How Life Insurance Underwriters Evaluate You

Underwriters look at multiple areas of your life to assess risk. Below is a quick overview of what they focus on and how you can strengthen your application.

| Risk Factor | What Underwriters Look For | How to Strengthen Your Application |

|---|---|---|

| Health Metrics | Your overall health, including height-to weight ratio, blood sugar, cholesterol, and blood pressure readings. | Maintain a healthy diet, exercise regularly, and schedule checkups to monitor key health stats. |

| Family Medical History | Whether close relatives have had serious conditions (heart disease, cancer, diabetes) at an early age. | Share full details honestly; you can’t change your genes, but you can demonstrate proactive healthcare habits. |

| Lifestyle | Smoking, alcohol use, and other habits that can affect longevity. | Quit smoking, limit alcohol, and document healthy routines (like exercise or stress management activities). |

| Occupation and Hobbies | Jobs or pastimes that could increase risk (e.g., construction, aviation, scuba diving). | If possible, show safety training or certifications that reduce your risk level. |

| Financial Health | Your income, debt levels, and ability to maintain policy payments. | Keep finances in order as assurance that you can maintain premiums long-term. |

| Driving Record | Tickets, DUIs, or accidents can signal risky behaviour. | Drive safely and maintain a clean record for several years before applying, if possible. |

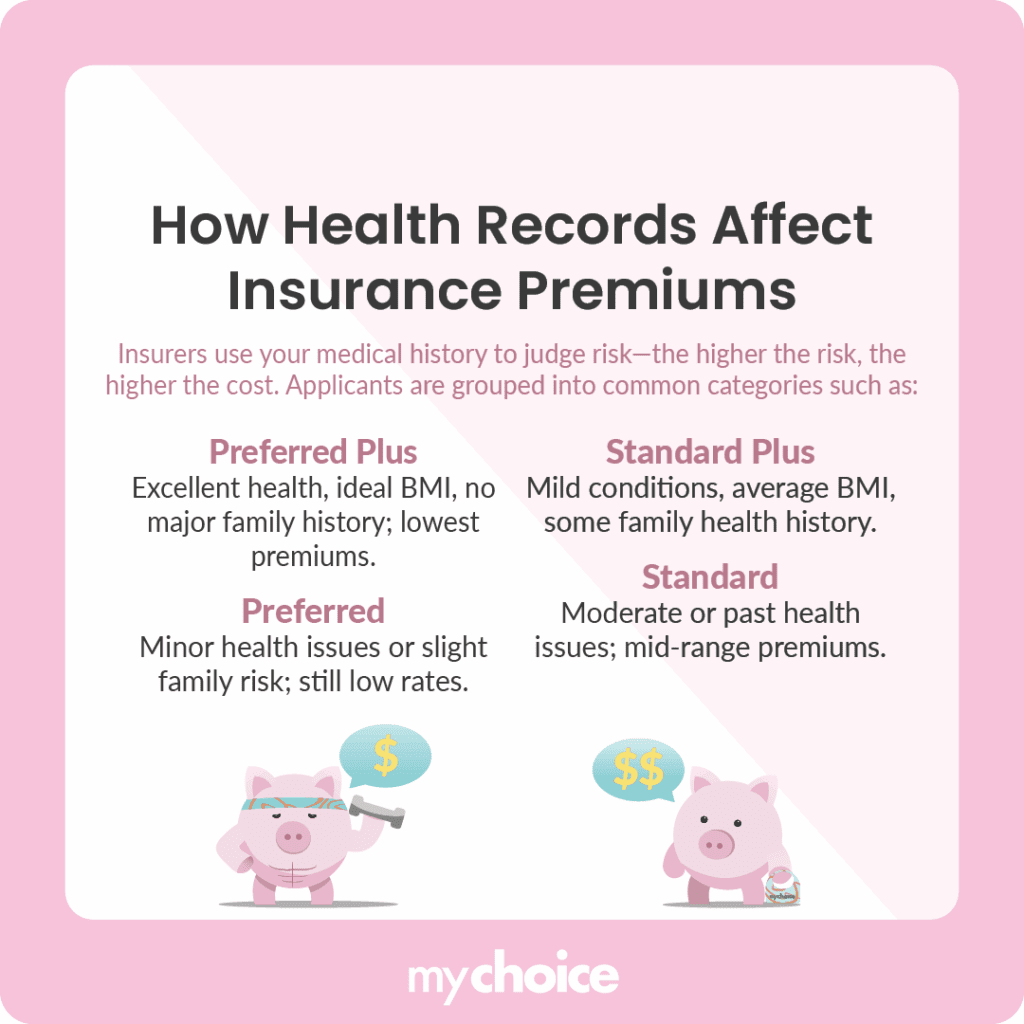

What Are the Main Life Insurance Health Classes?

When underwriters assess your health profile, they assign you to a health class based on your medical records, lifestyle habits, and overall risk factors.

If your health is below average, you can still qualify for coverage — just under a Table Rating (sometimes referred to as “Substandard”). This means the insurer considers you a higher risk because of ongoing or multiple health issues.

The 3 Types of Life Insurance Underwriting in Canada

In Canada, you’ll generally encounter three types of life insurance underwriting depending on how much coverage you want and how detailed your application is.

What Actually Happens During the Underwriting Process

Once you submit a life insurance application, the insurer starts reviewing your information. The process usually looks something like this:

- Step 1: You fill out the application. You’ll answer questions about your health, lifestyle, job, and basic financial details. This can be done online or on paper.

- Step 2: You provide extra information about your health. Depending on the policy, you might need to answer extra medical questions. Some insurers may also ask you to do a quick medical exam, which can include blood or urine tests, or a doctor’s report.

- Step 3: An underwriter reviews your records. An underwriter reviews your application, along with medical reports, lab results, prescription history, and sometimes your driving record. They use all this to understand your risk level.

- Step 4: An insurance company makes a decision. After reviewing the information, the insurer will either approve the application, decline it, or approve it with conditions. Conditions might include a higher premium or slightly different coverage terms.

- Step 5: Sometimes the decision can be postponed. In some situations, the insurer may delay its decision rather than approve or decline right away. This usually happens if there’s a health issue that might improve over time. You can often reapply later.

- Step 6: You receive your policy confirmation. If you’re approved, you’ll get a policy confirmation with the coverage amount, premium, and the full terms of the agreement.

The Rise of AI and Predictive Underwriting in Canada

In Canada, several insurers are adopting AI-driven and predictive underwriting to speed up approvals and improve accuracy. Instead of relying entirely on manual review, these systems analyze large datasets to predict risk with greater precision.

For example, AI can:

- Cross-reference public health data to estimate life expectancy trends

- Assess applications in minutes, reducing waiting times from weeks to days

- Identify inconsistencies or red flags automatically

For customers, that means faster decisions and, in many cases, more personalized pricing. Of course, data privacy remains a top concern, and Canadian insurers must comply with strict privacy laws, such as PIPEDA at the federal level and PHIPA in Ontario.

Key Advice from MyChoice

- Make small, positive lifestyle changes before applying for life insurance. Even little changes show you’re taking care of yourself and reduce the perceived risk of insuring you.

- Compare multiple insurers. Not all insurance companies weigh risk factors the same way, so shopping around can save you money.

- Before applying, gather key details like your doctor’s contact info, medical history, and current medications. Being prepared helps speed up the process and prevent delays.