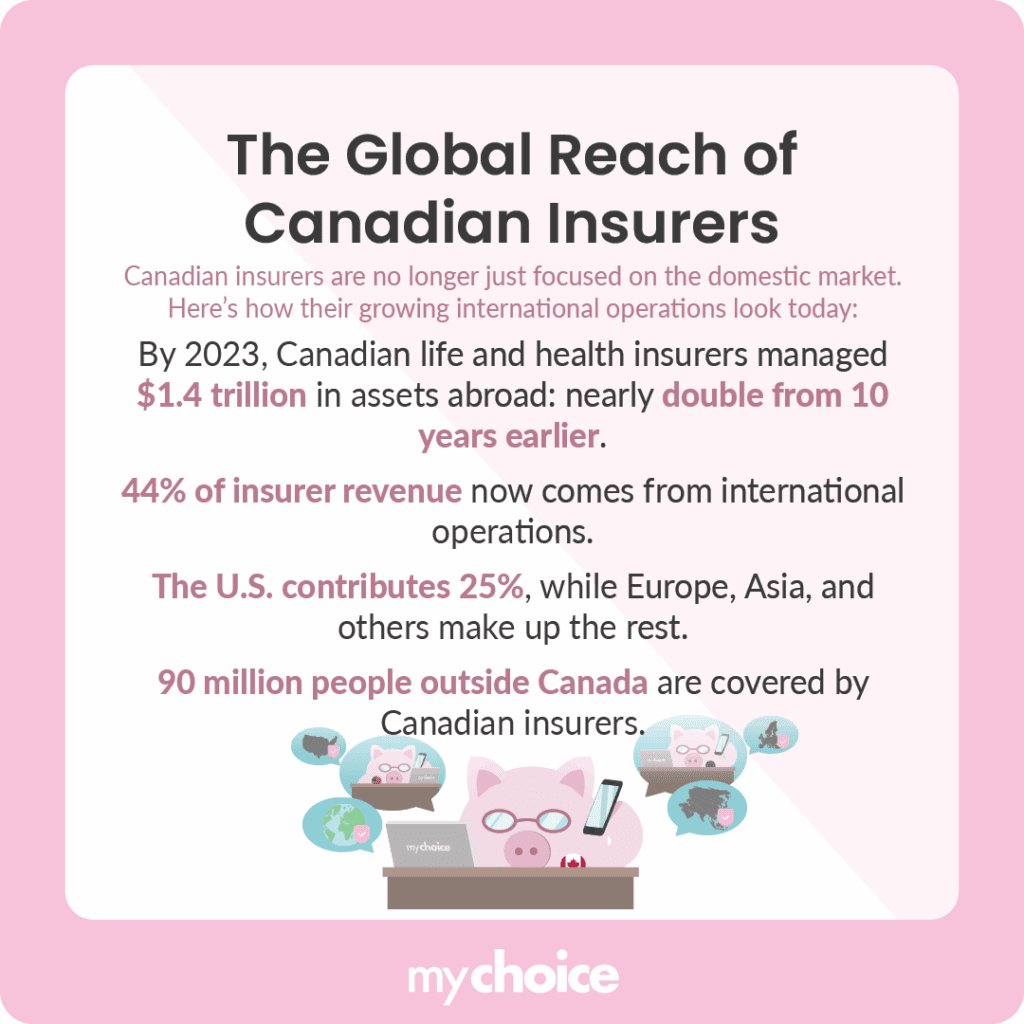

According to CLHIA, Canadian life and health insurance companies held over $1.4 trillion in assets on behalf of policyholders outside Canada as of the end of 2023, nearly double the amount ten years prior.

Additionally, CLHIA data indicate that international operations accounted for 44% of the insurance service revenue of Canadian insurers in 2023. The United States is the largest international revenue contributor, accounting for 25%, with Europe, Asia, and other regions making up the remaining 75%.

With 90 million people outside Canada having insurance protection from Canadian providers, it’s clear to see that the nation’s insurance companies are becoming powerhouses globally, not just at home.

Canada Life’s U.S. Reinsurance Exit

In June 2025, Canada Life Reinsurance announced that it will discontinue new business for its U.S. traditional life mortality risk reinsurance line effective December 31, 2025. While it won’t take on new reinsurance treaties after that date, Canada Life Reinsurance stated that it will still honour and manage existing policies.

In the press release for this announcement, Canada Life Reinsurance stated that the discontinuation of this business line is intended to enable the company to refocus on its structured reinsurance offerings.

Why Are These Shifts Happening?

As times change, so do insurance companies. They need to adapt and expand to meet the changing needs of the market. To understand more about why Canadian insurers are pursuing international expansion and expanding their offerings, let’s take a look at how several market forces influence them:

Implications for Policyholders and Industry

If you’re an individual policyholder, there are probably no significantly noticeable changes to your insurance policy since your protection will likely go on as-is. However, there’s always a chance that your premiums may change because the insurer adjusts to offset the risk changes after international expansion.

As a business insurance policyholder, you may find that with insurance companies expanding to other countries, getting cross-border insurance could be easier as they gain more presence abroad.For the insurance industry at large, international expansion presents numerous challenges, including shifting tax regulations, such as the Global Minimum Tax Act, which may prompt insurers to reassess their business expansion and acquisition strategies.

Key Advice from MyChoice

- As an individual policyholder, your insurance policy likely won’t change much with the expansion of insurance companies.

- If you’re a business insurance policyholder, the partnerships made by your insurer may mean that getting cross-border insurance is more likely.

- With insurers expanding their product offerings beyond just life insurance, you may be able to find other types of insurance coverages like critical illness and pension protection. Consider getting these policy types if they’re more budget-friendly without compromising coverage for your most pressing concerns.