What to Expect from a Life Insurance Medical Exam

During the exam, a licensed nurse or paramedical professional (arranged by the insurer) will come to your home, office, or you will have to visit them at a dedicated clinic.

During the exam, they will:

- Discuss your health and any current or past medical conditions you might have. This might include a history of high blood pressure, high cholesterol, diabetes, asthma, etc.

- Ask you about the stability of these conditions. They might ask you whether you’ve recently been hospitalized or had surgery or request information on upcoming tests/medical investigations.

- Discuss any prescriptions you’re taking. This will include questions around dosing and how long you’ve been taking your medications.

- Talk to you about your family history. They might ask about who in your family has had cancer, heart disease or kidney disease or any other hereditary conditions.

- Ask you about your lifestyle. This might include smoking habits, alcohol or drug use, exercise habits, or high-risk activities such as rock climbing, motorcycle racing or scuba diving.

- Check your blood pressure. A healthy reading is a systolic pressure (top number) of less than 120 mm Hg and a diastolic pressure (bottom number) of less than 80 mm Hg.

- Record your weight. This will be used to check your BMI, or Body to Mass Index. Learn how BMI can affect your insurance rates.

- Obtain blood samples. Your blood will be tested for cholesterol, blood sugar, kidney and liver function, immune system function and blood count. Your blood will also be screened for smoking or drug use.

- Obtain a urine sample. This tests for protein, glucose and medications.

A simple exam usually takes between 20 minutes to an hour. Sometimes an insurer will request a more detailed exam, particularly if you disclose ongoing, serious medical conditions. This exam might include an EKG, a test which measures your heart rate and rhythm.

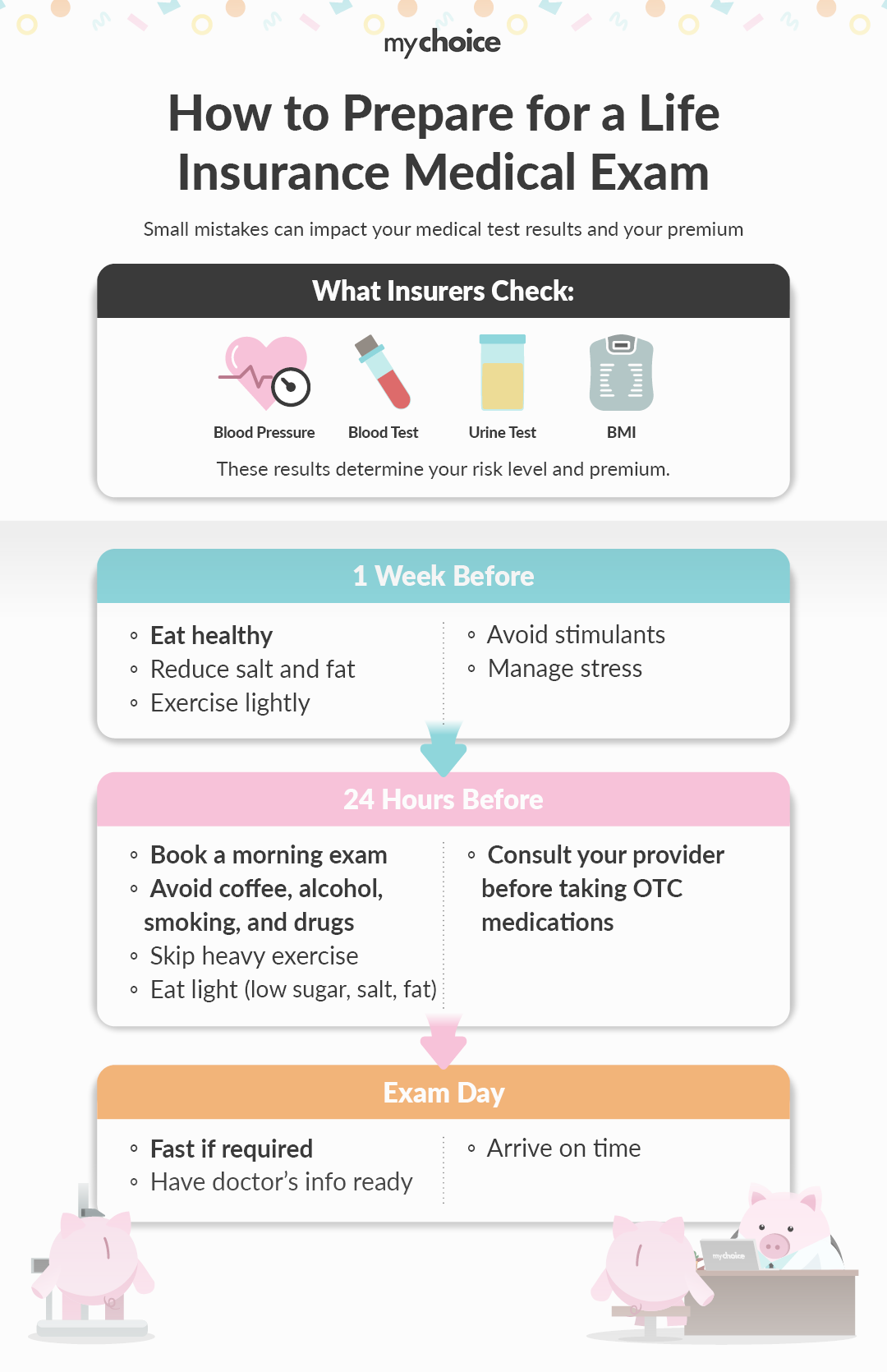

What to Do a Week Before the Exam

The longer you can prepare for your life insurance medical, the better. At a minimum, start planning a week before your exam, cutting out fatty or salty foods, exercising moderately, avoiding any stimulants and keeping your stress under control.

Life Insurance Blood Test Preparation

Being prepared for a life insurance blood test is key in getting the best rate possible. Take the following steps to prepare for a medical, starting 24 hours before the exam:

- Pick an optimal visit time. Schedule your exam in the morning when your vital signs are most stable. It is also easier to fast overnight.

- Find out if you need to fast before any bloodwork. Some blood tests require that you not eat or drink for eight to twelve hours beforehand.

- Skip the stimulants. Do not have any coffee, alcohol, recreational drugs or smoke for 24 hours before the exam to optimize blood pressure and blood tests.

- Forgo exercise. Strenuous exercise, such as running long distances or weightlifting, may raise your blood pressure and increase protein levels in your urine, which may result in temporarily elevated readings that affect your risk assessment.

- Eat sensibly. Avoid foods high in sugar or salt. Skip fatty meals, which can elevate cholesterol readings, or foods such as poppy seeds, which can cause false positives on drug screens.

- Avoid certain over-the-counter medications. Popular nasal decongestants or antihistamines, which treat allergies, can elevate blood pressure.

- Do your homework: Have your doctors’ names and contact information handy.

Common Mistakes Made During a Life Insurance Medical

Avoid these errors to ensure your medical goes as smoothly as possible:

- Over-indulging the night before. Eating a heavy, greasy meal can quickly skew cholesterol readings.

- Forgetting to stay hydrated. It’s important to drink water while fasting to ensure your kidneys are working well.

- Going for a morning run. Exercising is great. But don’t jog ahead of your medical exam.

- Doing the exam while fighting an infection. If you’ve got a cold or flu, make sure you reschedule your exam to ensure accurate readings.

- Not being honest. If you ‘forget’ to mention a history of cancer or that you’ve been a long-term smoker, you may be denied coverage or have your claim denied at a later time.

Key Advice from MyChoice

- Prepare for your medical ahead of time, even if it is just for a few days. Small changes, such as avoiding alcohol, eating healthy, and skipping hard workouts, can help your results.

- Be honest and clear. If your answers do not match your medical results, it can slow down or hurt your application.

- Compare policies from different insurers. Each company looks at medical and lifestyle factors in its own way, so getting several quotes can help you find a better option.